Loading page, please wait…

Concerns Over Cess and Surcharges in India - UPSC Economy

What is Concerns Over Cess and Surcharges in India in UPSC Economy?

Concerns Over Cess and Surcharges in India is a key topic under Economy for UPSC Civil Services Examination. Key points include: Cess is a "tax on tax" for specific purposes, not shared with states.. Surcharge is also a "tax on tax," for general purposes, not shared with states.. The 80th Amendment (2000) formally excluded cesses and surcharges from the divisible pool.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Concerns Over Cess and Surcharges in India important for UPSC exam?

Concerns Over Cess and Surcharges in India is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Concerns Over Cess and Surcharges in India, making it essential for comprehensive IAS preparation.

How to prepare Concerns Over Cess and Surcharges in India for UPSC?

To prepare Concerns Over Cess and Surcharges in India for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Concerns Over Cess and Surcharges in India to related GS Paper topics.

Key takeaways of Concerns Over Cess and Surcharges in India for UPSC

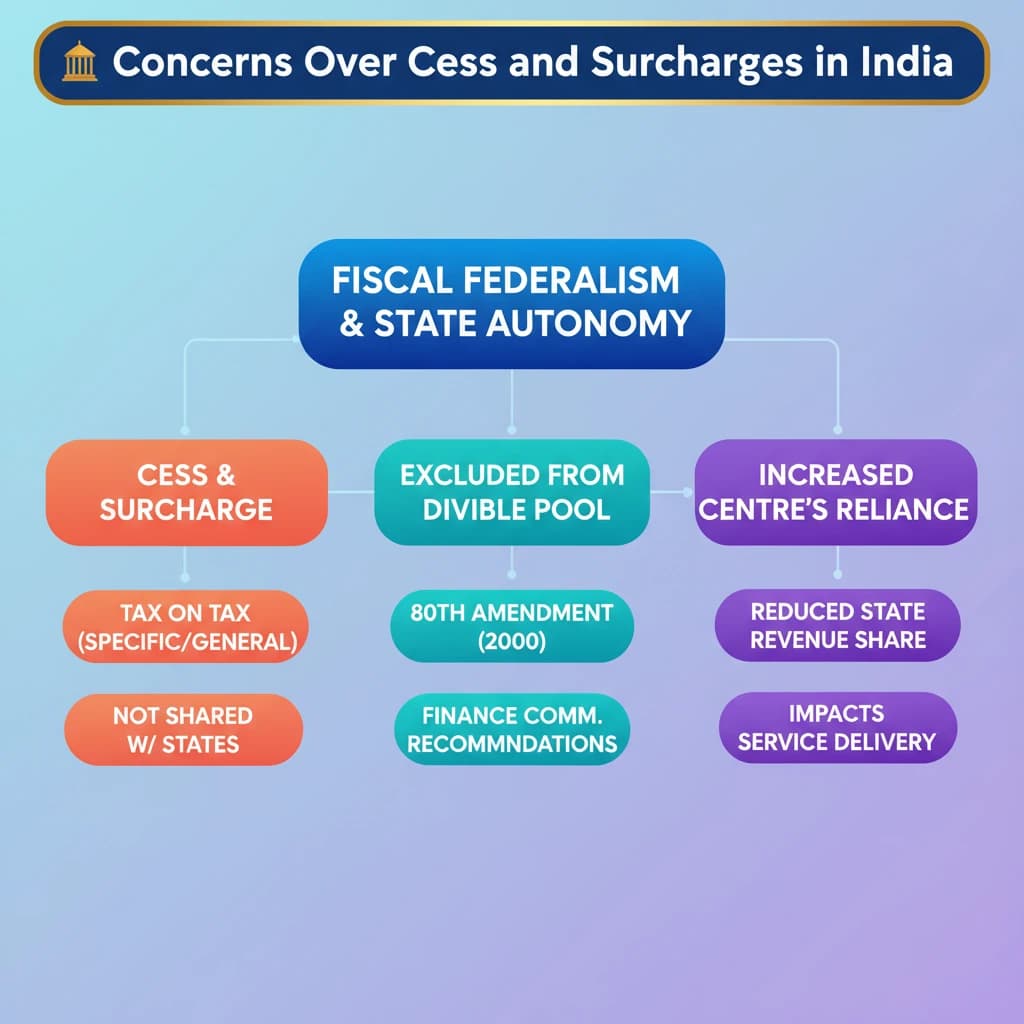

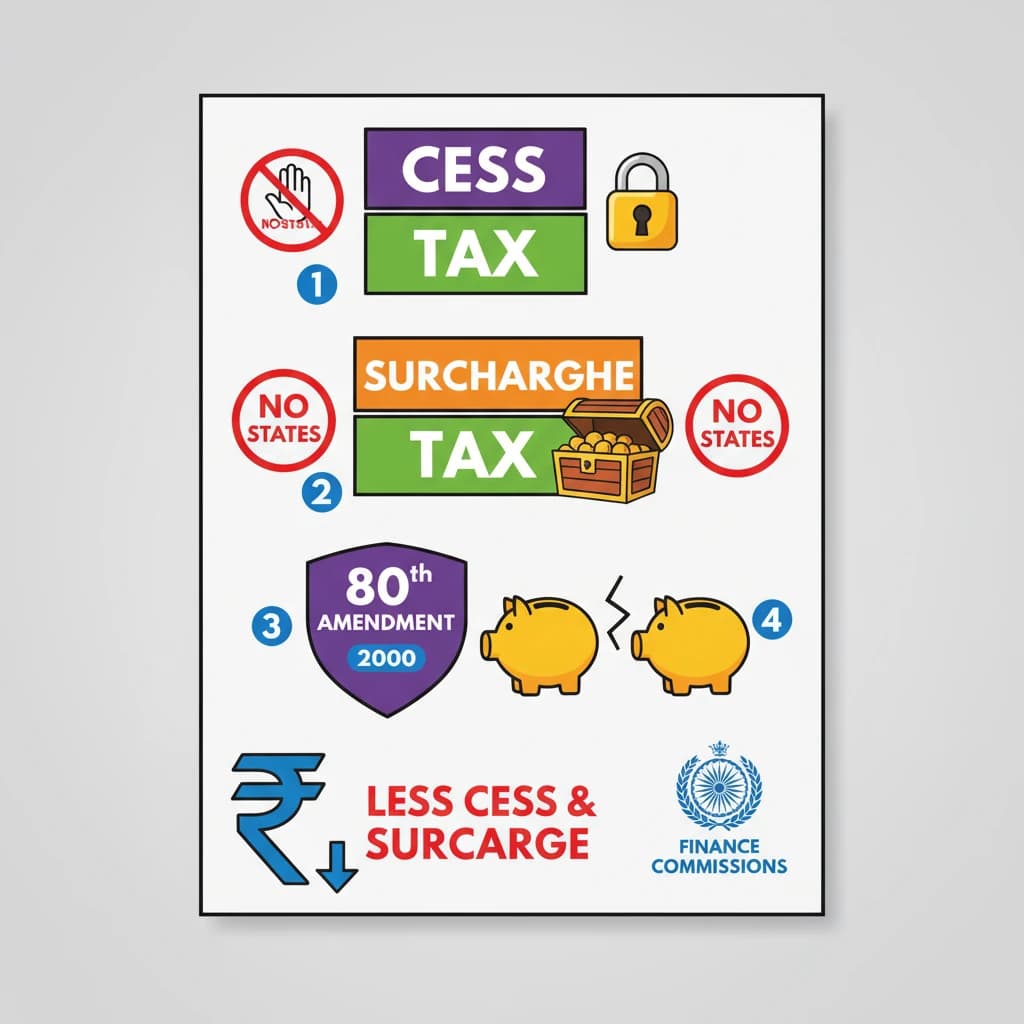

- Cess is a "tax on tax" for specific purposes, not shared with states.

- Surcharge is also a "tax on tax," for general purposes, not shared with states.

- The 80th Amendment (2000) formally excluded cesses and surcharges from the divisible pool.

- Finance Commissions have recommended reducing the Centre's reliance on these levies.

- Increasing reliance on cesses/surcharges raises concerns about fiscal federalism and state autonomy.

Concerns Over Cess and Surcharges in India

Medium⏱️ 8 min read

economy

📖 Introduction

Introduction to Cess and Surcharges

The issue of the Centre's increasing reliance on cesses and surcharges has recently been highlighted by Arvind Panagariya, the Chairman of the 16th Finance Commission. He described this as a "complicated issue" due to its implications for fiscal federalism.

Understanding Cess

A Cess is a specific type of tax levied for a designated purpose. It is essentially a tax on tax, imposed in addition to existing taxes like excise or income tax.

- Earmarked Revenue: The revenue collected from a cess is strictly earmarked for a particular use, meaning it cannot be used for any other purpose.

- Temporary Nature: Cesses are typically charged for a specific time period or until the government accumulates sufficient funds for its intended objective.

An example of this is the Education Cess, which was levied to fund educational initiatives.

Constitutional Basis for Cess

Cesses are recognized under Article 270 of the Indian Constitution, which outlines the revenue-sharing framework between the Union and States.

The 80th Amendment formally amended Article 270. This amendment explicitly excludes cesses and surcharges from the divisible pool of taxes. Consequently, revenue from cesses is not shared with states.

Understanding Surcharge

A Surcharge is another form of additional tax or levy imposed on existing duties or taxes. Similar to a cess, it functions as a "tax on tax".

- Constitutional Basis: Surcharges are discussed under Articles 270 and 271 of the Indian Constitution.

- Impact: Surcharges increase the overall tax liability, particularly for higher-income earners or specific sectors already subject to taxation.

Cess vs. Surcharge: Key Differences

While both cess and surcharge are additional levies and go into the Consolidated Fund of India (CFI), their usage differs significantly.

| Feature | Cess | Surcharge |

|---|---|---|

| Purpose | Earmarked for a specific purpose (e.g., education, infrastructure). | Can be spent like other general taxes for any government expenditure. |

| Divisible Pool | Excluded from the divisible pool; not shared with states. | Excluded from the divisible pool; not shared with states. |

| Constitutional Articles | Primarily Article 270. | Articles 270 and 271. |

Understanding the distinction between cess and surcharge is crucial for UPSC Mains GS Paper 3 (Indian Economy). Pay attention to their constitutional backing and impact on fiscal federalism.

💡 Key Takeaways

- •Cess is a "tax on tax" for specific purposes, not shared with states.

- •Surcharge is also a "tax on tax," for general purposes, not shared with states.

- •The 80th Amendment (2000) formally excluded cesses and surcharges from the divisible pool.

- •Finance Commissions have recommended reducing the Centre's reliance on these levies.

- •Increasing reliance on cesses/surcharges raises concerns about fiscal federalism and state autonomy.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•Indian Constitution (Articles 270, 271)

•Reports of 13th, 14th, 16th Finance Commissions