Loading page, please wait…

NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension - UPSC Economy

What is NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension in UPSC Economy?

NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension is a key topic under Economy for UPSC Civil Services Examination. Key points include: NPS is a market-linked, defined contribution pension scheme introduced on January 1, 2004.. It replaced the Old Pension Scheme (OPS) to address unsustainable government pension liabilities.. NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) under the PFRDA Act, 2013.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension important for UPSC exam?

NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension, making it essential for comprehensive IAS preparation.

How to prepare NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension for UPSC?

To prepare NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension to related GS Paper topics.

Key takeaways of NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension for UPSC

- NPS is a market-linked, defined contribution pension scheme introduced on January 1, 2004.

- It replaced the Old Pension Scheme (OPS) to address unsustainable government pension liabilities.

- NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) under the PFRDA Act, 2013.

- Employees contribute 10% of basic pay + DA, and the government contributes 14% to NPS.

- Unlike OPS, NPS does not guarantee a fixed pension; benefits depend on market performance.

- It aims for fiscal prudence and provides a structured retirement savings avenue.

NPS vs. UPS: Features, Lump Sum Payments & Minimum Pension

Medium⏱️ 8 min read

economy

📖 Introduction

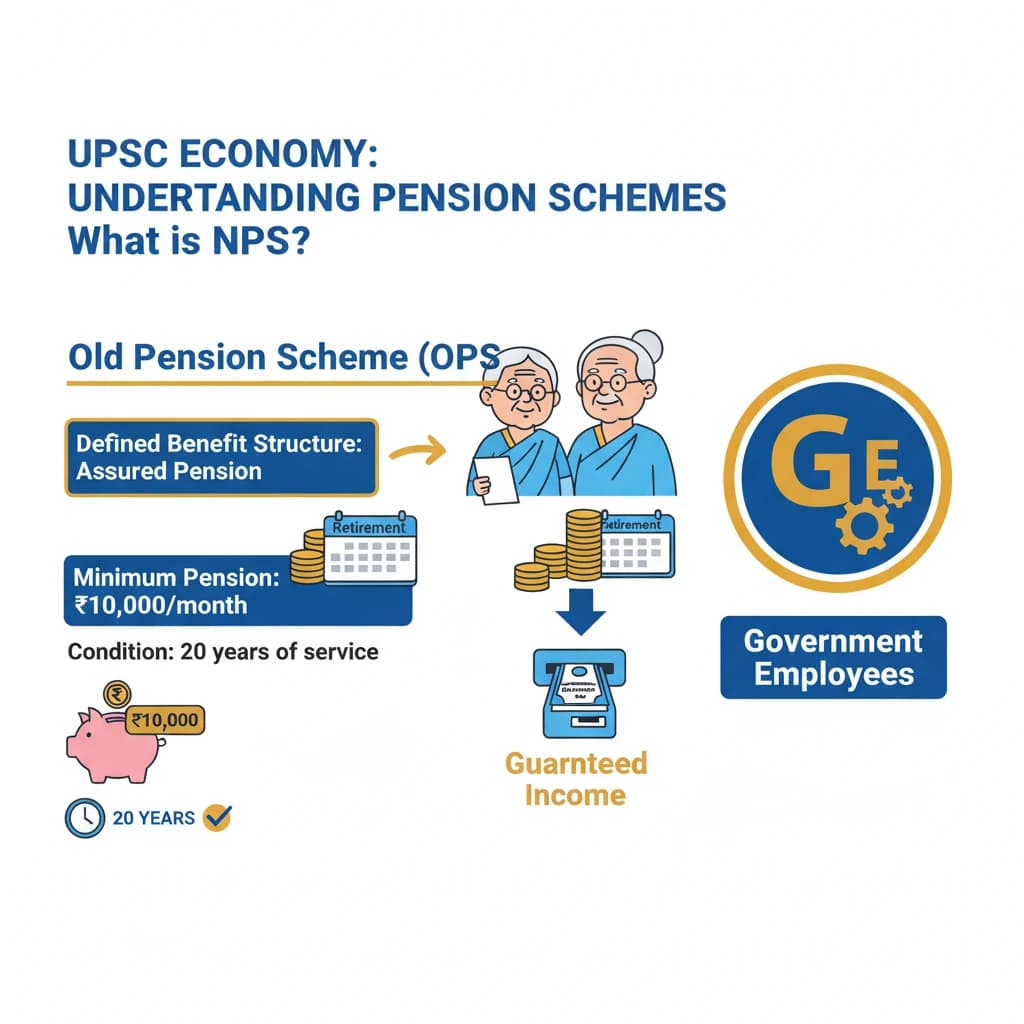

Understanding the Old Pension Scheme (OPS)

The Old Pension Scheme (OPS) was a traditional pension system that offered assured benefits to government employees upon retirement. It was characterized by a defined benefit structure, meaning the pension amount was predetermined and guaranteed.

Under the OPS, the minimum pension offered per month was Rs 10,000 at the time of retirement, provided an employee had completed a 10-year minimum service. Prior to this, the minimum amount was Rs 9,000 after the same service period.

Another feature of OPS was the provision for lump sum payments. Employees could commute up to 40% of their pension into a lump sum, which would, however, reduce their subsequent monthly pension amount.

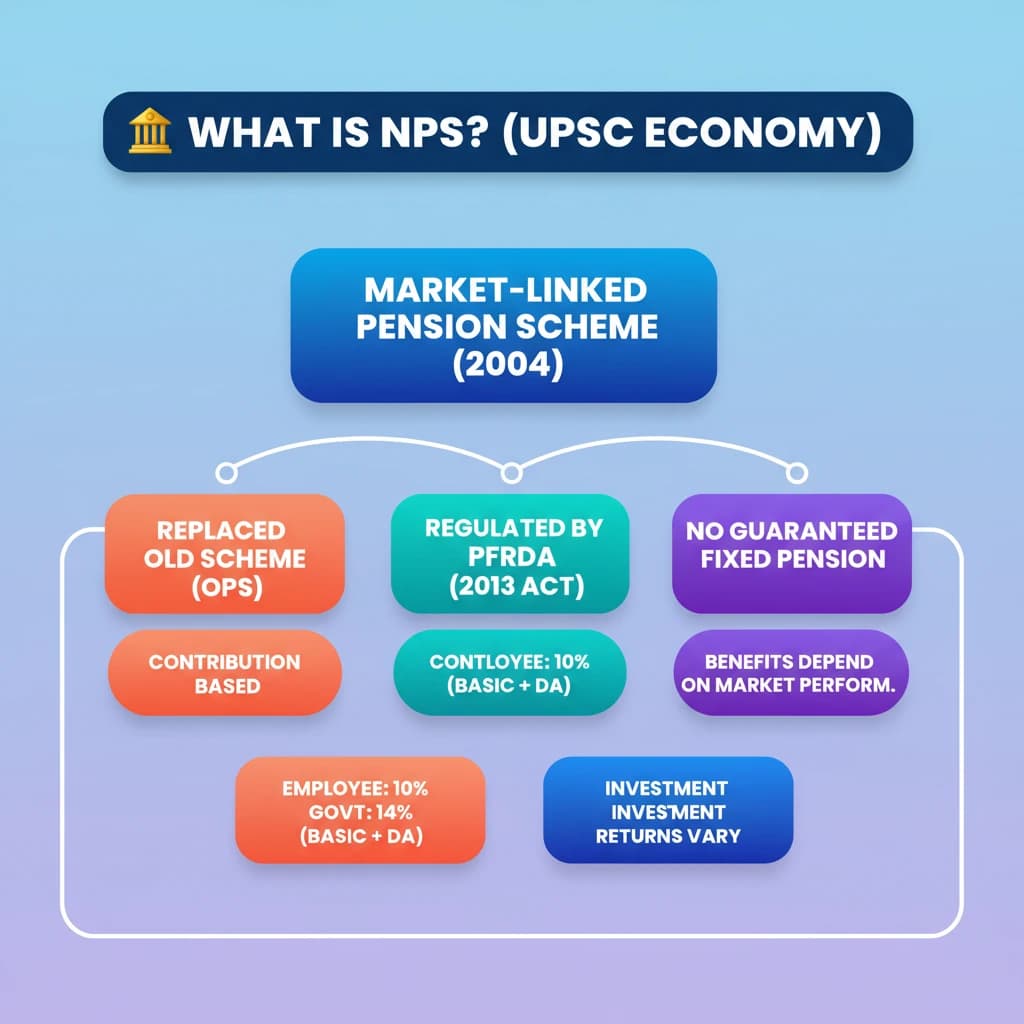

Introduction to the National Pension System (NPS)

The National Pension System (NPS) is a market-linked contribution scheme introduced by the Central Government. Its primary objective is to help individuals secure a regular income in the form of a pension to meet their retirement needs.

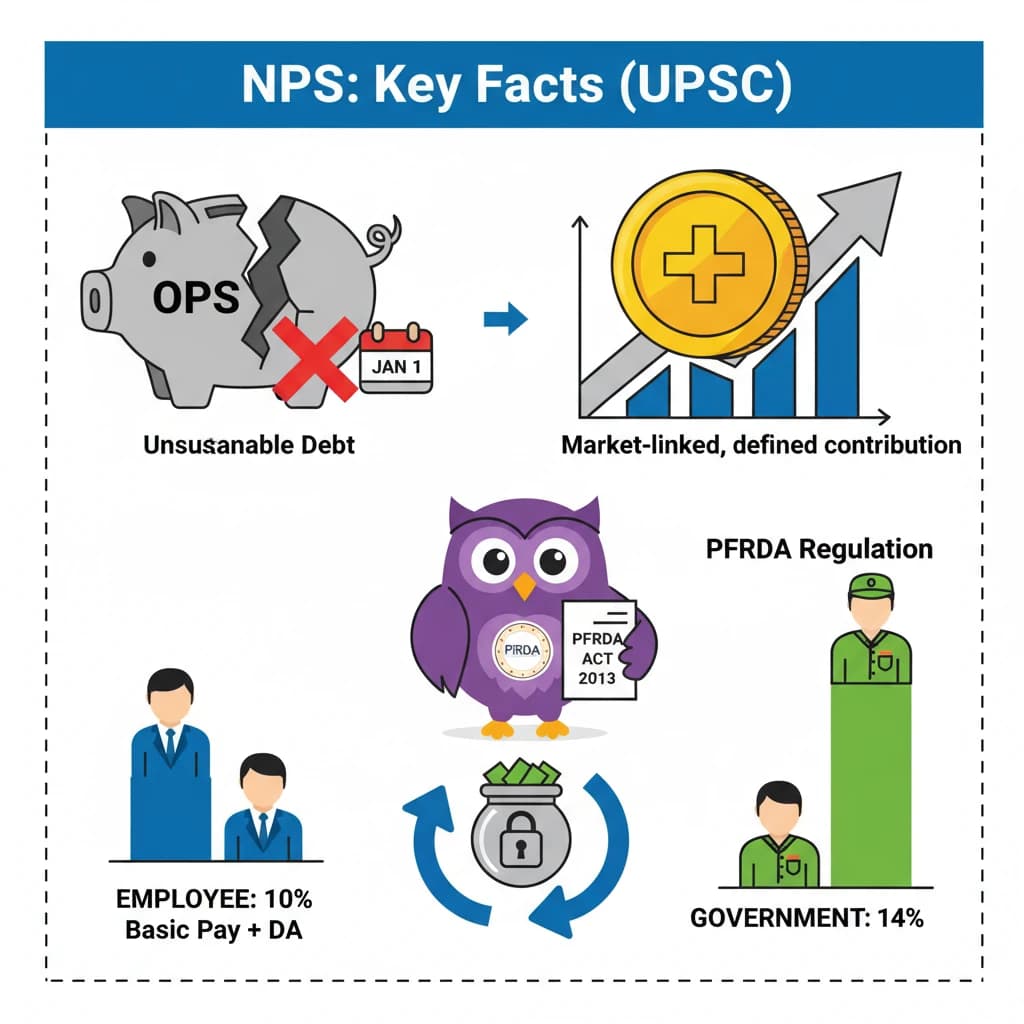

The NPS officially replaced the Old Pension Scheme (OPS) on 1st January, 2004. This reform was part of the Central Government's broader efforts to modernize India's pension policies and ensure fiscal sustainability.

The Pension Fund Regulatory and Development Authority (PFRDA) is the regulatory body responsible for administering and overseeing the NPS. Its powers and functions are defined under the PFRDA Act, 2013.

Need for the National Pension System (NPS)

The transition to NPS was necessitated by a fundamental problem inherent in the Old Pension Scheme (OPS). The OPS was an unfunded scheme, meaning there was no dedicated corpus or fund specifically earmarked for pension payments.

Over time, this lack of a dedicated fund led to a significant increase in the government's pension liability. This escalating liability began to reach fiscally unsustainable levels, posing a substantial burden on public finances.

The pension liabilities of the Central Government witnessed a dramatic increase, jumping from Rs 3,272 crore in 1990-91 to a staggering Rs 1,90,886 crore in 2020-21, highlighting the urgent need for reform.

Working Mechanism of NPS

The National Pension System (NPS) fundamentally differs from the Old Pension Scheme (OPS) in two critical aspects. These differences address the core issues that made OPS unsustainable.

- No Assured Pension: Unlike OPS, NPS does away with an assured or defined pension. The final pension amount depends on the market performance of the invested contributions.

- Funded by Contributions: NPS is a defined contribution scheme. It is funded by contributions from both the employee and the government, creating a dedicated corpus for retirement.

Under the NPS, the employee's contribution is a defined percentage of their basic pay and dearness allowance. The government also makes a matching contribution to the employee's pension account.

The defined contribution structure typically involves 10% of the basic pay and dearness allowance contributed by the employee. The government's contribution is higher, at 14% of the employee's basic pay and dearness allowance.

Understanding the transition from OPS to NPS and its fiscal implications is crucial for UPSC Mains GS Paper 3 (Economy). Focus on the reasons for reform and the structural differences.

💡 Key Takeaways

- •NPS is a market-linked, defined contribution pension scheme introduced on January 1, 2004.

- •It replaced the Old Pension Scheme (OPS) to address unsustainable government pension liabilities.

- •NPS is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) under the PFRDA Act, 2013.

- •Employees contribute 10% of basic pay + DA, and the government contributes 14% to NPS.

- •Unlike OPS, NPS does not guarantee a fixed pension; benefits depend on market performance.

- •It aims for fiscal prudence and provides a structured retirement savings avenue.

🧠 Memory Techniques

98% Verified Content