Loading page, please wait…

What are the Key Aspects of the Income Tax Act, 1961? - UPSC Economy

What is What are the Key Aspects of the Income Tax Act, 1961? in UPSC Economy?

What are the Key Aspects of the Income Tax Act, 1961? is a key topic under Economy for UPSC Civil Services Examination. Key points include: The Income Tax Act, 1961, is India's core law for direct income taxation.. It's a comprehensive statute with 298 sections and 23 chapters, governing income tax levy and collection.. Key objectives include economic stability, progressive taxation, and efficient revenue collection.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are the Key Aspects of the Income Tax Act, 1961? important for UPSC exam?

What are the Key Aspects of the Income Tax Act, 1961? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are the Key Aspects of the Income Tax Act, 1961?, making it essential for comprehensive IAS preparation.

How to prepare What are the Key Aspects of the Income Tax Act, 1961? for UPSC?

To prepare What are the Key Aspects of the Income Tax Act, 1961? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are the Key Aspects of the Income Tax Act, 1961? to related GS Paper topics.

Key takeaways of What are the Key Aspects of the Income Tax Act, 1961? for UPSC

- The Income Tax Act, 1961, is India's core law for direct income taxation.

- It's a comprehensive statute with 298 sections and 23 chapters, governing income tax levy and collection.

- Key objectives include economic stability, progressive taxation, and efficient revenue collection.

- Important provisions cover tax slabs, various deductions (e.g., 80C, 80D, 80G), assessment procedures, and Tax Deducted at Source (TDS).

- Income tax is a direct tax, meaning the burden cannot be shifted by the taxpayer.

What are the Key Aspects of the Income Tax Act, 1961?

Medium⏱️ 5 min read

economy

📖 Introduction

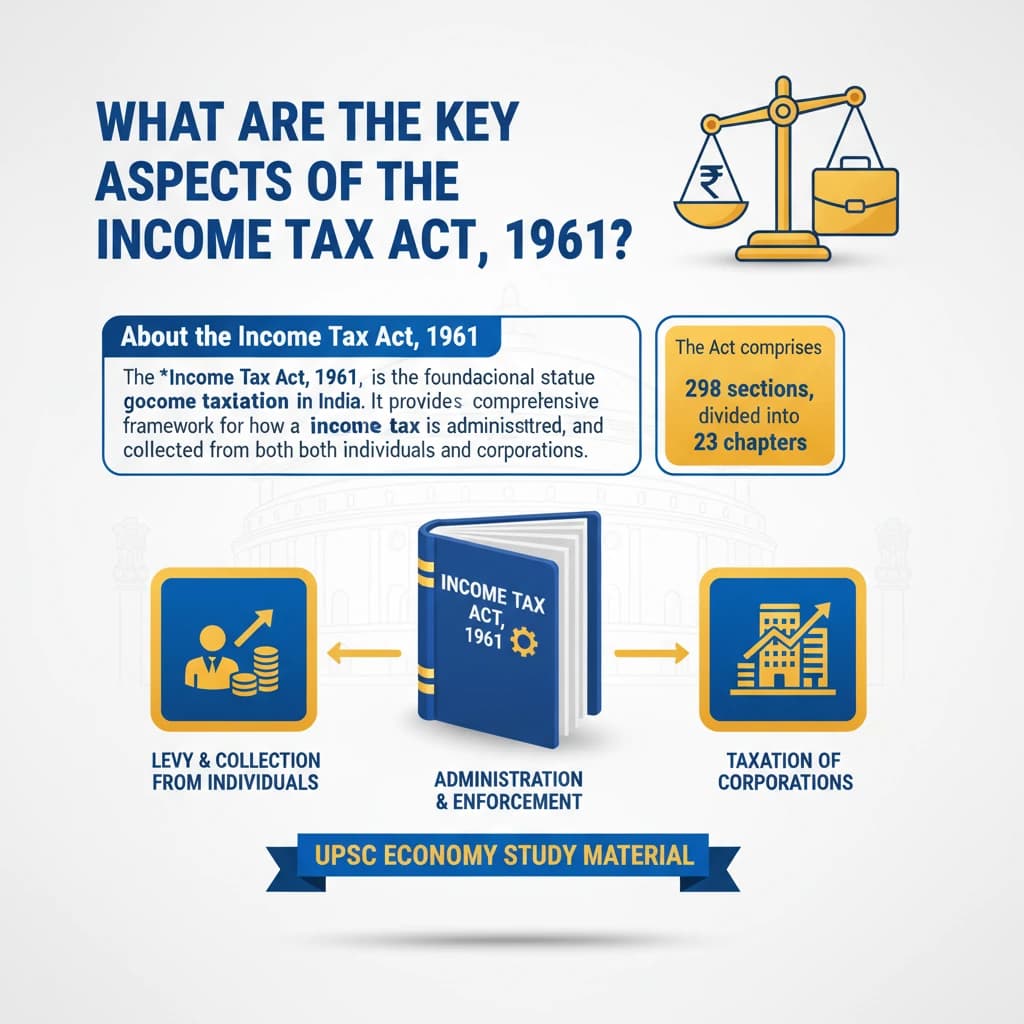

About the Income Tax Act, 1961

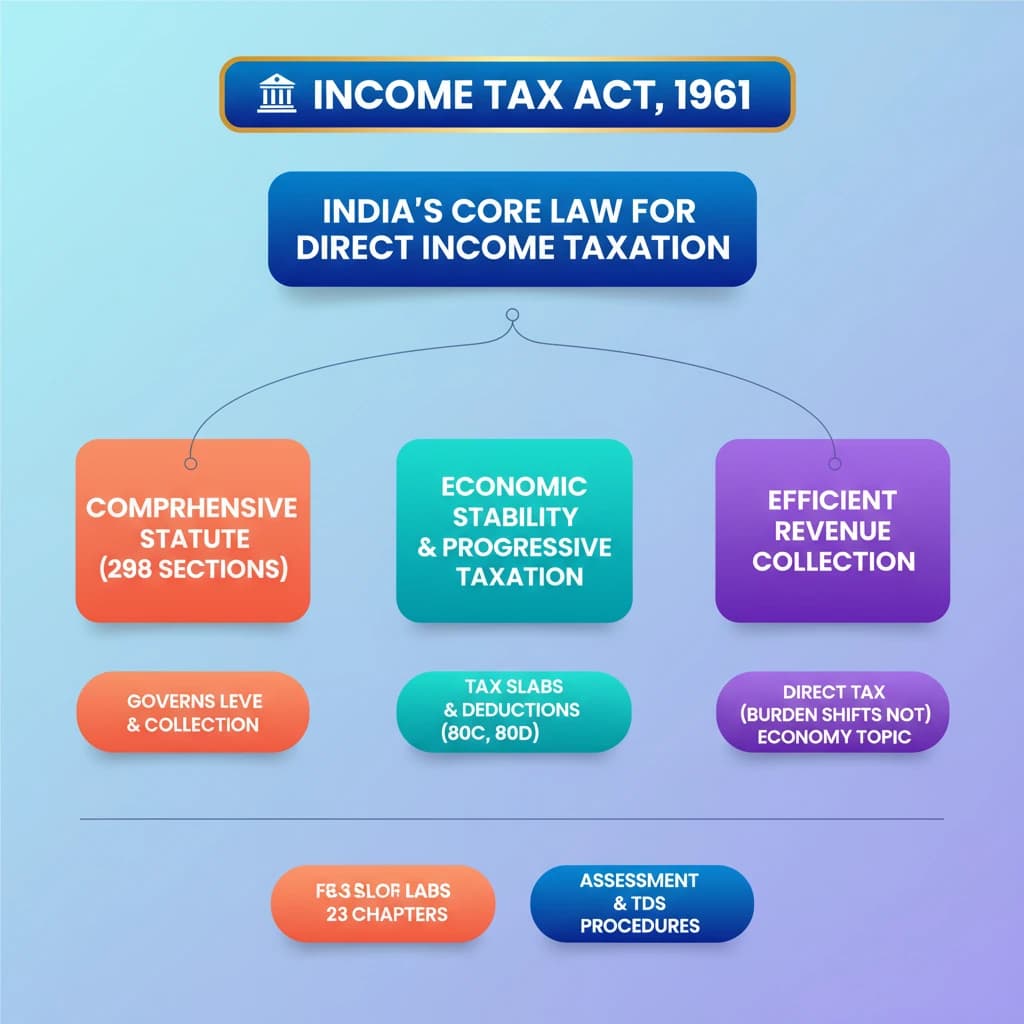

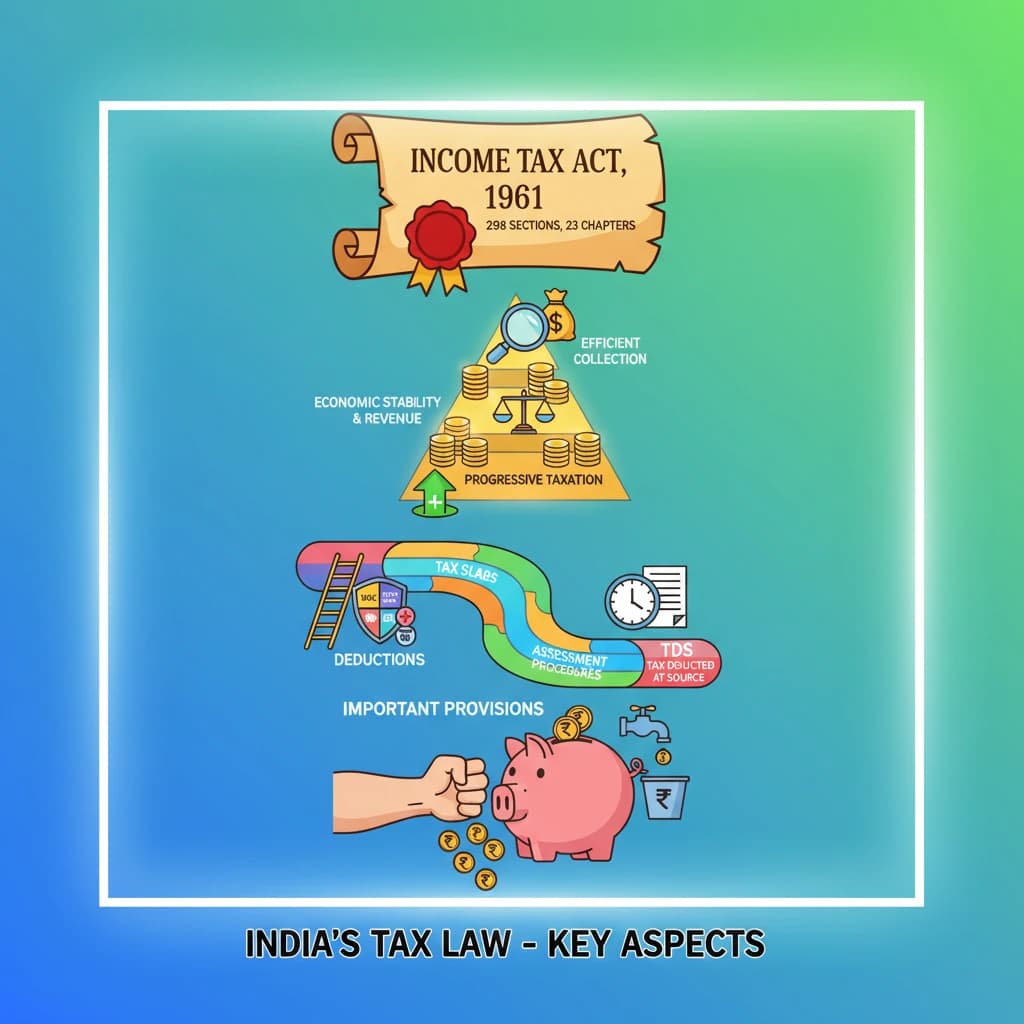

The Income Tax Act, 1961, is the foundational statute governing income taxation in India. It provides a comprehensive framework for how income tax is levied, administered, and collected from both individuals and corporations.

The Act comprises 298 sections, divided into 23 chapters, along with several important provisions detailing all aspects of taxation in India.

Nature of Income Tax

Income tax is categorized as a direct tax. This means the burden of the tax cannot be shifted to another entity or individual.

Individuals and entities are required to directly bear this tax, without the option to transfer their liability.

Objectives of the Act

One key objective is to foster economic stability. It achieves this by regulating private spending and ensuring a structured taxation system.

The Act promotes progressive taxation, aiming for fairness and equity. It ensures that individuals contribute to taxes based on their income levels.

A fundamental goal is efficient revenue collection. By outlining clear rules for taxing income from various sources, it aids in effective financial management for the government.

Key Provisions of the Act

The Act defines various tax slabs. These are income brackets that determine the corresponding tax rates applicable to both individuals and businesses.

It allows for significant deductions, reducing the taxable income. Common sections include:

- Section 80C: For specified investments (e.g., EPF, PPF, life insurance premiums).

- Section 80D: For medical insurance premiums.

- Section 80G: For eligible donations to charitable institutions.

These deductions are subject to specific annual limits as prescribed by the government.

The Act details the procedures for assessing taxable income. This includes guidelines for filing income tax returns and conducting necessary audits.

A crucial provision is Tax Deducted at Source (TDS). This requires tax to be deducted by the payer at the time of making certain payments (e.g., salaries, interest, rent).

TDS simplifies the tax collection process for the government and ensures a steady flow of revenue throughout the year.

💡 Key Takeaways

- •The Income Tax Act, 1961, is India's core law for direct income taxation.

- •It's a comprehensive statute with 298 sections and 23 chapters, governing income tax levy and collection.

- •Key objectives include economic stability, progressive taxation, and efficient revenue collection.

- •Important provisions cover tax slabs, various deductions (e.g., 80C, 80D, 80G), assessment procedures, and Tax Deducted at Source (TDS).

- •Income tax is a direct tax, meaning the burden cannot be shifted by the taxpayer.

🧠 Memory Techniques

95% Verified Content