Loading page, please wait…

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? - UPSC Economy

What is What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? in UPSC Economy?

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? is a key topic under Economy for UPSC Civil Services Examination. Key points include: OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).. NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.. UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? important for UPSC exam?

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)?, making it essential for comprehensive IAS preparation.

How to prepare What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC?

To prepare What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? to related GS Paper topics.

Key takeaways of What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)? for UPSC

- OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).

- NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.

- UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.

- OPS has no employee contribution; UPS and NPS require 10% employee contribution.

- NPS offers clear tax benefits on government contributions; UPS tax benefits are yet to be clarified.

- UPS includes a lump sum payment at retirement and pension indexation based on CPI-IW.

What are the Key Differences between UPS, Old Pension Scheme (OPS) and National Pension Scheme (NPS)?

Medium⏱️ 8 min read

economy

📖 Introduction

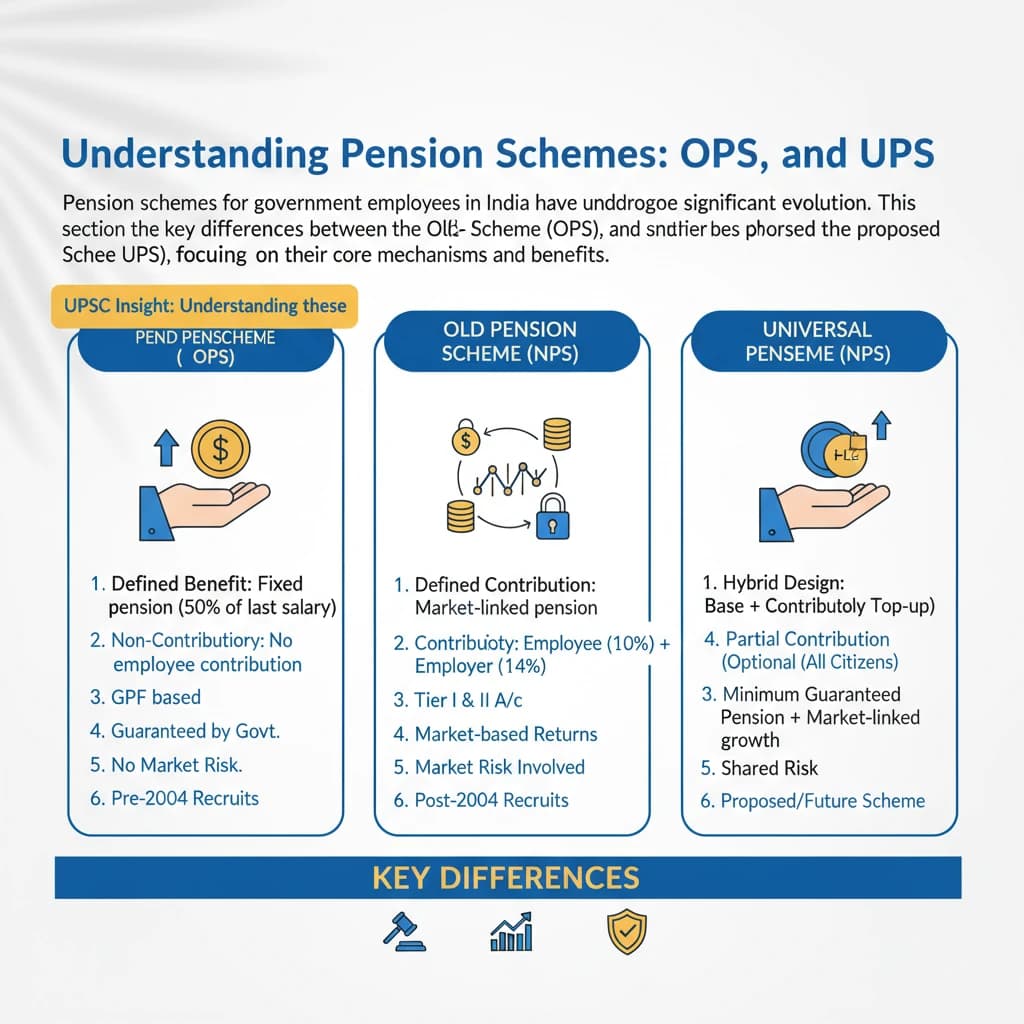

Understanding Pension Schemes: OPS, NPS, and UPS

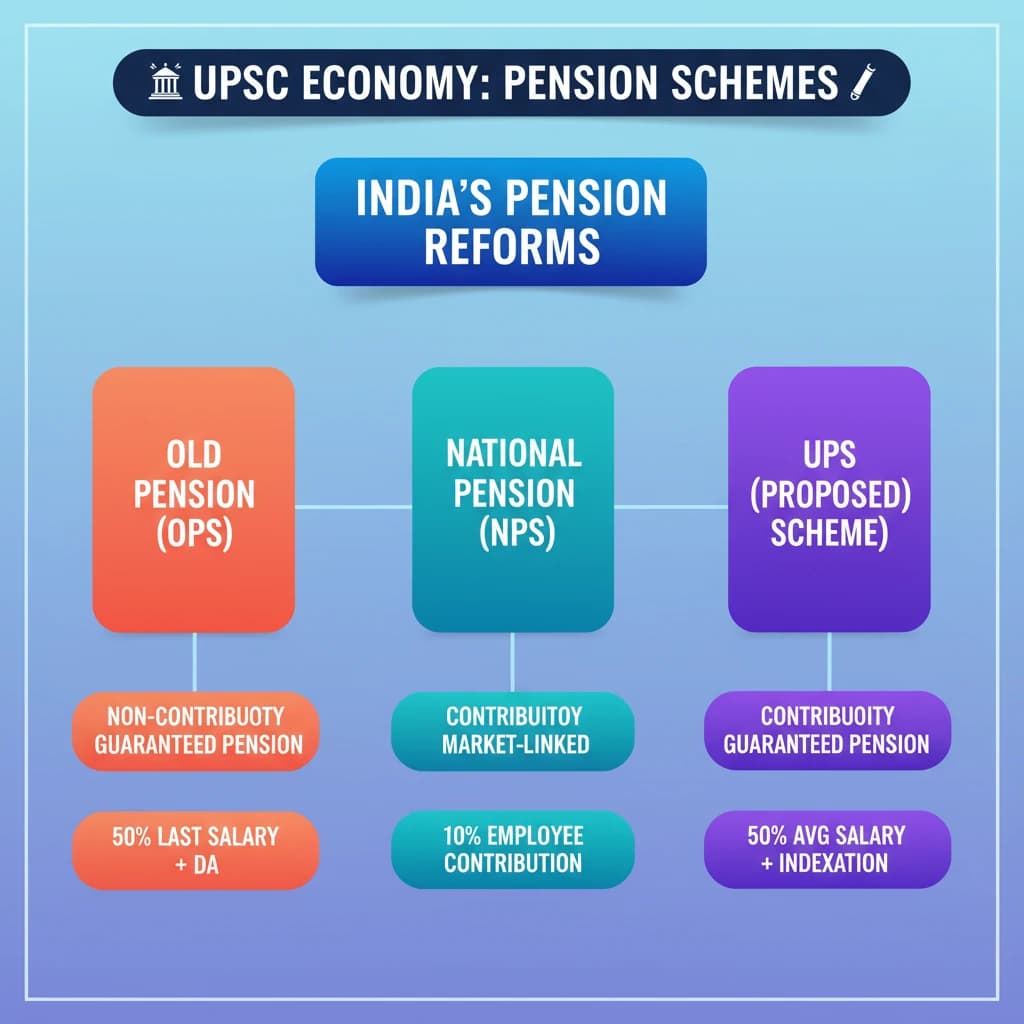

Pension schemes for government employees in India have undergone significant evolution. This section details the key differences between the Old Pension Scheme (OPS), the National Pension Scheme (NPS), and the proposed Universal Pension Scheme (UPS), focusing on their core mechanisms and benefits.

UPSC Insight: Understanding these schemes is crucial for GS Paper 2 (Governance) and GS Paper 3 (Indian Economy). Questions often revolve around fiscal sustainability, social security, and employee welfare.

Pension Calculation Method

The method used to calculate an employee's pension is a primary differentiator among these schemes.

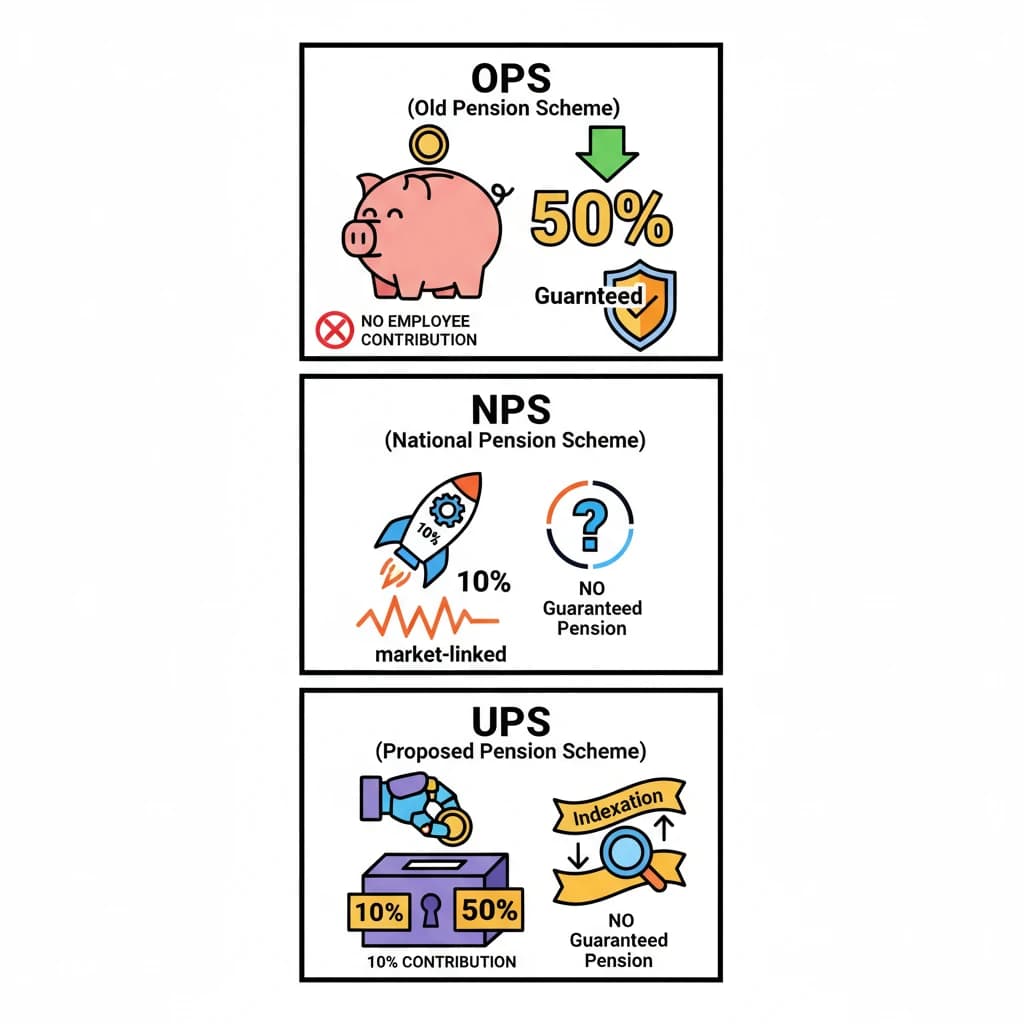

Under the Old Pension Scheme (OPS), pension was fixed at a generous 50% of the last drawn basic salary plus Dearness Allowance (DA). This provided a predictable and often higher retirement income.

For the Universal Pension Scheme (UPS), pension is calculated as 50% of the average of the last salary plus DA drawn in the last year before retirement. This adjustment can result in a slightly lower pension if an employee receives a promotion shortly before retiring, as the average might not fully reflect the final higher pay.

The National Pension Scheme (NPS), being a defined contribution scheme, does not guarantee a fixed pension amount. The pension received depends on the accumulated corpus and market performance of investments.

Employee Contribution and Government Support

The requirement for employee contributions varies significantly across the schemes, impacting both the employee's take-home pay and the government's fiscal burden.

The Old Pension Scheme (OPS) required no employee contribution. This made it highly attractive to employees, as the entire pension was funded by the government.

Under the Universal Pension Scheme (UPS), employees are required to contribute 10% of their basic pay and DA. The government's contribution is set at 14.85%.

The National Pension Scheme (NPS) mandates a 10% contribution from the central government employee’s basic salary. The government's contribution to NPS is 14%.

Tax Benefits

Tax implications play a crucial role in the net financial benefit for employees under different pension schemes.

Employees under the Old Pension Scheme (OPS) could not avail of any specific tax benefits related to pension contributions, as there were no employee contributions required.

For the National Pension Scheme (NPS), central government employees are eligible for significant tax benefits. They can deduct the government's 14% contribution under Section 80CCD(2) of the Income Tax Act, 1961, applicable to both old and new taxation regimes.

Regarding the Universal Pension Scheme (UPS), the government has yet to clarify whether employee and government contributions will be eligible for any specific tax benefits.

Lump Sum Payment at Retirement (UPS Specific)

The Universal Pension Scheme (UPS) introduces a unique provision for a lump sum payment at retirement.

In addition to gratuity, UPS employees will receive a lump sum payment equivalent to 10% of their monthly emoluments (pay + DA) as of the retirement date, for every completed six months of service. This payment is designed to provide immediate financial support upon retirement and will not affect the amount of the assured pension.

Definition: Gratuity is a one-time amount paid by an employer to its employees for rendering their services, typically upon retirement or resignation after a minimum service period.

Indexation of Pension (UPS Specific)

Indexation is a key feature of the Universal Pension Scheme (UPS), ensuring that pension benefits keep pace with inflation.

Under UPS, indexation will be calculated based on the All India Consumer Price Index for Industrial Workers (CPI-IW). This mechanism helps to protect the purchasing power of the pension over time.

Employee Choice (UPS Specific)

The Universal Pension Scheme (UPS) provides a degree of flexibility for existing employees.

Employees can still opt to remain under the National Pension Scheme (NPS) if they choose. However, this is a one-time option; once an employee opts out of NPS for UPS, or vice versa, the option cannot be changed.

💡 Key Takeaways

- •OPS is a non-contributory, defined benefit scheme with guaranteed pension (50% of last salary + DA).

- •NPS is a contributory, defined contribution scheme, market-linked, with no guaranteed pension.

- •UPS (proposed) is a contributory scheme aiming for a guaranteed pension (50% of last year's average salary + DA) with indexation.

- •OPS has no employee contribution; UPS and NPS require 10% employee contribution.

- •NPS offers clear tax benefits on government contributions; UPS tax benefits are yet to be clarified.

- •UPS includes a lump sum payment at retirement and pension indexation based on CPI-IW.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•Reports by the Finance Ministry on NPS and pension reforms

•Economic Survey documents