Loading page, please wait…

Angel Tax and Capital Gain Tax - UPSC Economy

What is Angel Tax and Capital Gain Tax in UPSC Economy?

Angel Tax and Capital Gain Tax is a key topic under Economy for UPSC Civil Services Examination. Key points include: Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.. Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.. DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Angel Tax and Capital Gain Tax important for UPSC exam?

Angel Tax and Capital Gain Tax is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Angel Tax and Capital Gain Tax, making it essential for comprehensive IAS preparation.

How to prepare Angel Tax and Capital Gain Tax for UPSC?

To prepare Angel Tax and Capital Gain Tax for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Angel Tax and Capital Gain Tax to related GS Paper topics.

Key takeaways of Angel Tax and Capital Gain Tax for UPSC

- Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.

- Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.

- DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.

- Capital Gain Tax is a tax on profits from selling capital assets, gaining attention for the Union Budget 2024-25.

- These taxes significantly impact startup funding, investor confidence, and India's 'Ease of Doing Business' ranking.

Angel Tax and Capital Gain Tax

Medium⏱️ 7 min read

economy

📖 Introduction

Context and Recent Developments

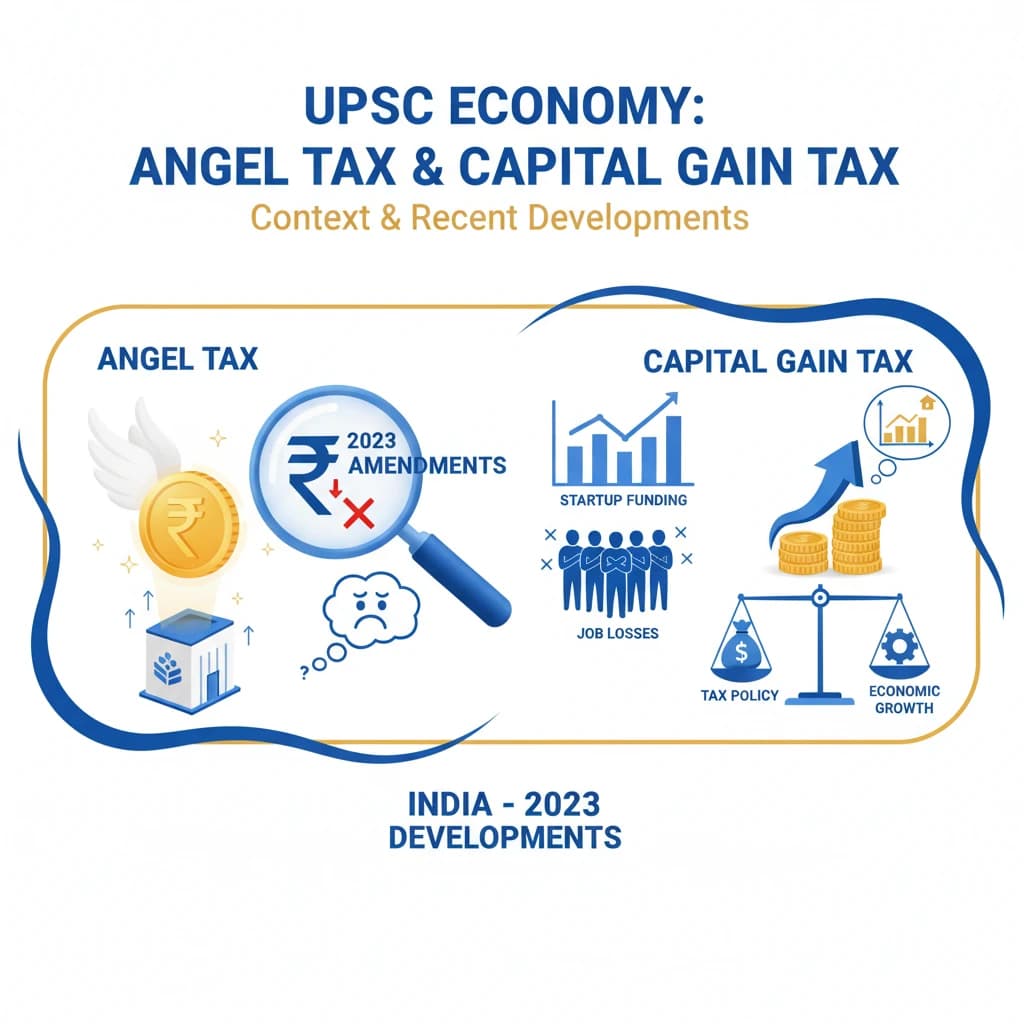

The Angel Tax and Capital Gain Tax have recently garnered significant attention in India. Amendments made in 2023 broadened the scope of the Angel Tax, leading to criticism.

This criticism arose amid a notable downturn in startup funding and subsequent job losses in the sector. These developments highlight the complex interplay between taxation policy and economic growth.

UPSC Insight: Understanding the recent amendments and their economic impact is crucial for GS Paper 3 (Economy). Be prepared to analyze the pros and cons of such tax policies on the startup ecosystem.

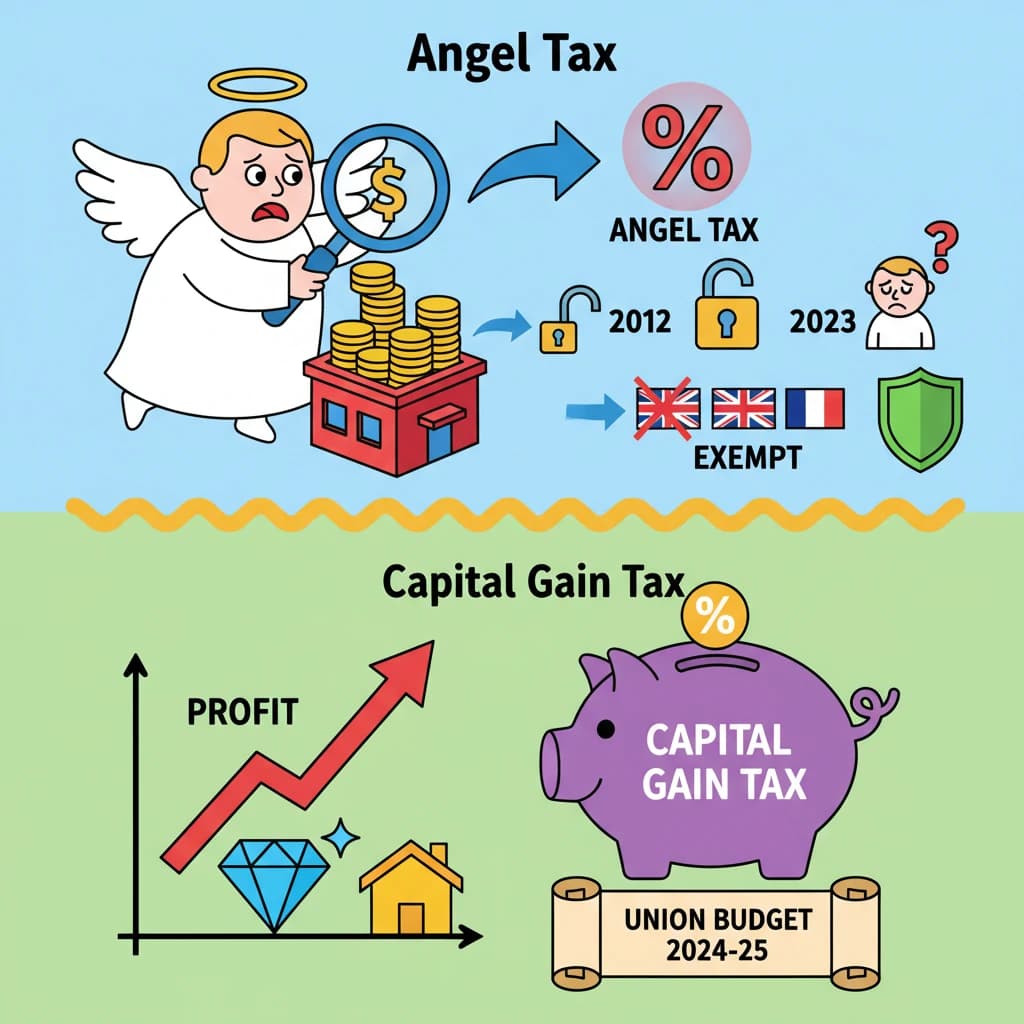

Separately, Capital Gains Tax has also become a focal point, especially with the anticipation of the Union Budget for 2024-25. Its implications for investors and the market are under close scrutiny.

What is Angel Tax?

Definition: Angel Tax is a tax levied on the funds raised by unlisted companies through the issuance of shares in off-market transactions if the issue price exceeds the fair market value (FMV) of the company.

It was initially introduced in 2012. The primary objective behind its introduction was to discourage the generation and utilization of unaccounted money (black money) through investments in closely held companies.

Core Concept: The tax essentially targets the premium received by unlisted companies on share issuance, treating any excess over FMV as taxable income.

Fair Market Value (FMV): This refers to the price of an asset where both the buyer and seller possess reasonable knowledge of its value and are willing to trade without undue pressure or compulsion.

Expansion Under Finance Act, 2023

The Finance Act, 2023, brought significant changes to the Angel Tax provisions. A relevant section of the Income-tax Act was amended to expand its ambit.

Crucially, this expansion included foreign investors within the scope of the Angel Tax provision. This move initially raised concerns among international investors and the startup community.

Exemptions and Industry Pushback

Initially, startups recognized by the Department for Promotion of Industry and Internal Trade (DPIIT) were explicitly excluded from the purview of this provision. This was a measure to support legitimate startups.

However, the inclusion of foreign investors led to considerable industry pushback. Concerns were raised regarding declining foreign direct investment and its potential adverse effects on the Indian startup ecosystem.

Responding to these concerns, the Finance Ministry subsequently announced exemptions. Investors from 21 countries were exempted from the Angel Tax levy for their investments in Indian startups.

- These exempted countries include major global economies such as the United States (US), the United Kingdom (UK), and France.

- This exemption aims to alleviate funding concerns and encourage foreign investment into Indian startups.

💡 Key Takeaways

- •Angel Tax is levied on unlisted companies' share premiums exceeding Fair Market Value (FMV), aiming to curb unaccounted money.

- •Introduced in 2012, its scope was expanded in 2023 to include foreign investors, causing criticism.

- •DPIIT-recognized startups and investors from 21 specific countries (e.g., US, UK, France) are exempted from Angel Tax.

- •Capital Gain Tax is a tax on profits from selling capital assets, gaining attention for the Union Budget 2024-25.

- •These taxes significantly impact startup funding, investor confidence, and India's 'Ease of Doing Business' ranking.

🧠 Memory Techniques

98% Verified Content

📚 Reference Sources

•Income-tax Act, 1961 (Section 56(2)(viib))

•Finance Act, 2023

•Notifications from the Ministry of Finance and DPIIT regarding Angel Tax exemptions