What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? - UPSC Economy

What is What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? in UPSC Economy?

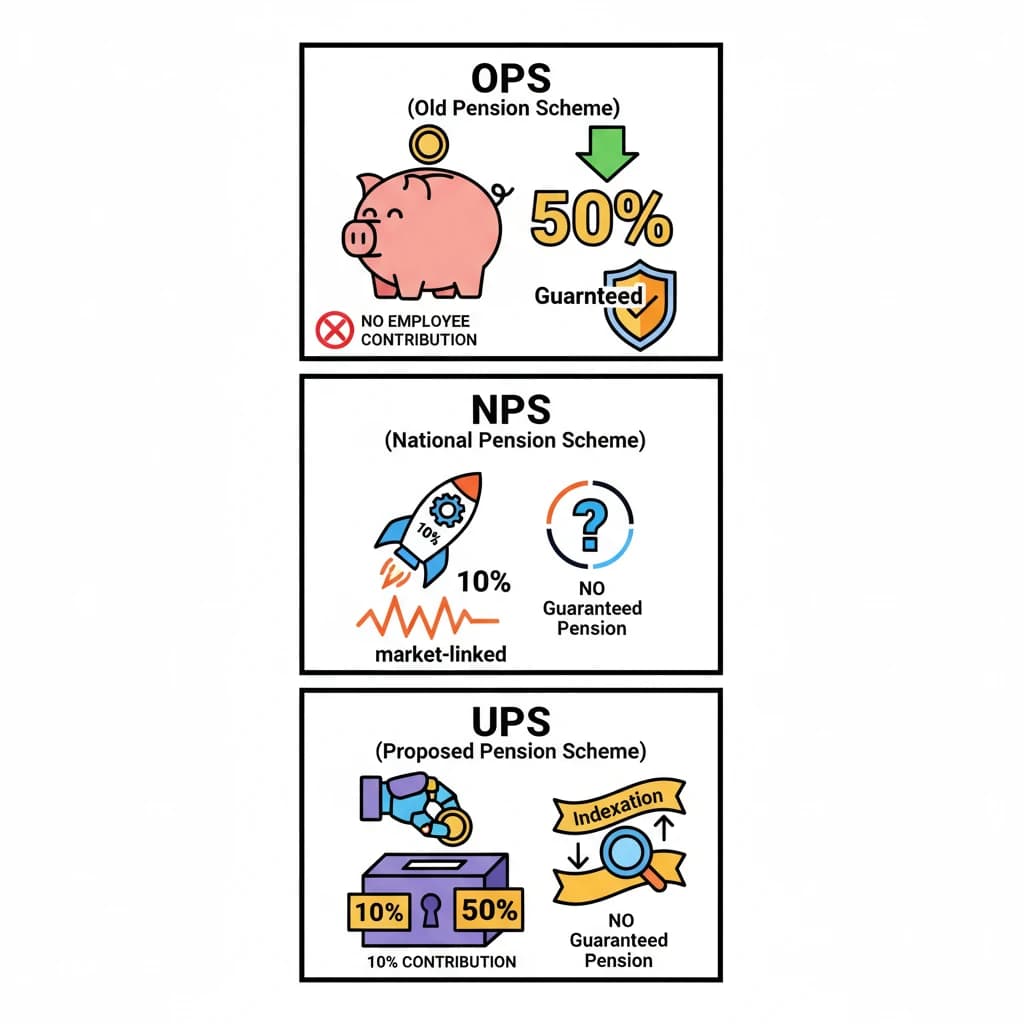

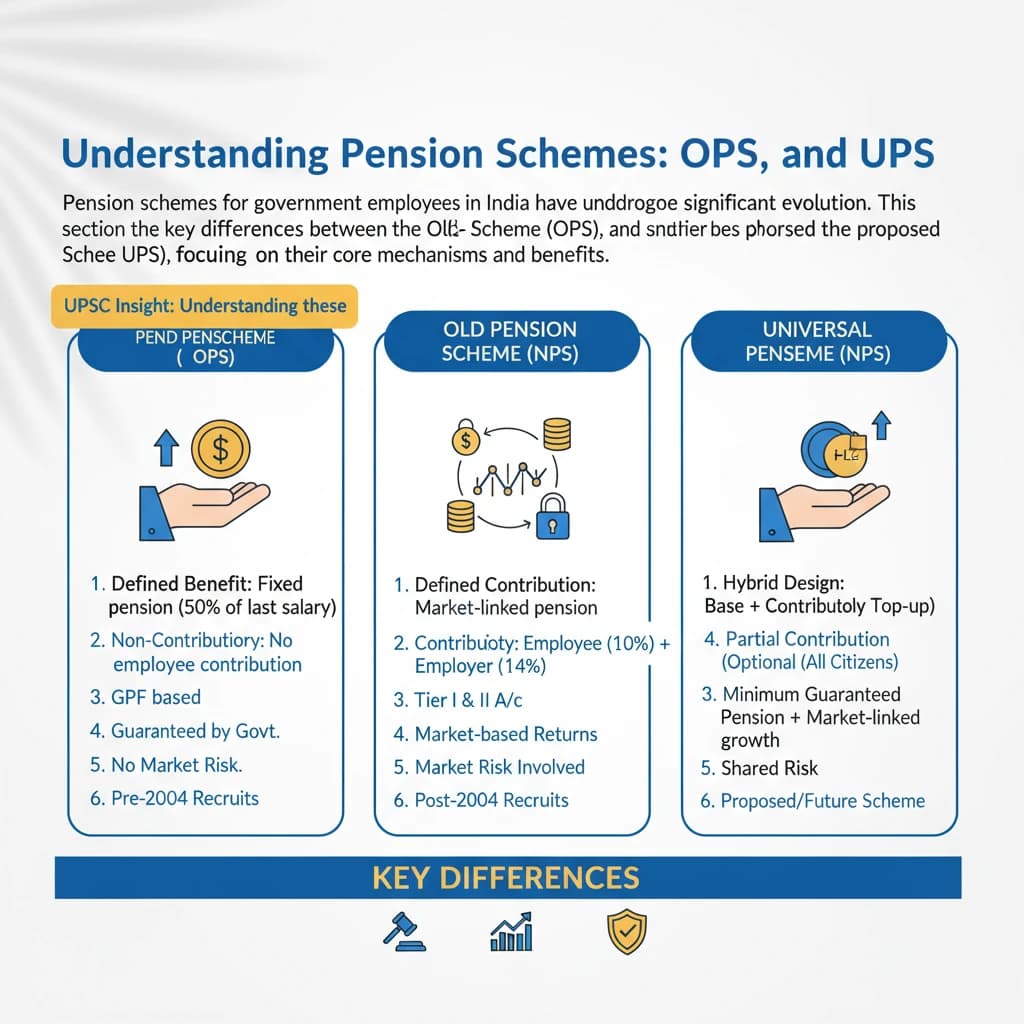

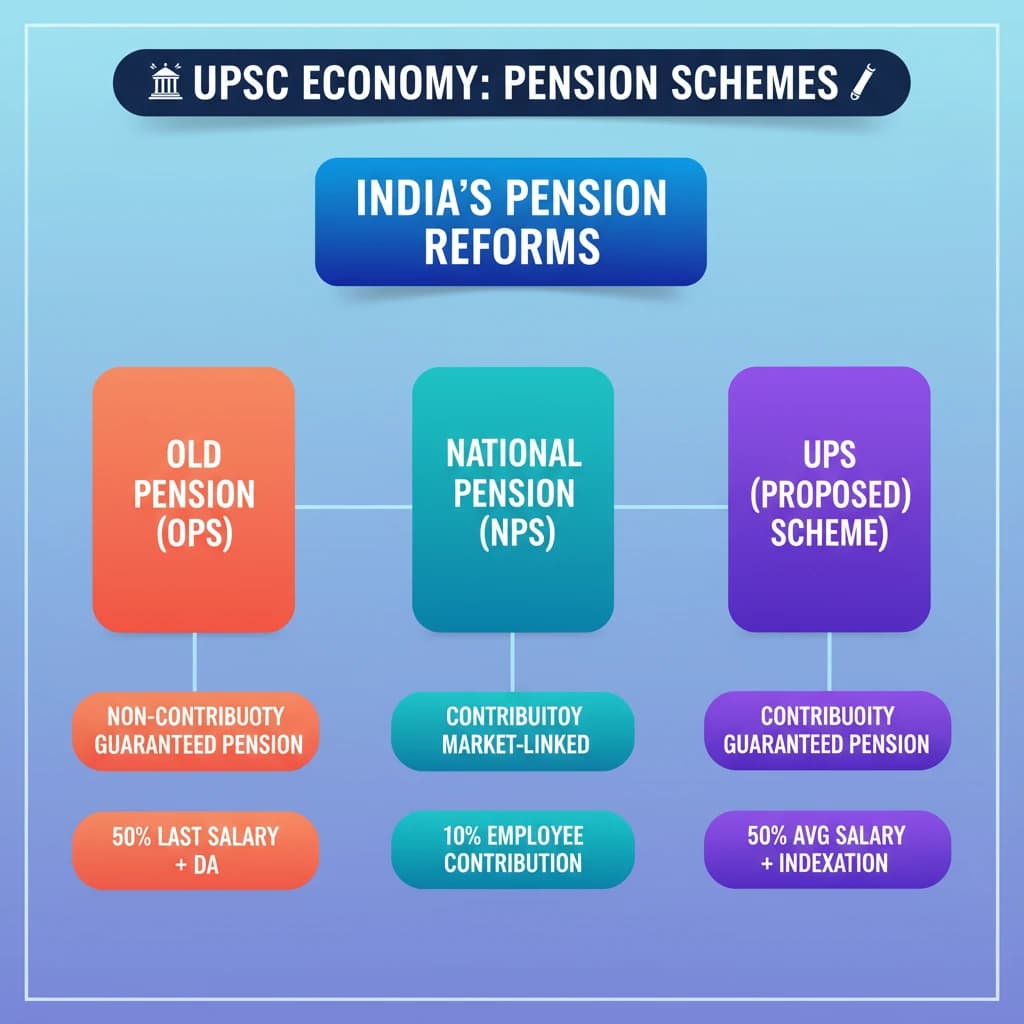

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? is a key topic under Economy for UPSC Civil Services Examination. Key points include: OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).. NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.. UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? important for UPSC exam?

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)?, making it essential for comprehensive IAS preparation.

How to prepare What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC?

To prepare What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? to related GS Paper topics.

Key takeaways of What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC

- OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).

- NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.

- UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.

- OPS has no employee contribution; UPS and NPS require 10% employee contribution.

- NPS offers clear tax benefits on government contributions; UPS tax benefits are yet to be clarified.

- UPS includes a lump sum payment at retirement and pension indexation based on CPI-IW.

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)?

📖 Introduction

💡 Key Takeaways

- •OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).

- •NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.

- •UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.

- •OPS has no employee contribution; UPS and NPS require 10% employee contribution.

- •NPS offers clear tax benefits on government contributions; UPS tax benefits are yet to be clarified.

- •UPS includes a lump sum payment at retirement and pension indexation based on CPI-IW.

🧠 Memory Techniques