Angel Tax and Capital Gain Tax - UPSC Economy

What is Angel Tax and Capital Gain Tax in UPSC Economy?

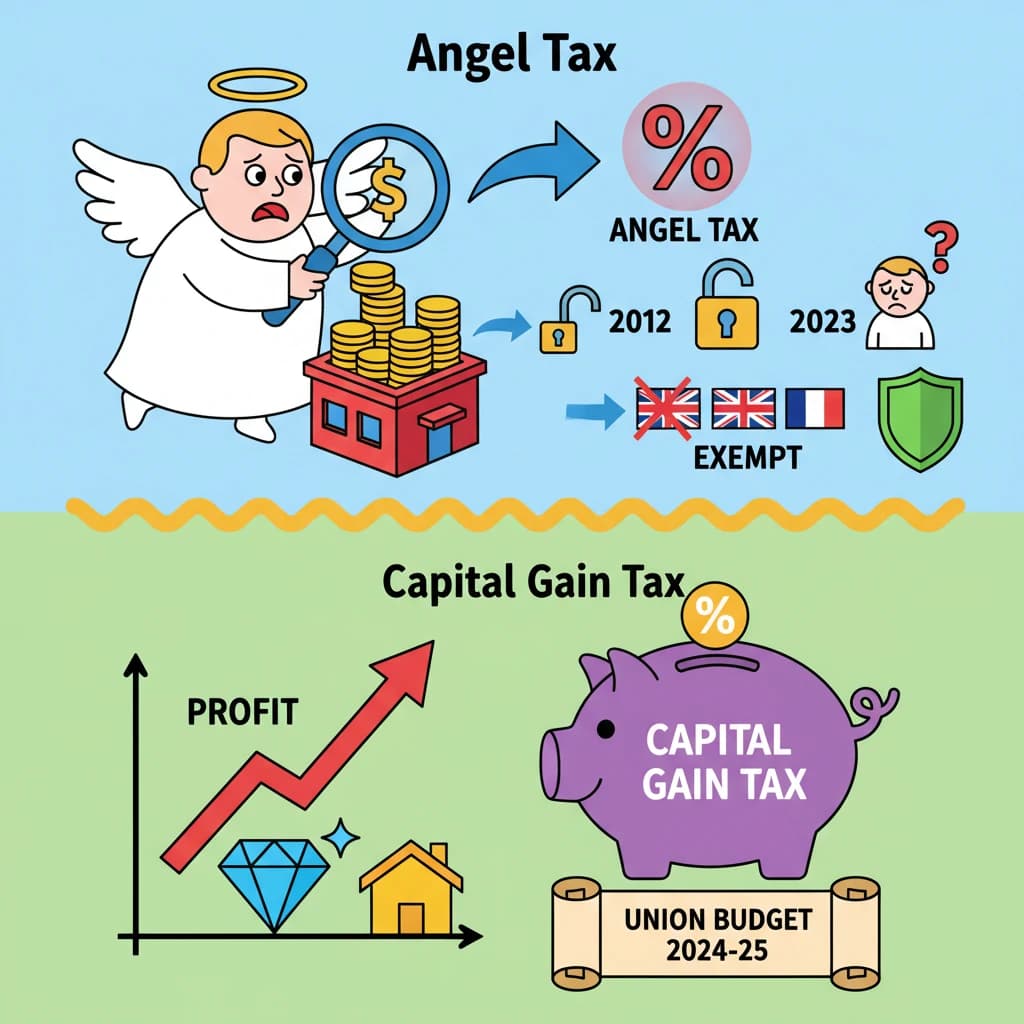

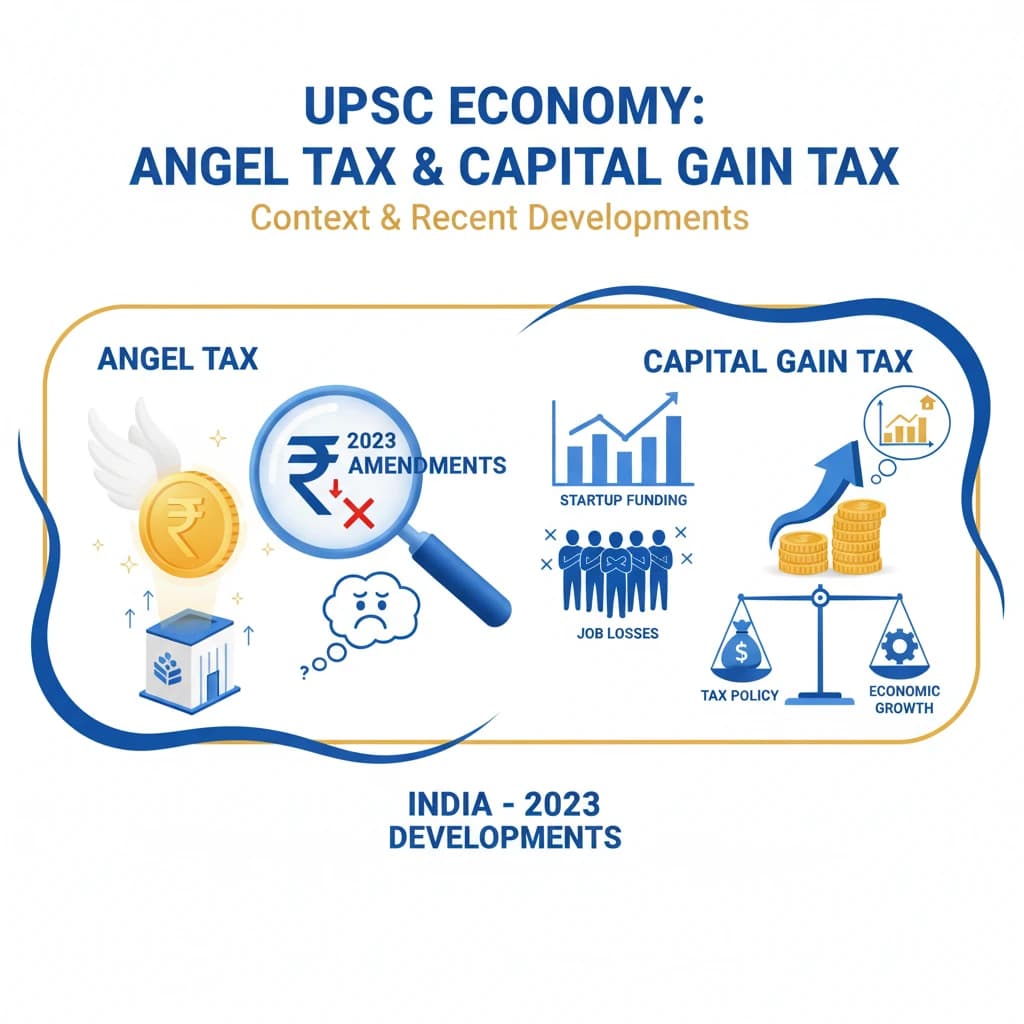

Angel Tax and Capital Gain Tax is a key topic under Economy for UPSC Civil Services Examination. Key points include: Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.. Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.. DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Angel Tax and Capital Gain Tax important for UPSC exam?

Angel Tax and Capital Gain Tax is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Angel Tax and Capital Gain Tax, making it essential for comprehensive IAS preparation.

How to prepare Angel Tax and Capital Gain Tax for UPSC?

To prepare Angel Tax and Capital Gain Tax for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Angel Tax and Capital Gain Tax to related GS Paper topics.

Key takeaways of Angel Tax and Capital Gain Tax for UPSC

- Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.

- Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.

- DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.

- Capital Gain Tax is a tax on profits from selling capital assets, gaining attention for the Union Budget 2024-25.

- These taxes significantly impact startup funding, investor confidence, and India's 'Ease of Doing Business' ranking.

Angel Tax and Capital Gain Tax

📖 Introduction

💡 Key Takeaways

- •Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.

- •Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.

- •DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.

- •Capital Gain Tax is a tax on profits from selling capital assets, gaining attention for the Union Budget 2024-25.

- •These taxes significantly impact startup funding, investor confidence, and India's 'Ease of Doing Business' ranking.

🧠 Memory Techniques