Loading page, please wait…

RBI Guidelines Related to Microfinance Lending (2022) - UPSC Economy

What is RBI Guidelines Related to Microfinance Lending (2022) in UPSC Economy?

RBI Guidelines Related to Microfinance Lending (2022) is a key topic under Economy for UPSC Civil Services Examination. Key points include: Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.. Lenders must implement policies for flexible repayment and robust household income assessment.. The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is RBI Guidelines Related to Microfinance Lending (2022) important for UPSC exam?

RBI Guidelines Related to Microfinance Lending (2022) is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of RBI Guidelines Related to Microfinance Lending (2022), making it essential for comprehensive IAS preparation.

How to prepare RBI Guidelines Related to Microfinance Lending (2022) for UPSC?

To prepare RBI Guidelines Related to Microfinance Lending (2022) for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking RBI Guidelines Related to Microfinance Lending (2022) to related GS Paper topics.

Key takeaways of RBI Guidelines Related to Microfinance Lending (2022) for UPSC

- Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.

- Lenders must implement policies for flexible repayment and robust household income assessment.

- The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.

- NBFC-MFIs must maintain 75% of their assets as microfinance loans (down from 85%).

- Entities are mandated to report income discrepancies and household income.

- No pre-payment penalties are allowed, and late fees apply only to the overdue amount.

- The guidelines aim for regulatory harmonization and enhanced borrower protection across all regulated entities.

RBI Guidelines Related to Microfinance Lending (2022)

Medium⏱️ 8 min read

economy

📖 Introduction

Introduction to RBI Microfinance Guidelines 2022

The Reserve Bank of India (RBI) introduced comprehensive guidelines for microfinance lending in March 2022. These guidelines aimed to create a harmonized regulatory framework for all regulated entities involved in microfinance, promoting greater transparency and borrower protection.

The objective was to ensure a level playing field across different types of lenders, including NBFC-MFIs, banks, and other financial institutions, while safeguarding the interests of vulnerable borrowers.

UPSC Relevance: These guidelines are crucial for GS Paper III (Indian Economy), particularly topics related to financial sector reforms, financial inclusion, and the role of regulatory bodies like the RBI.

Eligibility for Collateral-Free Loans

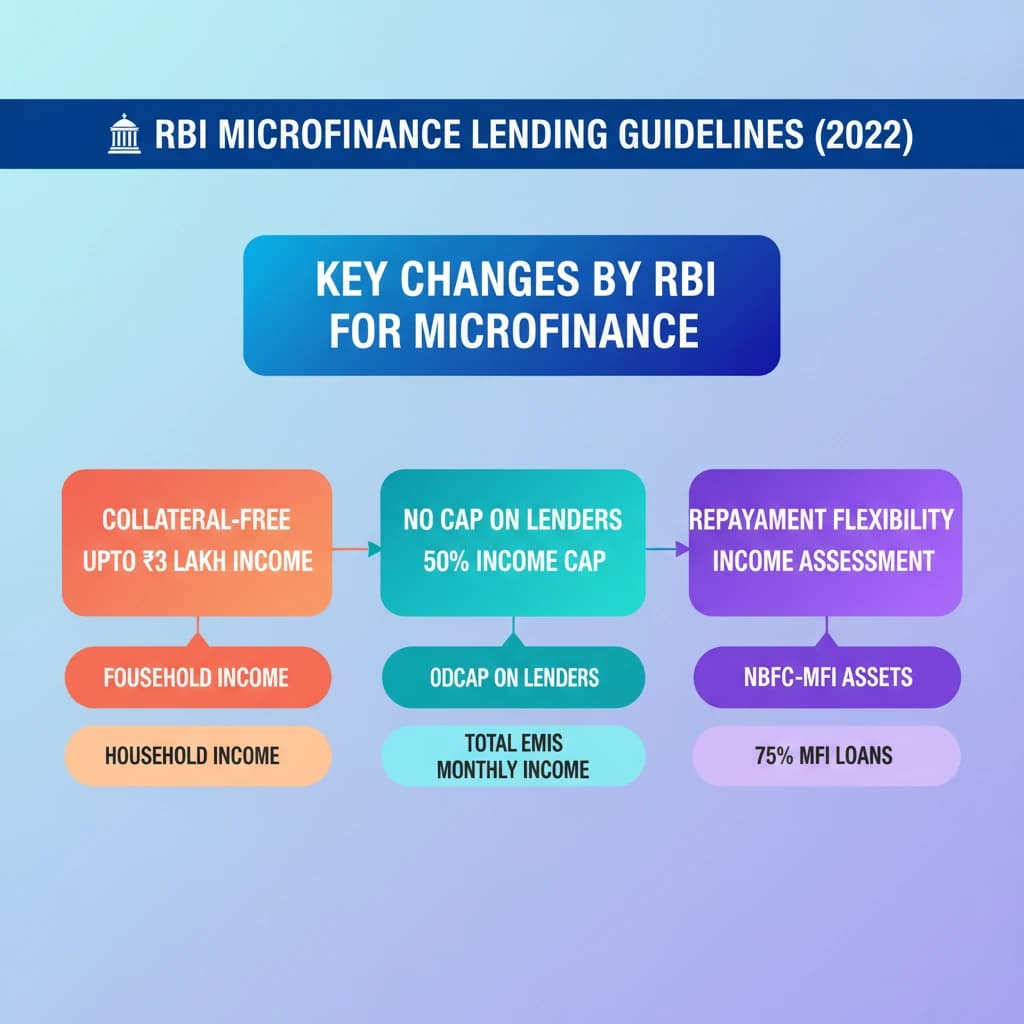

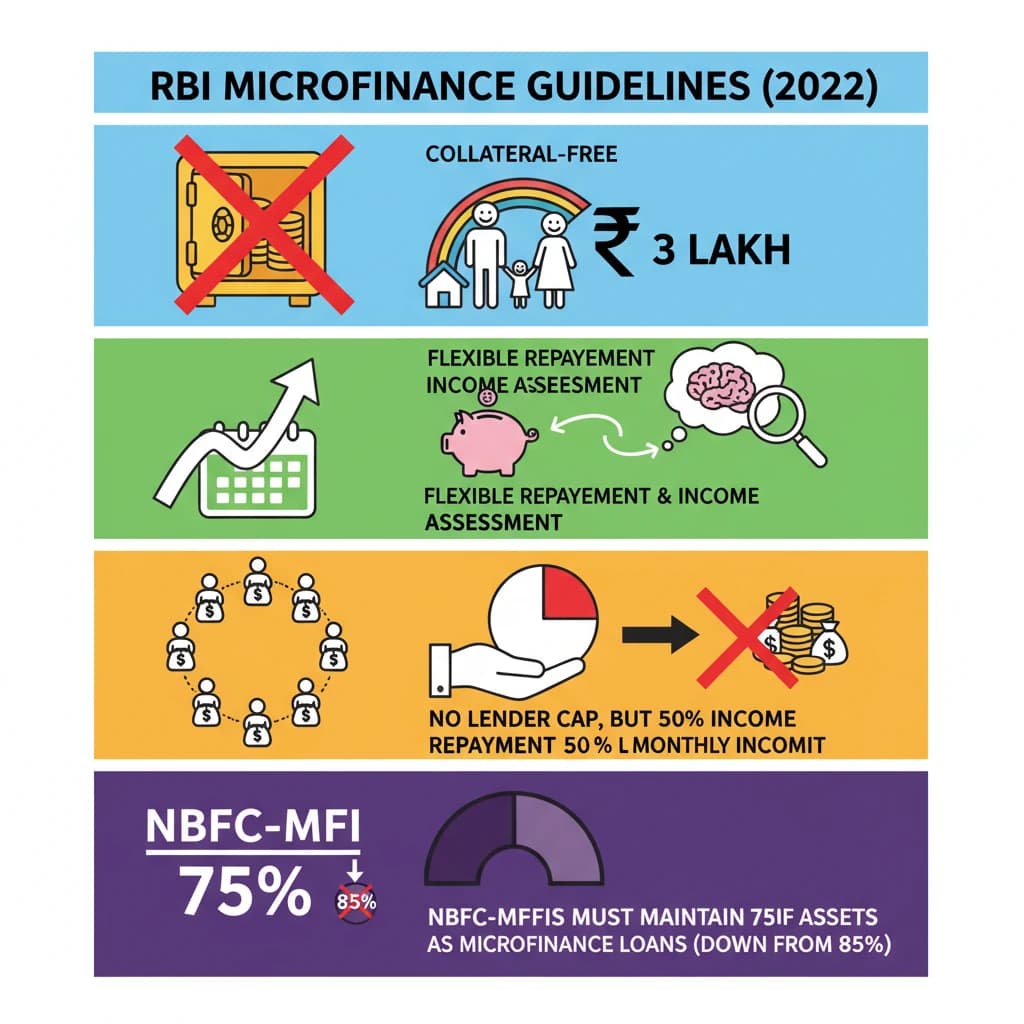

The 2022 guidelines specify clear criteria for classifying a loan as microfinance. A key provision is that loans extended to households with a specific income ceiling are considered collateral-free.

Income Threshold: Microfinance loans are defined as collateral-free loans extended to households with an annual income of up to Rs 3 lakh.

This threshold ensures that low-income households, who often lack traditional collateral, can access credit, thereby promoting financial inclusion.

Flexible Repayment and Income Assessment

Regulated entities are mandated to establish robust policies regarding repayment flexibility and thorough household income assessment. This ensures that repayment schedules are tailored to the borrower's capacity.

Key Requirement: Lenders must formulate policies for flexible repayment options and undertake a comprehensive assessment of household income to prevent over-indebtedness.

Such policies are vital for maintaining the sustainability of microfinance operations and protecting borrowers from undue financial stress.

Lender Cap and Repayment Limit

A significant change introduced by the 2022 guidelines was the removal of the previous cap on the number of lenders a single borrower could access. However, a crucial limit on total repayment was introduced.

New Norms:

- The cap on lenders per borrower has been removed.

- The total repayment obligation for all loans of a household cannot exceed 50% of its monthly household income.

This 50% repayment cap acts as a crucial safeguard against multiple lending and potential over-indebtedness, ensuring responsible lending practices.

NBFC-MFI Portfolio Qualification

The guidelines also revised the criteria for Non-Banking Financial Company - Microfinance Institutions (NBFC-MFIs) regarding the percentage of their loan portfolio that must qualify as microfinance.

Portfolio Requirement: At least 75% of an NBFC-MFI's total assets (excluding cash, bank balances, and money market instruments) must qualify as microfinance loans. This is a reduction from the previous requirement of 85%.

This adjustment provides NBFC-MFIs with slightly more flexibility in managing their asset portfolios while still ensuring their primary focus remains on microfinance activities.

Reporting Requirements

To enhance transparency and data accuracy, regulated entities are now required to report specific financial information related to their borrowers.

Mandatory Reporting: Entities must report any income discrepancies identified during their assessment and regularly update records of the household income of their borrowers.

This reporting mechanism helps the RBI monitor the sector effectively and ensures that lending practices remain aligned with the spirit of the guidelines.

Pre-payment and Late Fee Norms

Borrower protection is further strengthened by specific rules regarding pre-payment penalties and late fees. These norms aim to make microfinance more borrower-friendly.

Borrower-Friendly Norms:

- There shall be no pre-payment penalties on microfinance loans.

- Late payment charges, if any, shall be applicable only on the overdue amount and not on the entire outstanding loan amount.

These provisions reduce the financial burden on borrowers, encouraging timely repayments without punitive charges for early closure or excessive fees on partial delays.

💡 Key Takeaways

- •Microfinance loans are now collateral-free for households with annual income up to Rs 3 lakh.

- •Lenders must implement policies for flexible repayment and robust household income assessment.

- •The cap on the number of lenders per borrower is removed, but total repayment cannot exceed 50% of monthly income.

- •NBFC-MFIs must maintain 75% of their assets as microfinance loans (down from 85%).

- •Entities are mandated to report income discrepancies and household income.

- •No pre-payment penalties are allowed, and late fees apply only to the overdue amount.

- •The guidelines aim for regulatory harmonization and enhanced borrower protection across all regulated entities.

🧠 Memory Techniques

100% Verified Content

📚 Reference Sources

•Economic Survey of India (relevant chapters on financial sector)

•Reputable financial news outlets (e.g., The Economic Times, Livemint) for policy analysis.