Loading page, please wait…

India’s Taxation System - UPSC Economy

What is India’s Taxation System in UPSC Economy?

India’s Taxation System is a key topic under Economy for UPSC Civil Services Examination. Key points include: Taxes are mandatory government levies to fund public services, without direct quid pro quo.. India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).. Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is India’s Taxation System important for UPSC exam?

India’s Taxation System is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of India’s Taxation System, making it essential for comprehensive IAS preparation.

How to prepare India’s Taxation System for UPSC?

To prepare India’s Taxation System for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking India’s Taxation System to related GS Paper topics.

Key takeaways of India’s Taxation System for UPSC

- Taxes are mandatory government levies to fund public services, without direct quid pro quo.

- India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).

- Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).

- Key Indirect Tax: Goods and Services Tax (GST), a consumption-based, value-added tax.

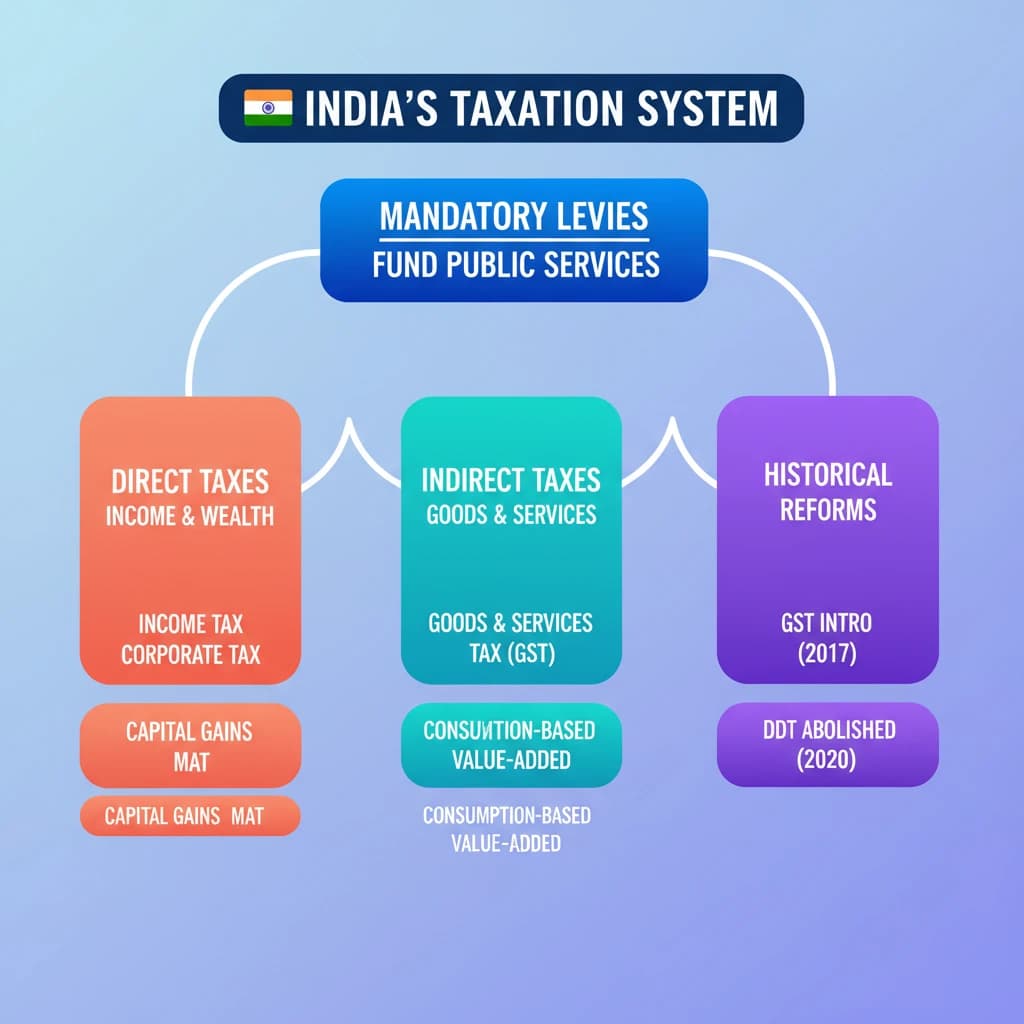

- Historical reforms include the abolition of FBT/BCTT (2009) and DDT (2020), and the introduction of GST (2017).

- The current GST framework's impact on growth, business, consumption, and investment reputation is a key area of discussion.

India’s Taxation System

Medium⏱️ 8 min read

economy

📖 Introduction

Introduction to India's Taxation System

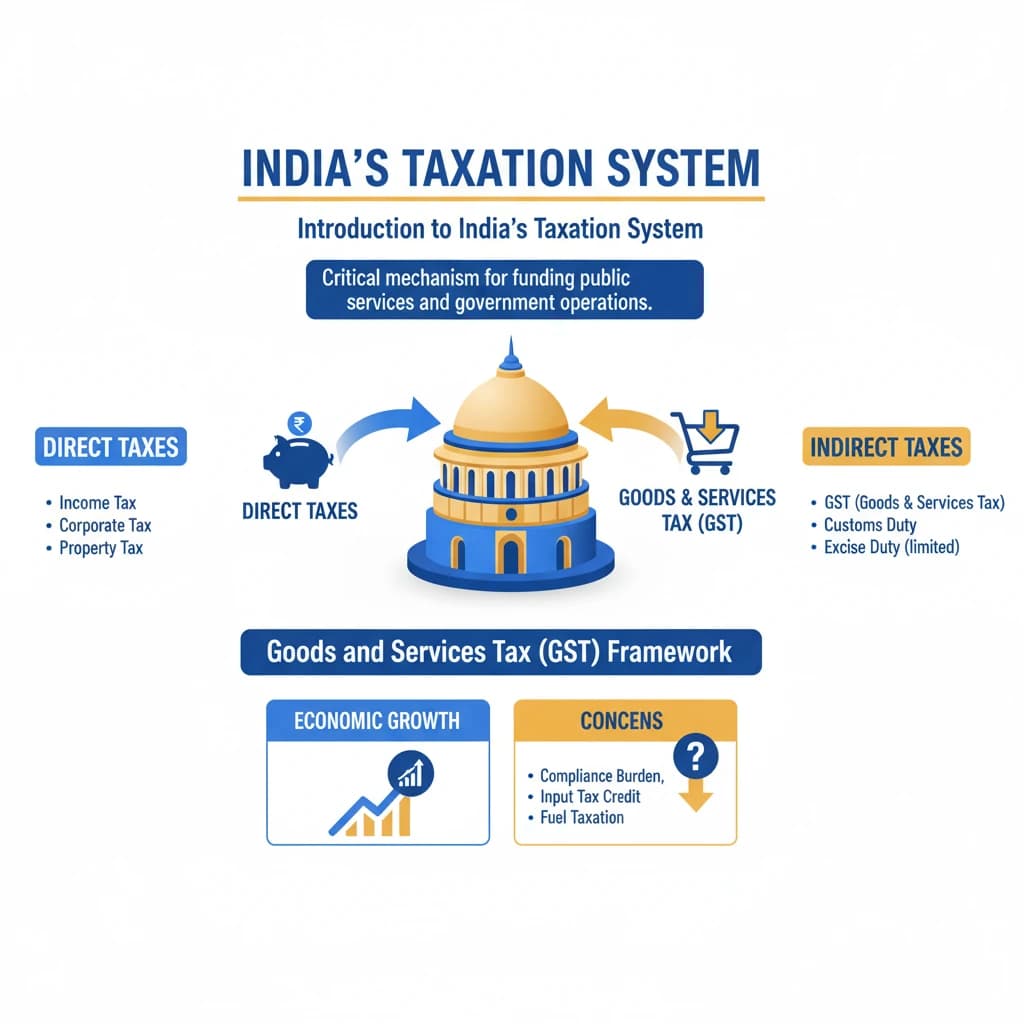

India's taxation system is a critical mechanism for funding public services and government operations. It comprises a mix of direct and indirect taxes, designed to collect revenue from various economic activities.

The contemporary system, particularly under the Goods and Services Tax (GST) framework, faces scrutiny regarding its impact on economic growth. Concerns include potential hindrances to business development, suppression of consumption, and damage to India's investment reputation.

Understanding the structure and impact of India's taxation system is vital for UPSC Mains GS Paper III (Economy). Focus on both the theoretical aspects and their real-world implications.

Understanding Taxes: The Core Concept

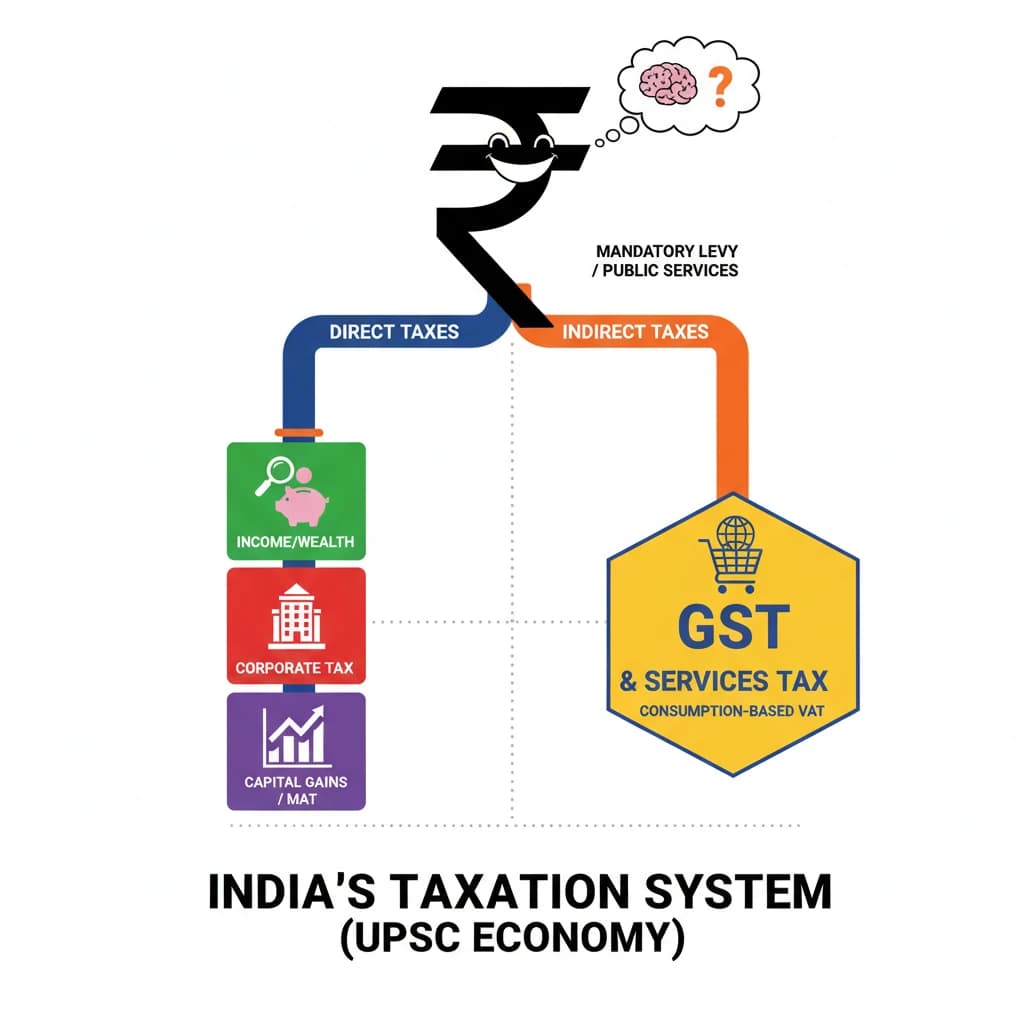

Definition of Tax: Taxes are mandatory financial charges or levies imposed by a government on individuals, businesses, or property. Their primary purpose is to fund public services and government operations.

A key characteristic of taxation is the absence of a direct quid pro quo. This means there is no direct, immediate exchange of goods or services between the taxpayer and the public authority for the tax paid.

Direct Taxes in India

Direct taxes are levied directly on the income or wealth of individuals and corporations. The burden of these taxes cannot be shifted to another person.

- Income Tax: This tax is imposed on an individual's income. It is generally progressive in nature, meaning higher income earners pay a larger percentage of their income as tax, with different slabs for various taxpayer categories.

- Capital Gains Tax: This tax is levied on the profit or gain realized from the sale of an investment or property. Different rates apply for short-term and long-term holdings, depending on the asset's holding period.

- Securities Transaction Tax (STT): A tax imposed on transactions involving the purchase and sale of securities traded on recognized stock exchanges.

- Perquisite Tax: This refers to the tax on benefits or amenities provided by an employer to employees, often in addition to their salary. Examples include company-provided housing or cars.

- Corporate Tax: This is the tax paid by companies on their net earnings or profits. Like income tax, it often features different slabs or rates based on the company's income level.

- Minimum Alternative Tax (MAT): Introduced to ensure that profitable companies, which might otherwise pay little or no tax due to various exemptions and incentives, pay a minimum amount of tax. Currently, MAT is set at 18.5% of book profits.

Abolished Direct Taxes:

- Fringe Benefit Tax (FBT): A tax on non-cash benefits provided by employers, abolished in 2009.

- Dividend Distribution Tax (DDT): A tax levied on companies distributing dividends, abolished in 2020.

- Banking Cash Transaction Tax (BCTT): A tax on certain banking transactions, abolished in 2009.

Indirect Taxes in India

Indirect taxes are levied on goods and services, and their burden can be shifted from the payer to the consumer. These taxes are typically included in the price of goods and services.

- Goods and Services Tax (GST): This is a comprehensive, multi-stage, destination-based consumption tax. It is an ad valorem tax, meaning it is levied as a percentage of the value, and is applied at each stage of the supply chain on the value addition.

- Value Added Tax (VAT): Prior to GST, VAT was a major indirect tax on goods sold. It was also applied at each stage of the supply chain, taxing only the value added at that stage.

The shift from multiple indirect taxes (like VAT, excise duty, service tax) to GST was a landmark reform aimed at simplifying the tax structure and reducing the cascading effect of taxes.

💡 Key Takeaways

- •Taxes are mandatory government levies to fund public services, without direct quid pro quo.

- •India's system includes Direct Taxes (on income/wealth) and Indirect Taxes (on goods/services).

- •Key Direct Taxes: Income Tax, Corporate Tax, Capital Gains Tax, Minimum Alternative Tax (MAT).

- •Key Indirect Tax: Goods and Services Tax (GST), a consumption-based, value-added tax.

- •Historical reforms include the abolition of FBT/BCTT (2009) and DDT (2020), and the introduction of GST (2017).

- •The current GST framework's impact on growth, business, consumption, and investment reputation is a key area of discussion.

🧠 Memory Techniques

95% Verified Content