India’s Taxation System - UPSC Economy

What is India’s Taxation System in UPSC Economy?

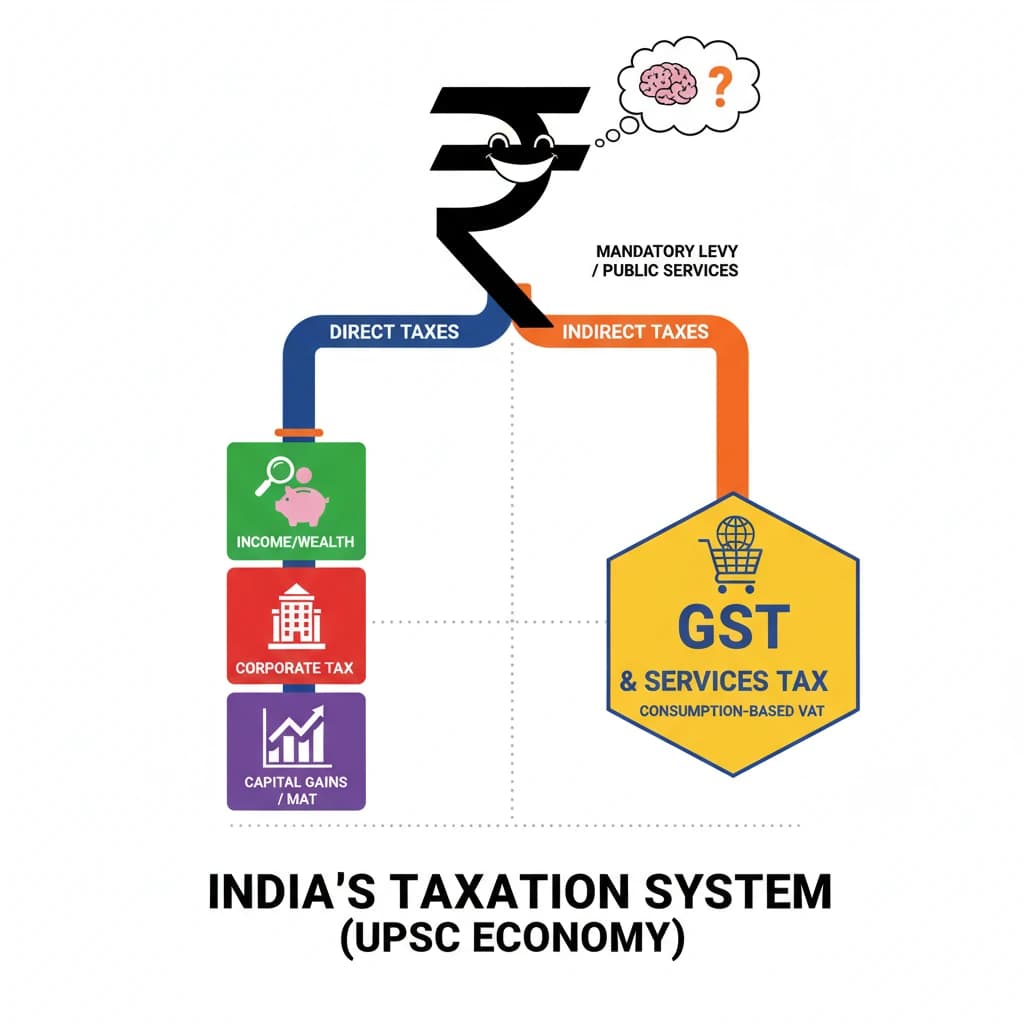

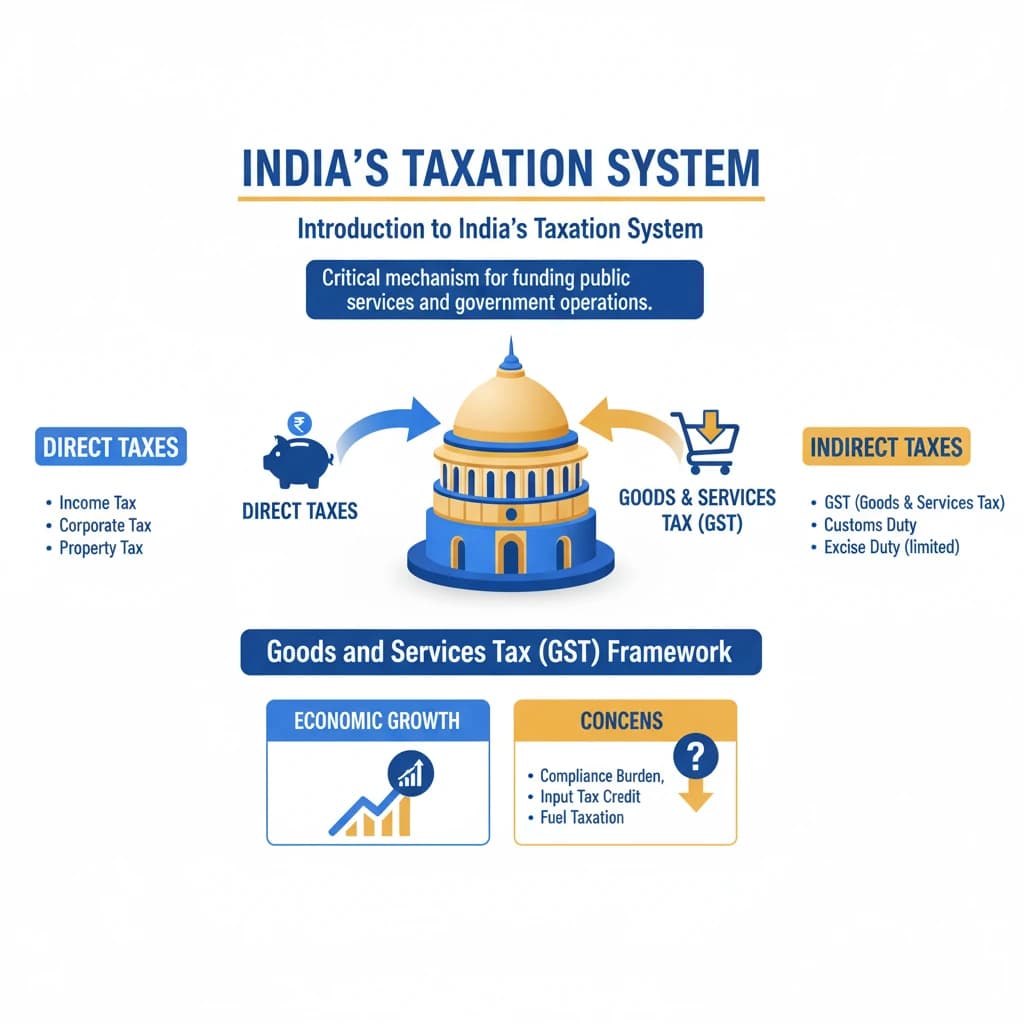

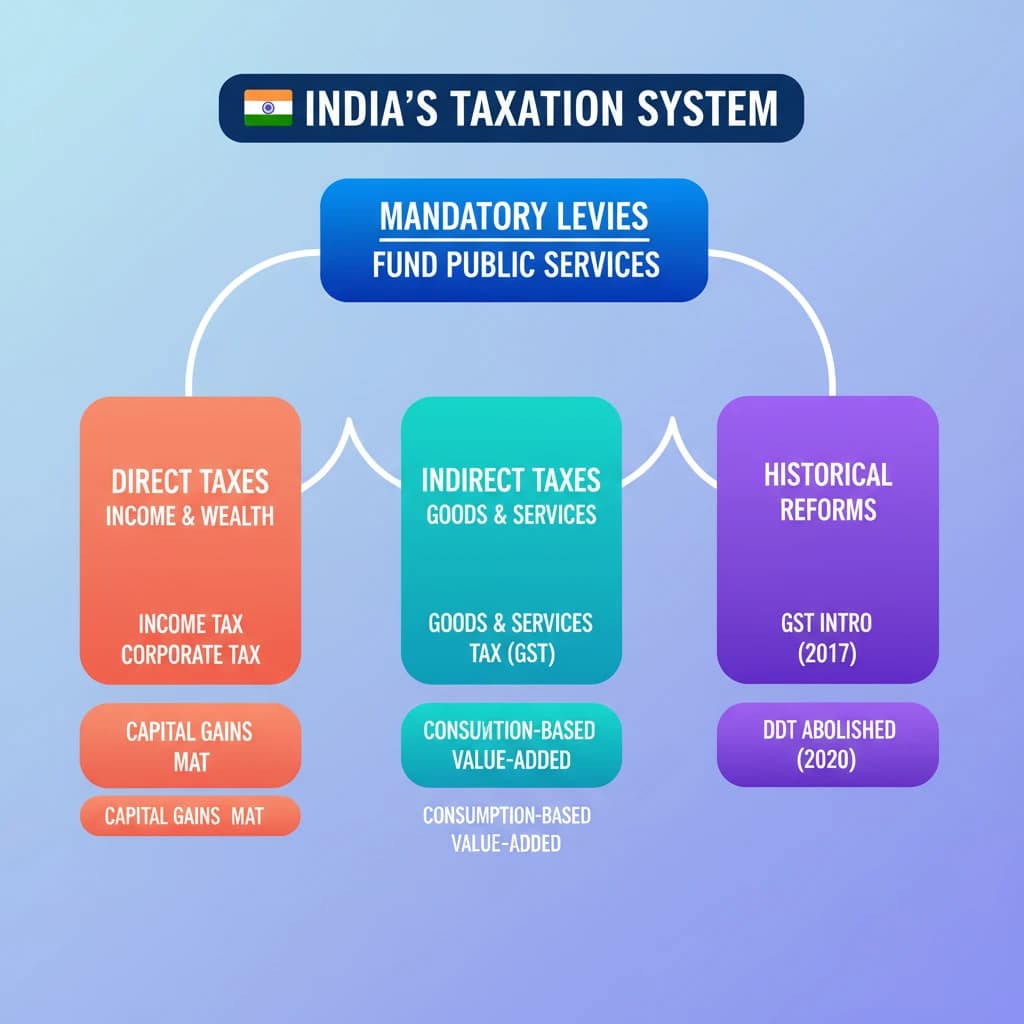

India’s Taxation System is a key topic under Economy for UPSC Civil Services Examination. Key points include: Taxes are mandatory government levies to fund public services, without direct quid pro quo.. India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).. Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is India’s Taxation System important for UPSC exam?

India’s Taxation System is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of India’s Taxation System, making it essential for comprehensive IAS preparation.

How to prepare India’s Taxation System for UPSC?

To prepare India’s Taxation System for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking India’s Taxation System to related GS Paper topics.

Key takeaways of India’s Taxation System for UPSC

- Taxes are mandatory government levies to fund public services, without direct quid pro quo.

- India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).

- Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).

- Key Indirect Tax: Goods and Services Tax (GST), a consumption-based, value-added tax.

- Historical reforms include the abolition of FBT/BCTT (2009) and DDT (2020), and the introduction of GST (2017).

- The current GST framework's impact on growth, business, consumption, and investment reputation is a key area of discussion.

India’s Taxation System

📖 Introduction

💡 Key Takeaways

- •Taxes are mandatory government levies to fund public services, without direct quid pro quo.

- •India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).

- •Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).

- •Key Indirect Tax: Goods and Services Tax (GST), a consumption-based, value-added tax.

- •Historical reforms include the abolition of FBT/BCTT (2009) and DDT (2020), and the introduction of GST (2017).

- •The current GST framework's impact on growth, business, consumption, and investment reputation is a key area of discussion.

🧠 Memory Techniques