Loading page, please wait…

Microfinance Institutions - UPSC Economy

What is Microfinance Institutions in UPSC Economy?

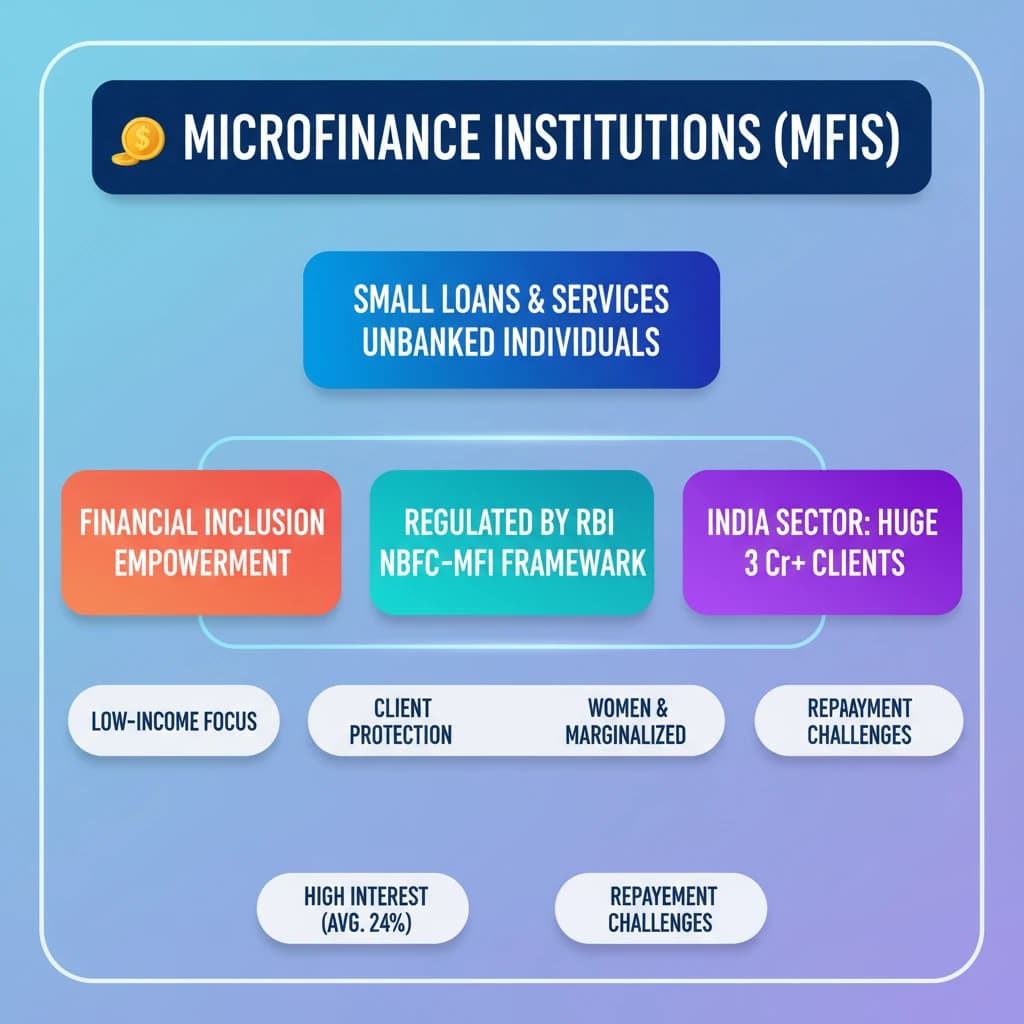

Microfinance Institutions is a key topic under Economy for UPSC Civil Services Examination. Key points include: MFIs provide small loans and financial services to low-income, unbanked individuals, promoting self-sufficiency.. Their core goal is financial inclusion, particularly empowering marginalized groups and women.. MFIs are regulated by the RBI under the 2014 NBFC-MFI framework, which covers client protection and credit pricing.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Microfinance Institutions important for UPSC exam?

Microfinance Institutions is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Microfinance Institutions, making it essential for comprehensive IAS preparation.

How to prepare Microfinance Institutions for UPSC?

To prepare Microfinance Institutions for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Microfinance Institutions to related GS Paper topics.

Key takeaways of Microfinance Institutions for UPSC

- MFIs provide small loans and financial services to low-income, unbanked individuals, promoting self-sufficiency.

- Their core goal is financial inclusion, particularly empowering marginalized groups and women.

- MFIs are regulated by the RBI under the 2014 NBFC-MFI framework, which covers client protection and credit pricing.

- India's microfinance sector is significant, with 184 MFIs serving over 3 crore clients across 29 States and 4 UTs.

- Key challenges include high interest rates (avg. 24%), high processing fees, and non-compliance in assessing borrower repayment capacity.

- There is a crucial need to balance financial outreach with responsible lending practices and robust regulatory oversight.

Microfinance Institutions

Medium⏱️ 7 min read

economy

📖 Introduction

Introduction to Microfinance Institutions (MFIs)

The Financial Services Secretary has highlighted the critical role of Microfinance Institutions (MFIs) in advancing financial inclusion across the country.

Despite their significant positive impact, the Secretary stressed the importance of avoiding reckless lending practices by these institutions to ensure sustainable growth.

Understanding Microfinance Institutions

Definition: MFIs are financial companies that extend small loans and provide other financial services.

They cater specifically to individuals and groups who typically lack access to conventional banking facilities.

The primary objective of microfinance is to empower low-income and unemployed individuals, helping them achieve self-sufficiency.

MFIs serve as a vital instrument for financial inclusion, particularly benefiting marginalized groups and women, thereby fostering social equity and empowerment.

Regulatory Framework for MFIs in India

The Reserve Bank of India (RBI) is the primary regulator for MFIs in India, ensuring systematic operation and client protection.

Regulation is carried out under the NBFC-MFI framework, which was established in 2014 to formalize oversight.

The NBFC-MFI framework covers crucial aspects such as:

- Client protection and borrower safeguards.

- Ensuring privacy of clients' financial data.

- Guidelines for transparent credit pricing and fee structures.

Current Status and Growth of MFIs in India

The microfinance sector in India has experienced substantial growth, becoming a significant component of the financial landscape.

Currently, there are 184 Microfinance Institutions (MFIs) operating across a wide geographical expanse in the country.

Geographical Reach: MFIs are present in:

- 29 States

- 4 Union Territories

- 563 districts

These institutions collectively serve a vast client base of over 3 crore individuals, demonstrating their extensive outreach.

Challenges and Scrutiny Faced by MFIs

Many MFIs have come under scrutiny due to concerns regarding their lending practices, particularly concerning cost to borrowers.

One major issue is the charging of excessive interest rates, which average around 24% per annum, making repayments challenging for the poor.

Concerns also include high processing fees and instances of non-compliance in accurately assessing borrowers’ income and repayment capacities, potentially leading to over-indebtedness.

A report by Sa-Dhan indicates that minor reductions in interest rates would not significantly alleviate the repayment burden for low-income households, suggesting deeper structural issues.

UPSC often asks about the challenges of financial inclusion and the role of various institutions. Understanding the dual role of MFIs – promoting inclusion while facing scrutiny – is crucial for a balanced answer in GS Paper III (Economy).

💡 Key Takeaways

- •MFIs provide small loans and financial services to low-income, unbanked individuals, promoting self-sufficiency.

- •Their core goal is financial inclusion, particularly empowering marginalized groups and women.

- •MFIs are regulated by the RBI under the 2014 NBFC-MFI framework, which covers client protection and credit pricing.

- •India's microfinance sector is significant, with 184 MFIs serving over 3 crore clients across 29 States and 4 UTs.

- •Key challenges include high interest rates (avg. 24%), high processing fees, and non-compliance in assessing borrower repayment capacity.

- •There is a crucial need to balance financial outreach with responsible lending practices and robust regulatory oversight.

🧠 Memory Techniques

100% Verified Content