Loading page, please wait…

Taxation and Financial Reforms - UPSC Economy

What is Taxation and Financial Reforms in UPSC Economy?

Taxation and Financial Reforms is a key topic under Economy for UPSC Civil Services Examination. Key points include: TDS on Rent limit increased from ₹2.4 lakh to ₹6 lakh, easing compliance for many.. Time limit for updated tax returns extended from 2 years to 4 years, promoting voluntary compliance.. 36 life-saving drugs for cancer, chronic, and rare diseases fully exempted from Basic Customs Duty (BCD).. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is Taxation and Financial Reforms important for UPSC exam?

Taxation and Financial Reforms is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of Taxation and Financial Reforms, making it essential for comprehensive IAS preparation.

How to prepare Taxation and Financial Reforms for UPSC?

To prepare Taxation and Financial Reforms for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking Taxation and Financial Reforms to related GS Paper topics.

Key takeaways of Taxation and Financial Reforms for UPSC

- TDS on Rent limit increased from ₹2.4 lakh to ₹6 lakh, easing compliance for many.

- Time limit for updated tax returns extended from 2 years to 4 years, promoting voluntary compliance.

- 36 life-saving drugs for cancer, chronic, and rare diseases fully exempted from Basic Customs Duty (BCD).

- BCD exemption for Lithium-Ion battery manufacturing capital goods boosts EV/mobile domestic production.

- Textile and electronics sector components also exempted from BCD to encourage local manufacturing and reduce import dependency.

Taxation and Financial Reforms

Medium⏱️ 7 min read

economy

📖 Introduction

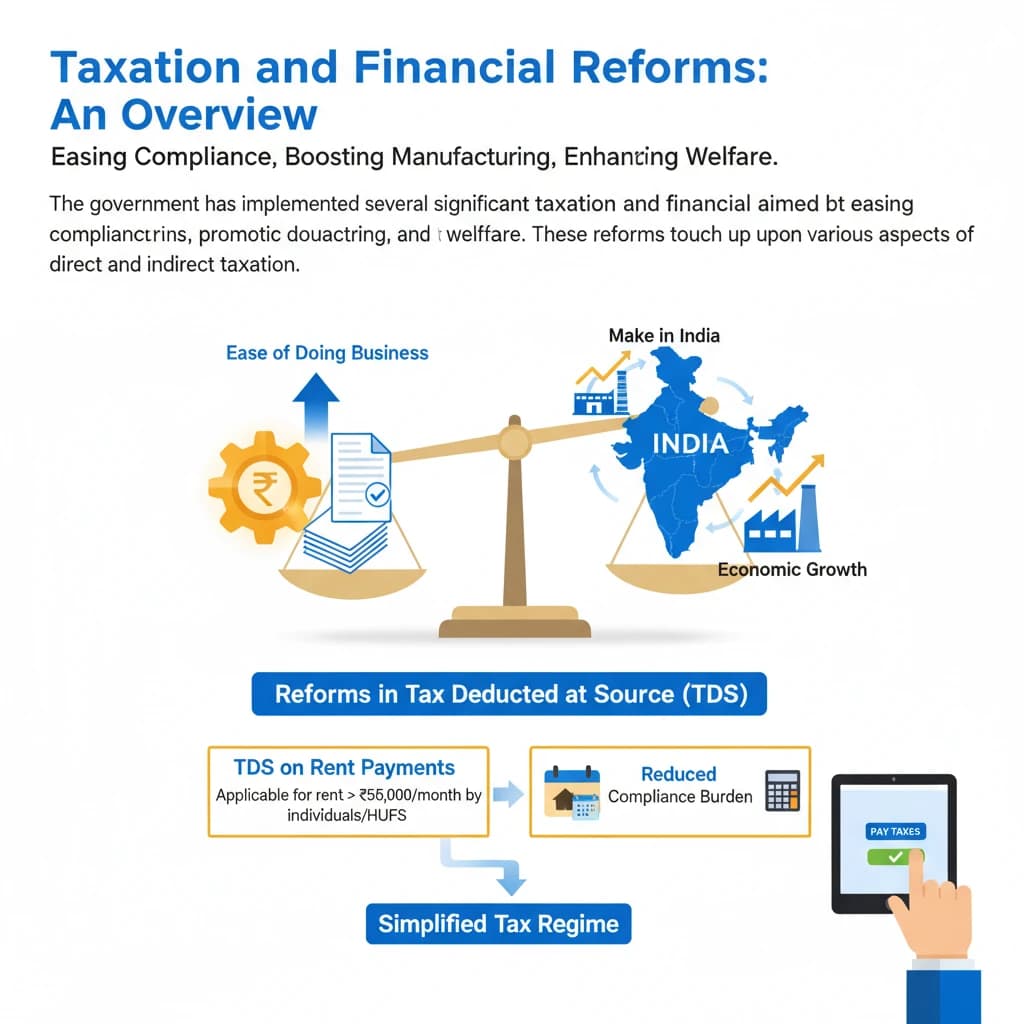

Taxation and Financial Reforms: An Overview

The government has implemented several significant taxation and financial reforms aimed at easing compliance burdens, promoting domestic manufacturing, and improving public welfare. These reforms touch upon various aspects of direct and indirect taxation.

Reforms in Tax Deducted at Source (TDS)

A notable reform involves the Tax Deducted at Source (TDS) mechanism, specifically for rent payments. This adjustment seeks to streamline tax procedures for a large segment of taxpayers.

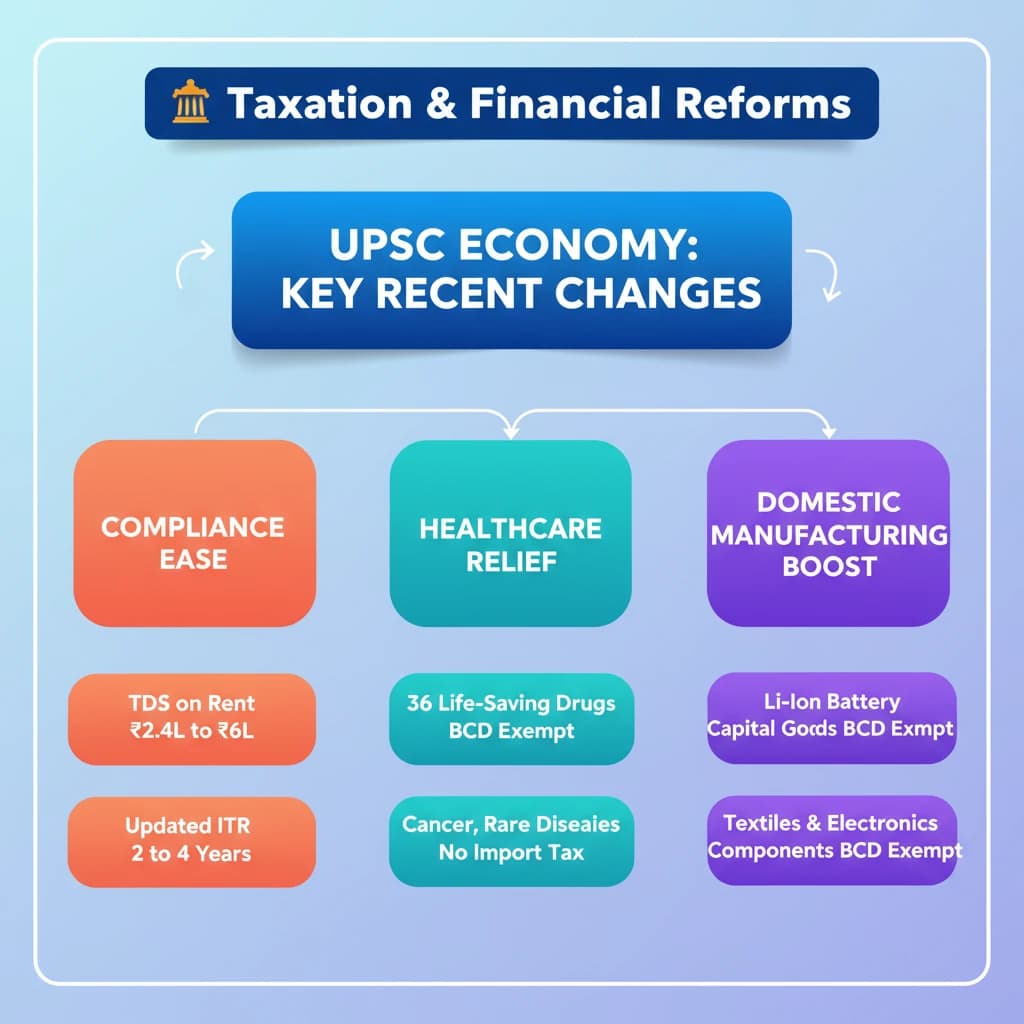

The threshold for TDS on Rent has been significantly increased from ₹2.4 lakh to ₹6 lakh per annum. This change directly impacts individuals and entities involved in rental transactions.

This enhancement is designed to substantially reduce the tax compliance burden on a large number of taxpayers, simplifying their financial obligations and administrative tasks.

Extension of Time Limit for Updated Tax Returns

Another key financial reform focuses on providing greater flexibility for taxpayers to rectify their tax filings. The government has extended the window for submitting updated tax returns.

The time limit for filing updated tax returns has been extended from 2 years to 4 years from the end of the relevant assessment year. This provides a longer period for corrections.

This extension is intended to facilitate voluntary tax compliance, allowing taxpayers more time to ensure accuracy and avoid penalties for past errors or omissions.

Exemptions in Basic Customs Duty (BCD)

To bolster public health and domestic industry, several critical exemptions have been introduced for Basic Customs Duty (BCD). These exemptions target specific sectors and products.

BCD Exemption for Life-Saving Drugs

In a humanitarian move, the government has granted full exemption from Basic Customs Duty (BCD) for essential medical supplies. This aims to make critical treatments more accessible and affordable.

36 life-saving drugs used for treating severe conditions such as cancer, various chronic diseases, and rare diseases are now fully exempted from BCD.

This reform aligns with India's public health goals and can be cited in answers related to healthcare accessibility and social welfare in GS Paper II (Social Justice).

BCD Exemption for Lithium-Ion Battery Manufacturing

To accelerate the transition to green energy and boost local manufacturing capabilities, exemptions have been provided for components crucial to the electric vehicle (EV) and mobile device sectors.

Capital goods used in the manufacturing of Lithium-Ion batteries for both Electric Vehicles (EVs) and mobile devices have been fully exempted from BCD.

This exemption is a strategic move to boost domestic production of these critical components, reducing reliance on imports and fostering a self-reliant energy ecosystem.

BCD Exemption for Textile and Electronics Sector Components

Further strengthening the 'Make in India' initiative, specific components for key industrial sectors have also received customs duty exemptions. This targets two significant manufacturing areas.

Components for the textile sector and the electronics sector have been exempted from BCD. This is designed to support indigenous manufacturing and value addition.

The primary objective of these exemptions is to encourage local manufacturing, thereby reducing India's dependency on imports for crucial industrial inputs and fostering job creation.

💡 Key Takeaways

- •TDS on Rent limit increased from ₹2.4 lakh to ₹6 lakh, easing compliance for many.

- •Time limit for updated tax returns extended from 2 years to 4 years, promoting voluntary compliance.

- •36 life-saving drugs for cancer, chronic, and rare diseases fully exempted from Basic Customs Duty (BCD).

- •BCD exemption for Lithium-Ion battery manufacturing capital goods boosts EV/mobile domestic production.

- •Textile and electronics sector components also exempted from BCD to encourage local manufacturing and reduce import dependency.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•Union Budget documents (general knowledge of where such reforms originate)

•Ministry of Finance official releases (general knowledge)