Loading page, please wait…

CBDT to Overhaul Income Tax Act 1961 - UPSC Economy

What is CBDT to Overhaul Income Tax Act 1961 in UPSC Economy?

CBDT to Overhaul Income Tax Act 1961 is a key topic under Economy for UPSC Civil Services Examination. Key points include: CBDT is overhauling the Income Tax Act, 1961, via an internal committee.. The primary goals are simplification and modernization of direct tax laws.. This initiative is mandated by the central government.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is CBDT to Overhaul Income Tax Act 1961 important for UPSC exam?

CBDT to Overhaul Income Tax Act 1961 is a Easy-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of CBDT to Overhaul Income Tax Act 1961, making it essential for comprehensive IAS preparation.

How to prepare CBDT to Overhaul Income Tax Act 1961 for UPSC?

To prepare CBDT to Overhaul Income Tax Act 1961 for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking CBDT to Overhaul Income Tax Act 1961 to related GS Paper topics.

Key takeaways of CBDT to Overhaul Income Tax Act 1961 for UPSC

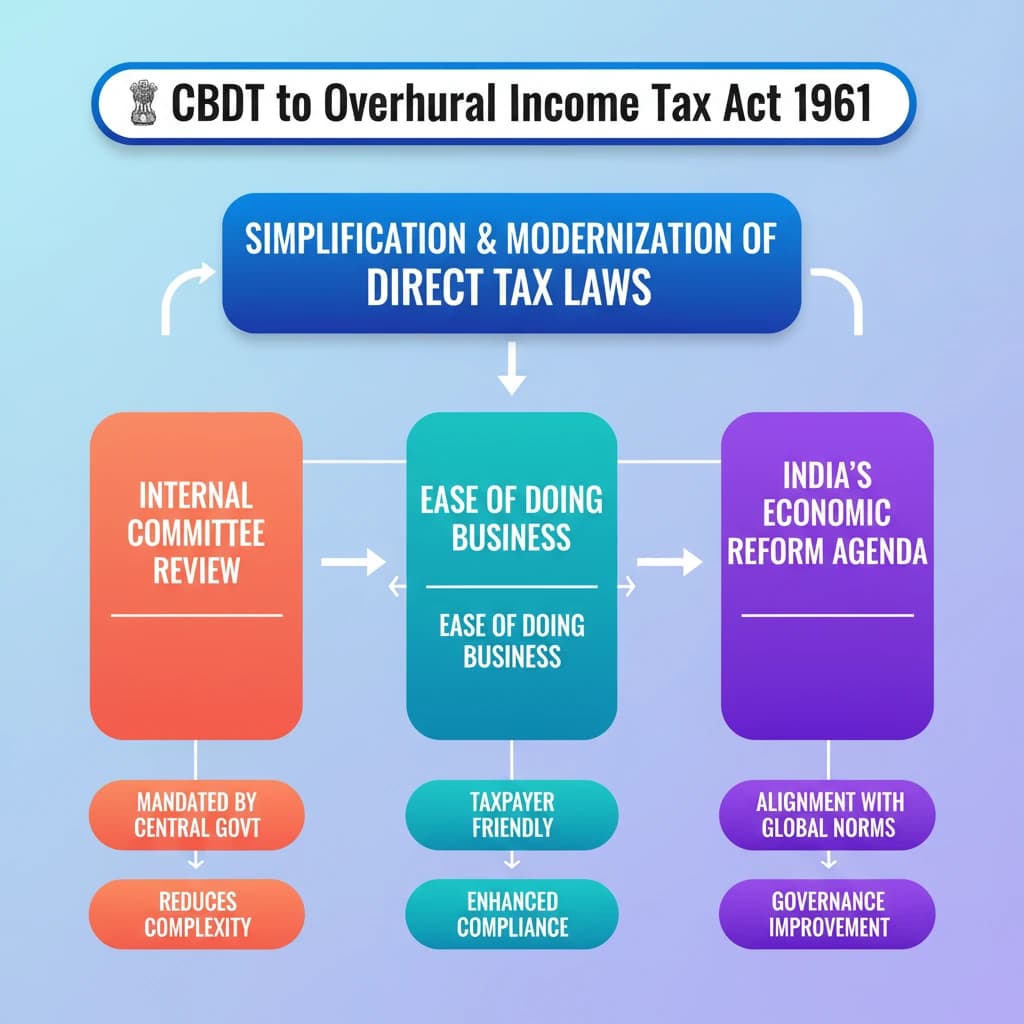

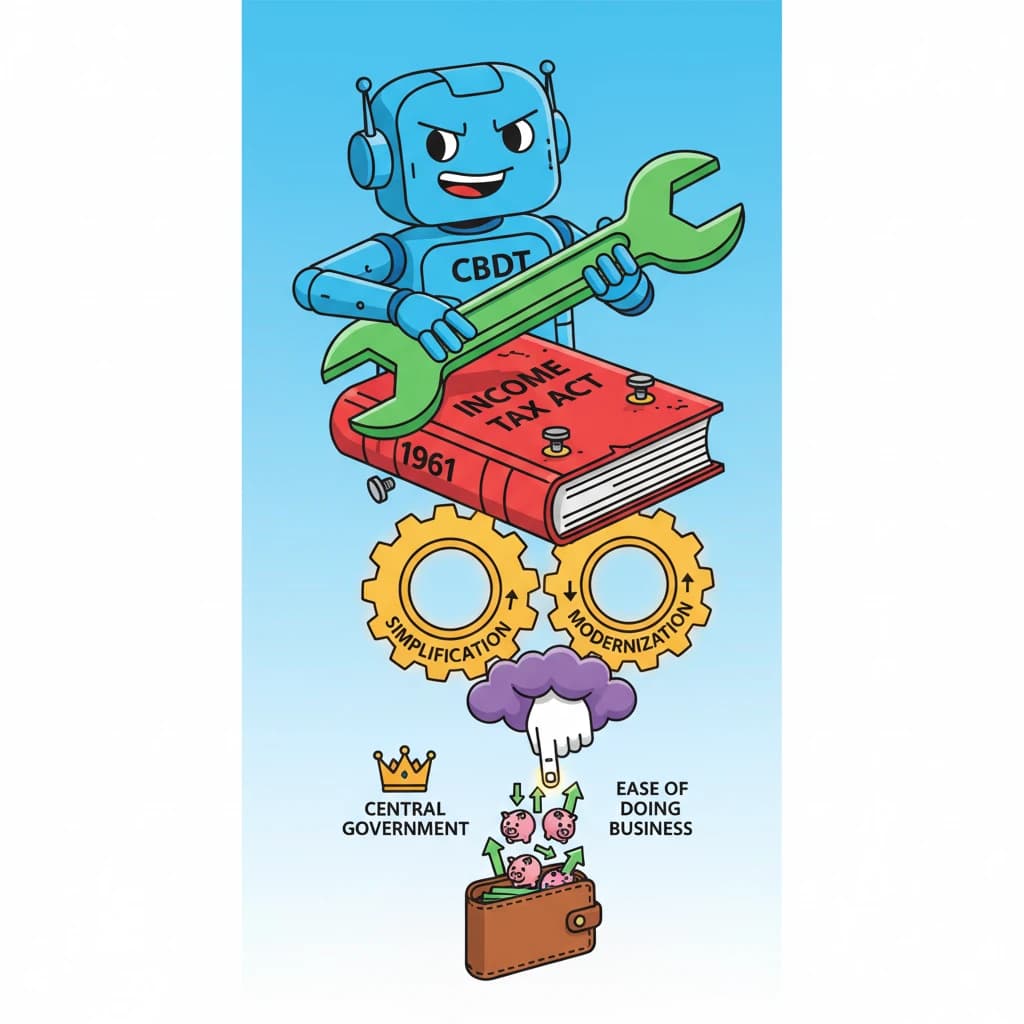

- CBDT is overhauling the Income Tax Act, 1961, via an internal committee.

- The primary goals are simplification and modernization of direct tax laws.

- This initiative is mandated by the central government.

- The overhaul aims to reduce complexity for taxpayers and enhance ease of doing business.

- It aligns with India's broader economic and governance reform agenda.

CBDT to Overhaul Income Tax Act 1961

Easy⏱️ 4 min read

economy

📖 Introduction

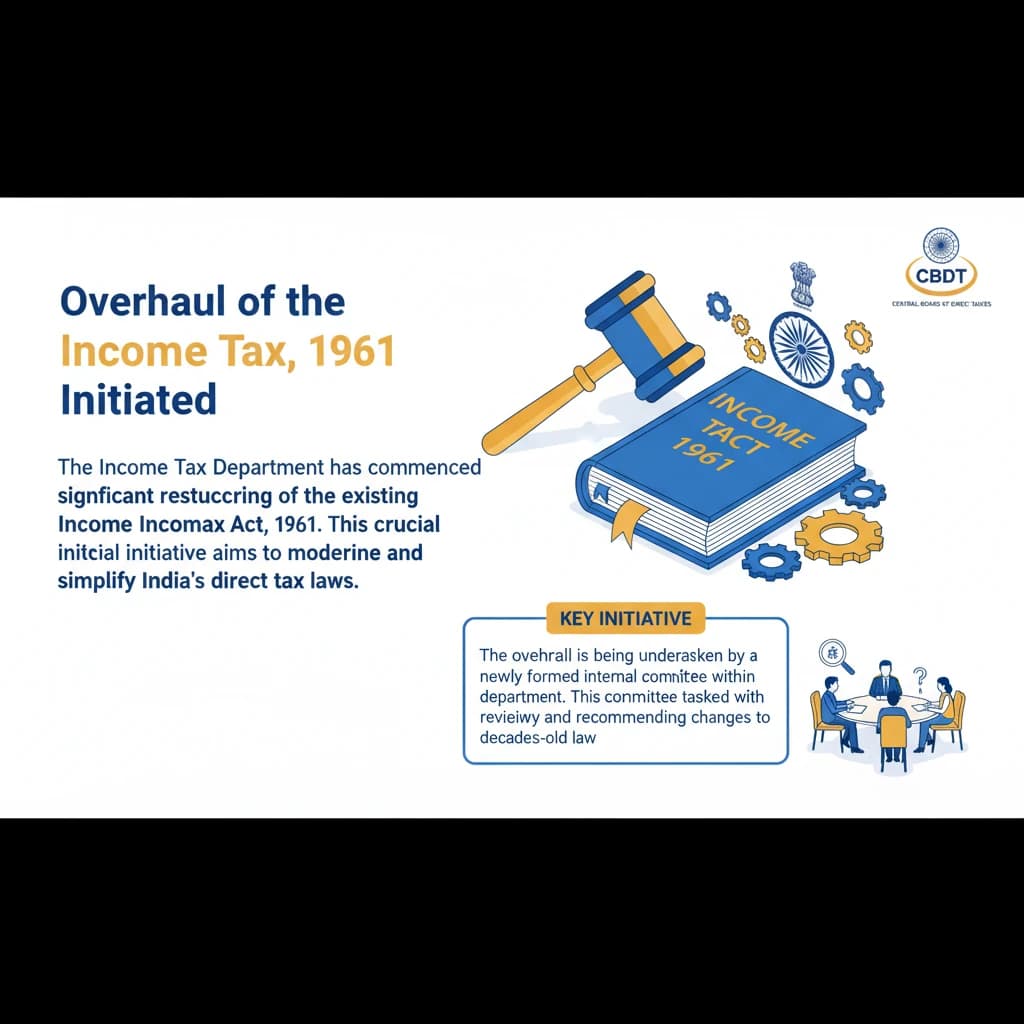

Overhaul of the Income Tax Act, 1961 Initiated

The Income Tax Department has commenced a significant restructuring of the existing Income Tax Act, 1961. This crucial initiative aims to modernize and simplify India’s direct tax laws.

The overhaul is being undertaken by a newly formed internal committee within the department. This committee is tasked with reviewing and recommending changes to the decades-old legislation.

The announcement regarding this overhaul was made by the chairman of the Central Board of Direct Taxes (CBDT). It is a direct response to a central government mandate.

The primary objectives behind this exercise are to ensure the tax laws are simpler to understand and comply with, and to bring them up to date with contemporary economic realities.

UPSC Mains GS Paper 3: This topic is highly relevant for questions on Indian Economy, specifically under Government Budgeting, Tax Reforms, and Ease of Doing Business. Understanding the rationale and potential impact is key.

💡 Key Takeaways

- •CBDT is overhauling the Income Tax Act, 1961, via an internal committee.

- •The primary goals are simplification and modernization of direct tax laws.

- •This initiative is mandated by the central government.

- •The overhaul aims to reduce complexity for taxpayers and enhance ease of doing business.

- •It aligns with India's broader economic and governance reform agenda.

🧠 Memory Techniques

98% Verified Content

📚 Reference Sources

•Basic knowledge of Income Tax Act, 1961 and CBDT functions