What are Payment Banks? - UPSC Economy

What is What are Payment Banks? in UPSC Economy?

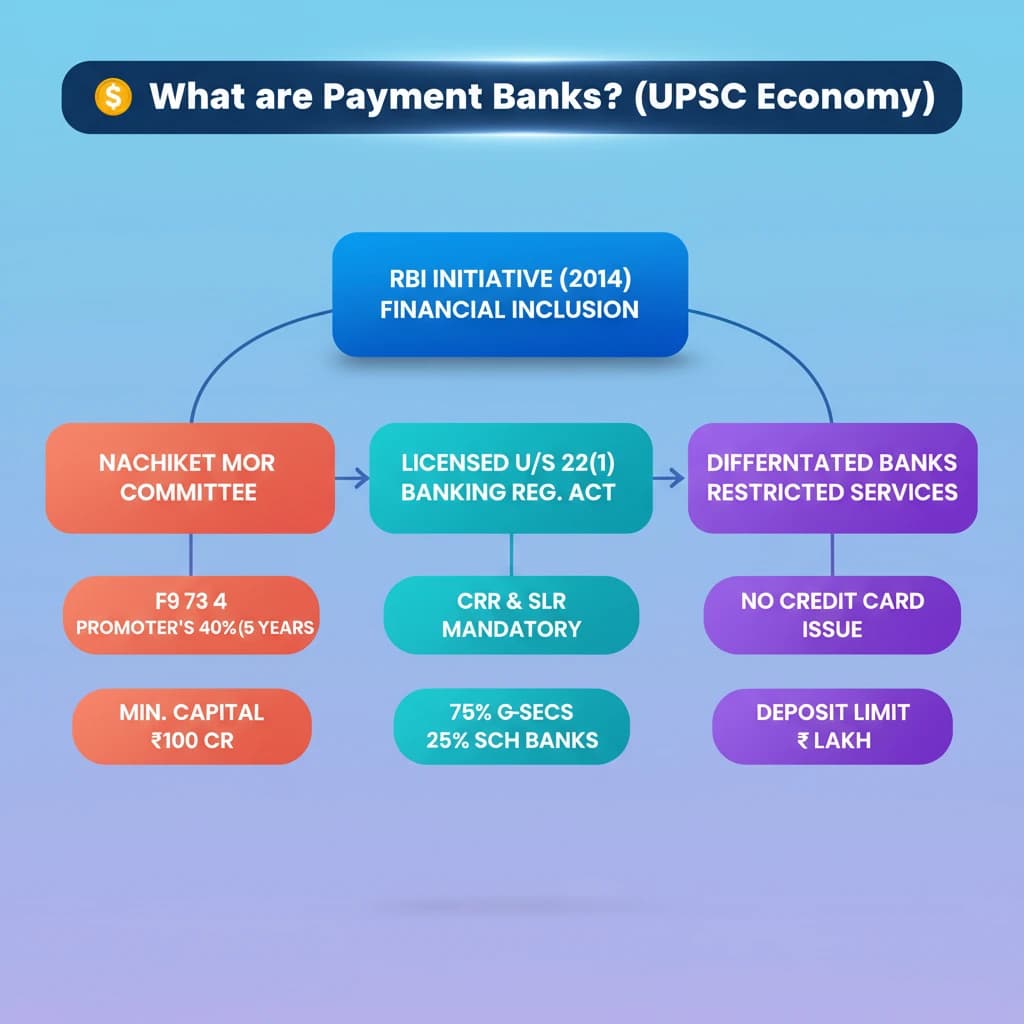

What are Payment Banks? is a key topic under Economy for UPSC Civil Services Examination. Key points include: Payment Banks are specialized banks introduced by RBI in 2014 to promote financial inclusion.. They were established based on the recommendations of the Nachiket Mor committee.. Licensed under Section 22 (1) of the Banking Regulation Act, 1949, as differentiated banks with restricted services.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are Payment Banks? important for UPSC exam?

What are Payment Banks? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are Payment Banks?, making it essential for comprehensive IAS preparation.

How to prepare What are Payment Banks? for UPSC?

To prepare What are Payment Banks? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are Payment Banks? to related GS Paper topics.

Key takeaways of What are Payment Banks? for UPSC

- Payment Banks are specialized banks introduced by RBI in 2014 to promote financial inclusion.

- They were established based on the recommendations of the Nachiket Mor committee.

- Licensed under Section 22 (1) of the Banking Regulation Act, 1949, as differentiated banks with restricted services.

- Required to maintain CRR and SLR; 75% of demand deposits in G-secs/T-bills (up to 1 year), 25% in other scheduled commercial banks.

- Minimum paid-up equity capital is ₹100 crore; promoter's initial contribution is 40% for the first 5 years.

- They cannot undertake lending activities, issue credit cards, or accept large deposits (currently capped at ₹2 lakh per customer).

- Primary focus is on deposits, remittances, and payment services, often leveraging digital platforms.

What are Payment Banks?

📖 Introduction

💡 Key Takeaways

- •Payment Banks are specialized banks introduced by RBI in 2014 to promote financial inclusion.

- •They were established based on the recommendations of the Nachiket Mor committee.

- •Licensed under Section 22 (1) of the Banking Regulation Act, 1949, as differentiated banks with restricted services.

- •Required to maintain CRR and SLR; 75% of demand deposits in G-secs/T-bills (up to 1 year), 25% in other scheduled commercial banks.

- •Minimum paid-up equity capital is ₹100 crore; promoter's initial contribution is 40% for the first 5 years.

- •They cannot undertake lending activities, issue credit cards, or accept large deposits (currently capped at ₹2 lakh per customer).

- •Primary focus is on deposits, remittances, and payment services, often leveraging digital platforms.

🧠 Memory Techniques