Loading page, please wait…

Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) - UPSC Economy

What is Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) in UPSC Economy?

Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) is a key topic under Economy for UPSC Civil Services Examination. Key points include: Deposit insurance protects depositors' funds in case of bank failure.. Recent bank crises (PMC, Yes, LVB) highlighted its critical need.. In India, DICGC provides deposit insurance coverage.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) important for UPSC exam?

Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases), making it essential for comprehensive IAS preparation.

How to prepare Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) for UPSC?

To prepare Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) to related GS Paper topics.

Key takeaways of Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases) for UPSC

- Deposit insurance protects depositors' funds in case of bank failure.

- Recent bank crises (PMC, Yes, LVB) highlighted its critical need.

- In India, DICGC provides deposit insurance coverage.

- The insurance cover was recently increased to ₹5 lakh per depositor per bank.

- It is essential for maintaining financial stability and public confidence in the banking system.

Deposit Insurance: Need and Relevance (PMC, Yes Bank Cases)

Medium⏱️ 6 min read

economy

📖 Introduction

Introduction to Deposit Insurance

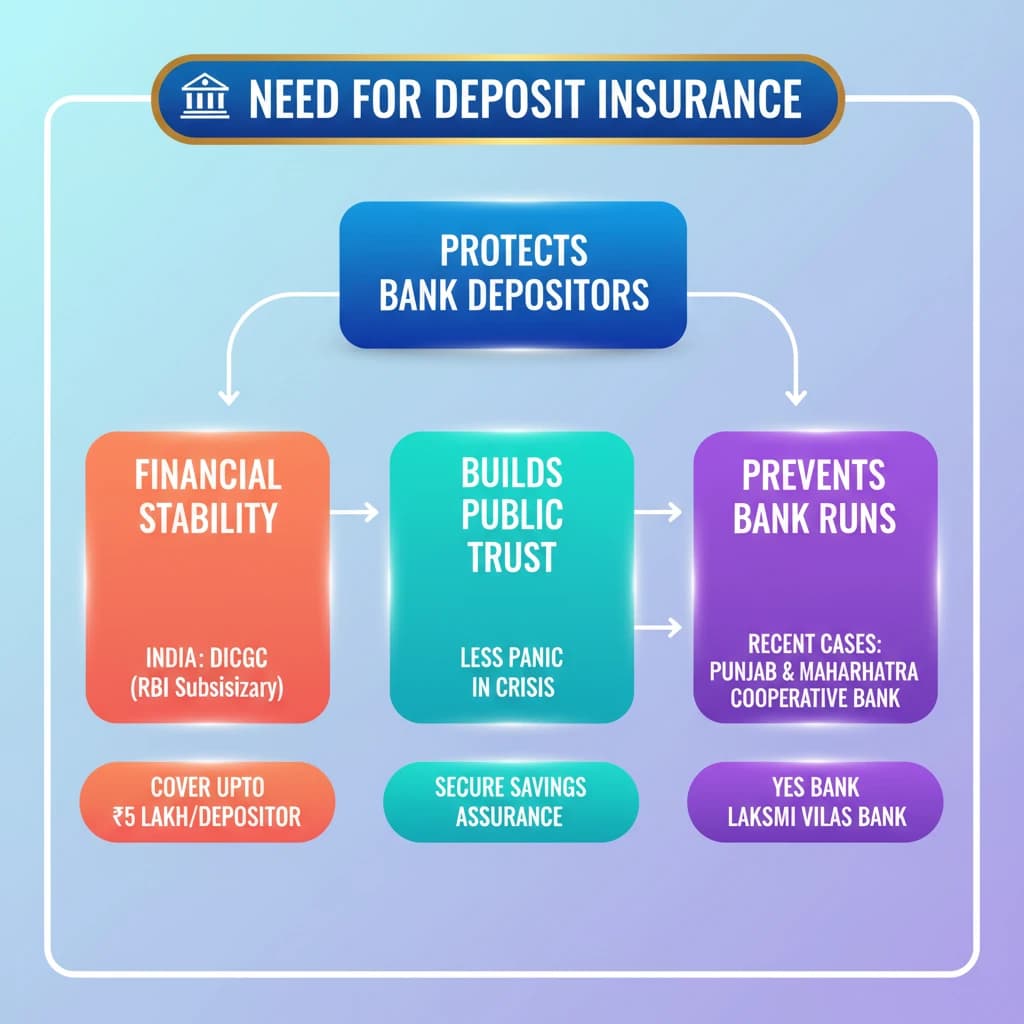

The concept of deposit insurance has gained significant attention, particularly in the wake of recent challenges faced by various banks in India. It serves as a crucial safety net for depositors.

This mechanism is designed to protect depositors' funds, ensuring they can access their money even if a bank faces financial distress or collapses.

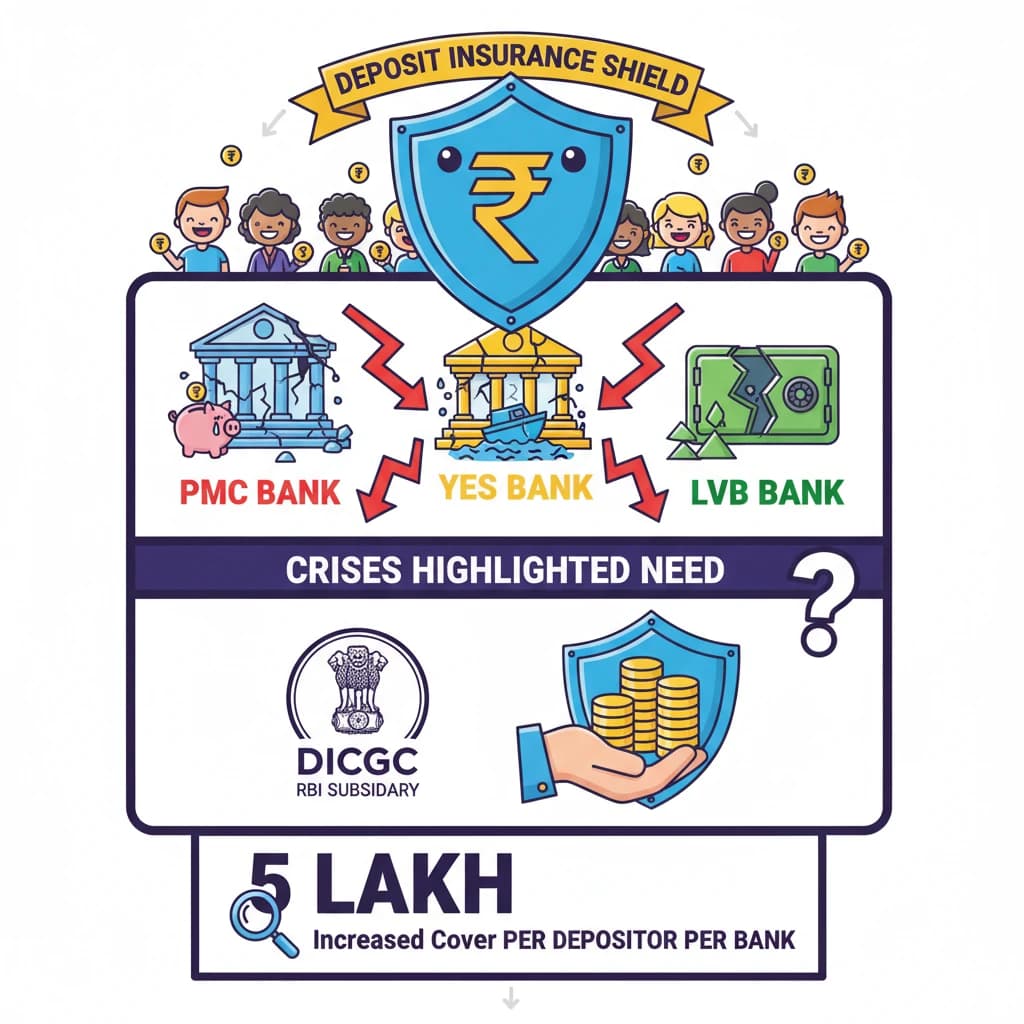

The Need for Deposit Insurance: Recent Cases

The immediate need for robust deposit insurance was sharply highlighted by difficulties experienced by depositors in accessing their funds from several banks.

These incidents underscored the vulnerability of public savings and the critical role of an effective insurance system to maintain public trust in the banking sector.

Recent cases that brought deposit insurance into the spotlight include:

- Punjab & Maharashtra Co-operative (PMC) Bank

- Yes Bank

- Lakshmi Vilas Bank

Impact on Depositors

In these instances, depositors faced significant hurdles and delays in withdrawing their own money. This created widespread panic and eroded confidence in the stability of financial institutions.

The situations at PMC Bank, Yes Bank, and Lakshmi Vilas Bank demonstrated that even regulated entities can face severe liquidity or solvency issues, directly impacting ordinary citizens.

Key Point: The troubles faced by depositors in these banks made the subject of deposit insurance a central topic of discussion regarding financial security and consumer protection.

Maintaining Financial Stability

A strong deposit insurance system is vital for preventing systemic risks. It assures depositors that their money is safe, thereby preventing bank runs and maintaining overall financial stability.

Without such a safety net, any perceived weakness in a bank could trigger mass withdrawals, potentially leading to a cascading failure across the banking system.

UPSC Insight: Understanding the 'Need' of deposit insurance is crucial for GS Paper III (Indian Economy). Focus on the underlying reasons, recent examples, and its role in financial stability and consumer confidence. Link it to the role of DICGC.

💡 Key Takeaways

- •Deposit insurance protects depositors' funds in case of bank failure.

- •Recent bank crises (PMC, Yes, LVB) highlighted its critical need.

- •In India, DICGC provides deposit insurance coverage.

- •The insurance cover was recently increased to ₹5 lakh per depositor per bank.

- •It is essential for maintaining financial stability and public confidence in the banking system.

🧠 Memory Techniques

98% Verified Content

📚 Reference Sources

•Reserve Bank of India (RBI) official communications

•Deposit Insurance and Credit Guarantee Corporation (DICGC) official website

•Union Budget 2020-21 documents