Government Securities - UPSC Economy

What is Government Securities in UPSC Economy?

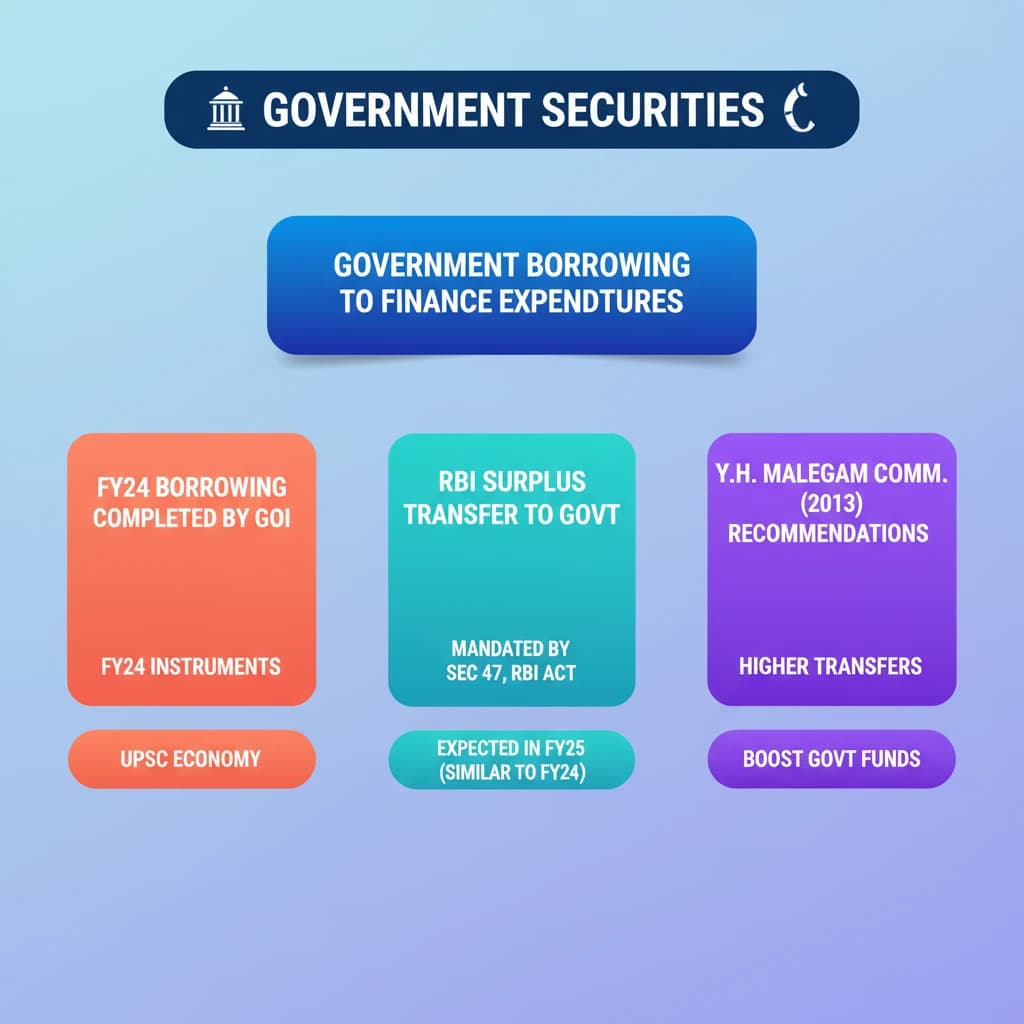

Government Securities is a key topic under Economy for UPSC Civil Services Examination. Key points include: Government Securities (G-Secs) are key instruments for government borrowing to finance expenditures.. The Government of India completed G-Sec borrowing for FY 2023-24.. RBI is expected to transfer a dividend to the government in FY25, similar to FY24.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Government Securities important for UPSC exam?

Government Securities is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Government Securities, making it essential for comprehensive IAS preparation.

How to prepare Government Securities for UPSC?

To prepare Government Securities for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Government Securities to related GS Paper topics.

Key takeaways of Government Securities for UPSC

- Government Securities (G-Secs) are key instruments for government borrowing to finance expenditures.

- The Government of India completed G-Sec borrowing for FY 2023-24.

- RBI is expected to transfer a dividend to the government in FY25, similar to FY24.

- RBI's surplus transfer to the government is mandated by Section 47 of the RBI Act, 1934.

- The Y.H. Malegam Committee (2013) recommended higher transfers of RBI's surplus to the government.

- RBI's surplus is determined by its income (interest on securities, fees, forex profits) minus expenditures (printing currency, salaries, provisions).

- RBI's dividend provides crucial non-tax revenue, impacting the government's fiscal deficit and overall borrowing needs.

Government Securities

📖 Introduction

💡 Key Takeaways

- •Government Securities (G-Secs) are key instruments for government borrowing to finance expenditures.

- •The Government of India completed G-Sec borrowing for FY 2023-24.

- •RBI is expected to transfer a dividend to the government in FY25, similar to FY24.

- •RBI's surplus transfer to the government is mandated by Section 47 of the RBI Act, 1934.

- •The Y.H. Malegam Committee (2013) recommended higher transfers of RBI's surplus to the government.

- •RBI's surplus is determined by its income (interest on securities, fees, forex profits) minus expenditures (printing currency, salaries, provisions).

- •RBI's dividend provides crucial non-tax revenue, impacting the government's fiscal deficit and overall borrowing needs.

🧠 Memory Techniques