Omnibus SRO Restrictions - UPSC Economy

What is Omnibus SRO Restrictions in UPSC Economy?

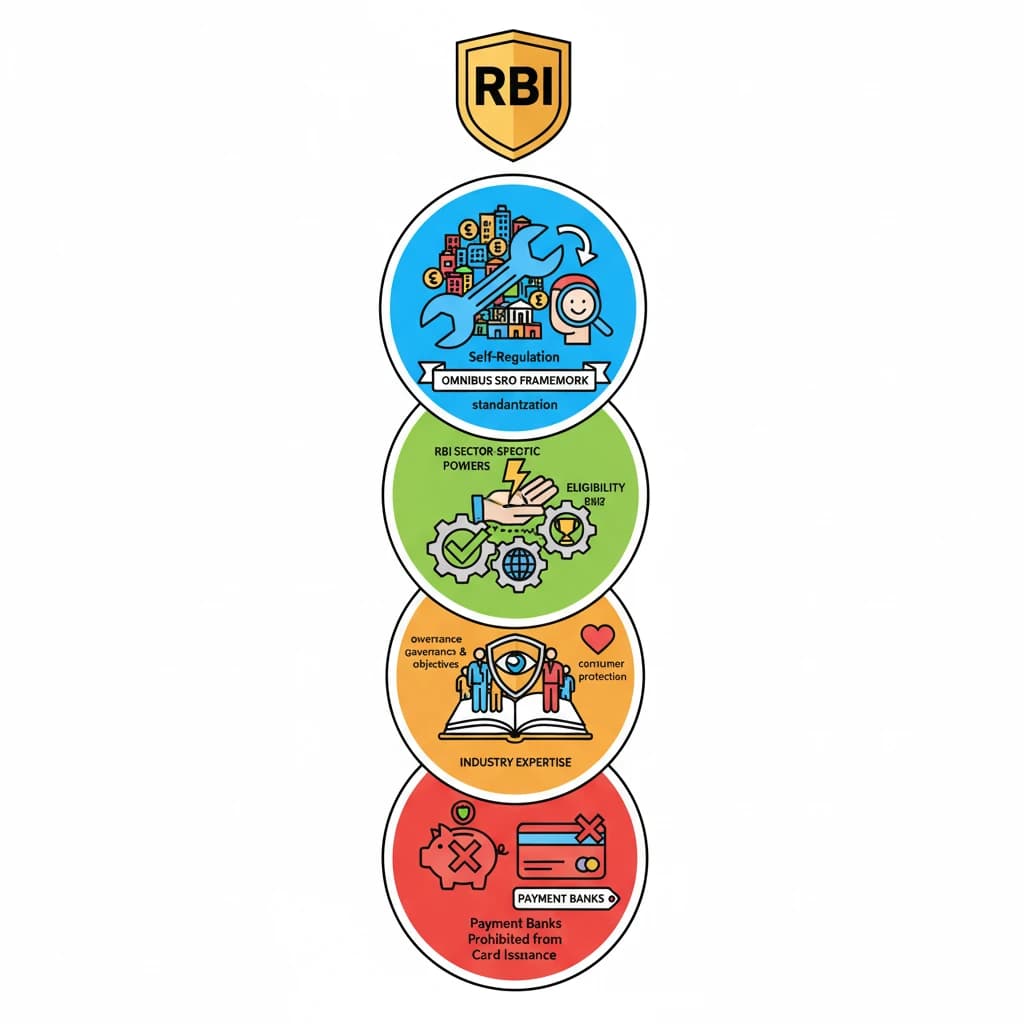

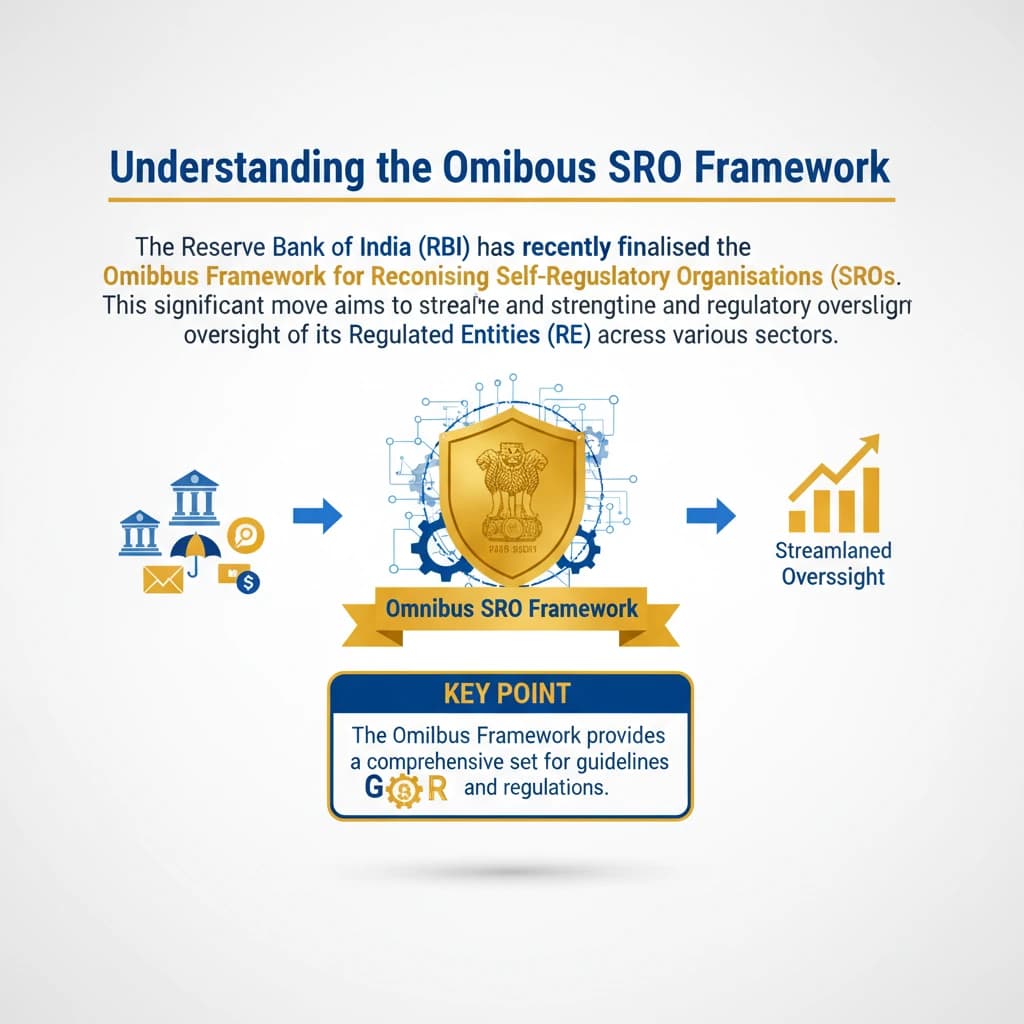

Omnibus SRO Restrictions is a key topic under Economy for UPSC Civil Services Examination. Key points include: RBI's Omnibus SRO Framework standardises self-regulation for all its Regulated Entities.. The framework sets common objectives, governance, and eligibility for SROs, with RBI retaining sector-specific powers.. SROs leverage industry expertise for oversight, compliance, and consumer protection.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Omnibus SRO Restrictions important for UPSC exam?

Omnibus SRO Restrictions is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Omnibus SRO Restrictions, making it essential for comprehensive IAS preparation.

How to prepare Omnibus SRO Restrictions for UPSC?

To prepare Omnibus SRO Restrictions for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Omnibus SRO Restrictions to related GS Paper topics.

Key takeaways of Omnibus SRO Restrictions for UPSC

- RBI's Omnibus SRO Framework standardises self-regulation for all its Regulated Entities.

- The framework sets common objectives, governance, and eligibility for SROs, with RBI retaining sector-specific powers.

- SROs leverage industry expertise for oversight, compliance, and consumer protection.

- Payment Banks are RBI-regulated entities prohibited from lending and credit card issuance.

- Payment Banks focus on deposits (up to Rs 2 lakh), remittances, and digital payments, with a 25% rural outreach mandate.

Omnibus SRO Restrictions

📖 Introduction

💡 Key Takeaways

- •RBI's Omnibus SRO Framework standardises self-regulation for all its Regulated Entities.

- •The framework sets common objectives, governance, and eligibility for SROs, with RBI retaining sector-specific powers.

- •SROs leverage industry expertise for oversight, compliance, and consumer protection.

- •Payment Banks are RBI-regulated entities prohibited from lending and credit card issuance.

- •Payment Banks focus on deposits (up to Rs 2 lakh), remittances, and digital payments, with a 25% rural outreach mandate.

🧠 Memory Techniques