RBI Guidelines Related to Microfinance Lending (2022) - UPSC Economy

What is RBI Guidelines Related to Microfinance Lending (2022) in UPSC Economy?

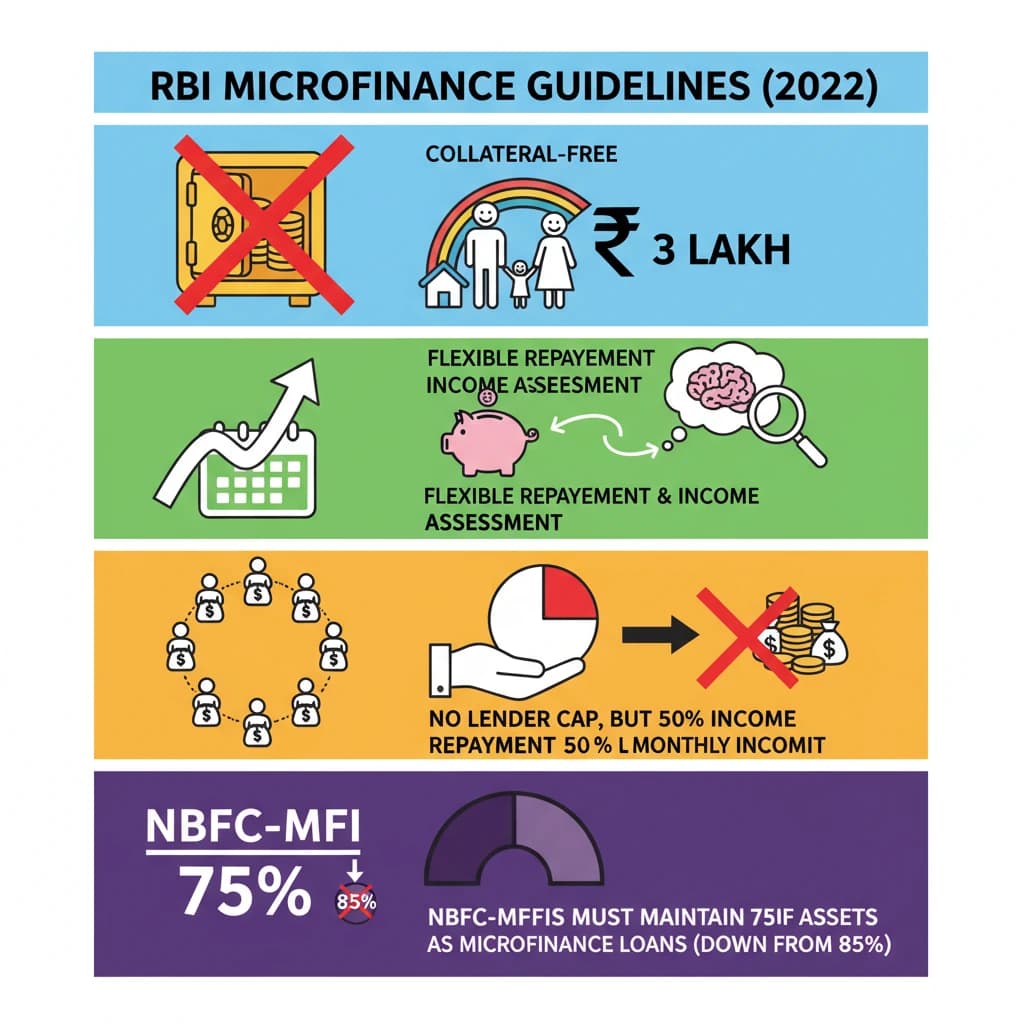

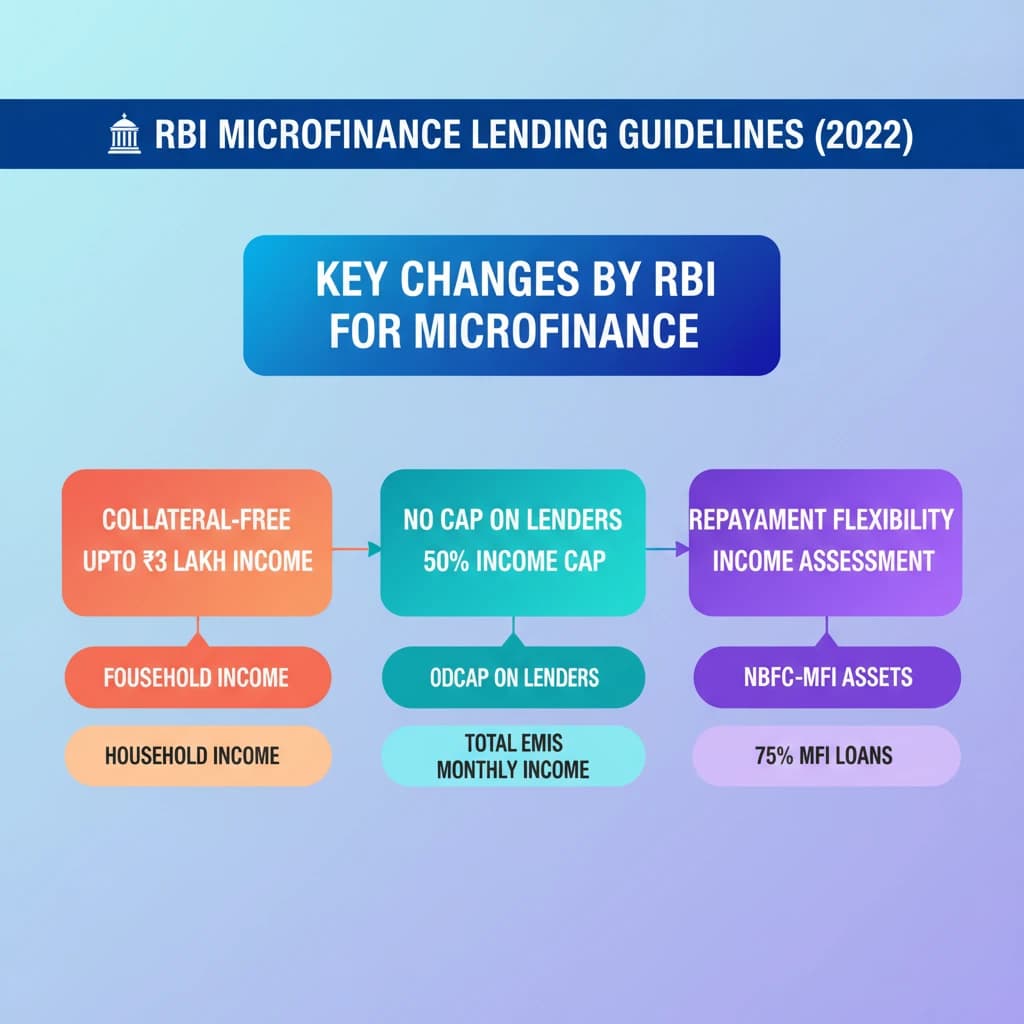

RBI Guidelines Related to Microfinance Lending (2022) is a key topic under Economy for UPSC Civil Services Examination. Key points include: Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.. Lenders must implement policies for flexible repayment and robust household income assessment.. The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is RBI Guidelines Related to Microfinance Lending (2022) important for UPSC exam?

RBI Guidelines Related to Microfinance Lending (2022) is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of RBI Guidelines Related to Microfinance Lending (2022), making it essential for comprehensive IAS preparation.

How to prepare RBI Guidelines Related to Microfinance Lending (2022) for UPSC?

To prepare RBI Guidelines Related to Microfinance Lending (2022) for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking RBI Guidelines Related to Microfinance Lending (2022) to related GS Paper topics.

Key takeaways of RBI Guidelines Related to Microfinance Lending (2022) for UPSC

- Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.

- Lenders must implement policies for flexible repayment and robust household income assessment.

- The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.

- NBFC-MFIs must maintain 75% of their assets as microfinance loans (down from 85%).

- Entities are mandated to report income discrepancies and household income.

- No pre-payment penalties are allowed, and late fees apply only to the overdue amount.

- The guidelines aim for regulatory harmonization and enhanced borrower protection across all regulated entities.

RBI Guidelines Related to Microfinance Lending (2022)

📖 Introduction

💡 Key Takeaways

- •Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.

- •Lenders must implement policies for flexible repayment and robust household income assessment.

- •The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.

- •NBFC-MFIs must maintain 75% of their assets as microfinance loans (down from 85%).

- •Entities are mandated to report income discrepancies and household income.

- •No pre-payment penalties are allowed, and late fees apply only to the overdue amount.

- •The guidelines aim for regulatory harmonization and enhanced borrower protection across all regulated entities.

🧠 Memory Techniques