Loading page, please wait…

What are the Key Facts About the Central Board of Direct Taxes? - UPSC Economy

What is What are the Key Facts About the Central Board of Direct Taxes? in UPSC Economy?

What are the Key Facts About the Central Board of Direct Taxes? is a key topic under Economy for UPSC Civil Services Examination. Key points include: CBDT is a statutory body under the Ministry of Finance, Department of Revenue, administering direct taxes.. It originated from the Central Board of Revenue (1924), which managed both direct and indirect taxes.. The Central Board of Revenue was bifurcated in 1964, formalized by the Central Boards of Revenue Act, 1963.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are the Key Facts About the Central Board of Direct Taxes? important for UPSC exam?

What are the Key Facts About the Central Board of Direct Taxes? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are the Key Facts About the Central Board of Direct Taxes?, making it essential for comprehensive IAS preparation.

How to prepare What are the Key Facts About the Central Board of Direct Taxes? for UPSC?

To prepare What are the Key Facts About the Central Board of Direct Taxes? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are the Key Facts About the Central Board of Direct Taxes? to related GS Paper topics.

Key takeaways of What are the Key Facts About the Central Board of Direct Taxes? for UPSC

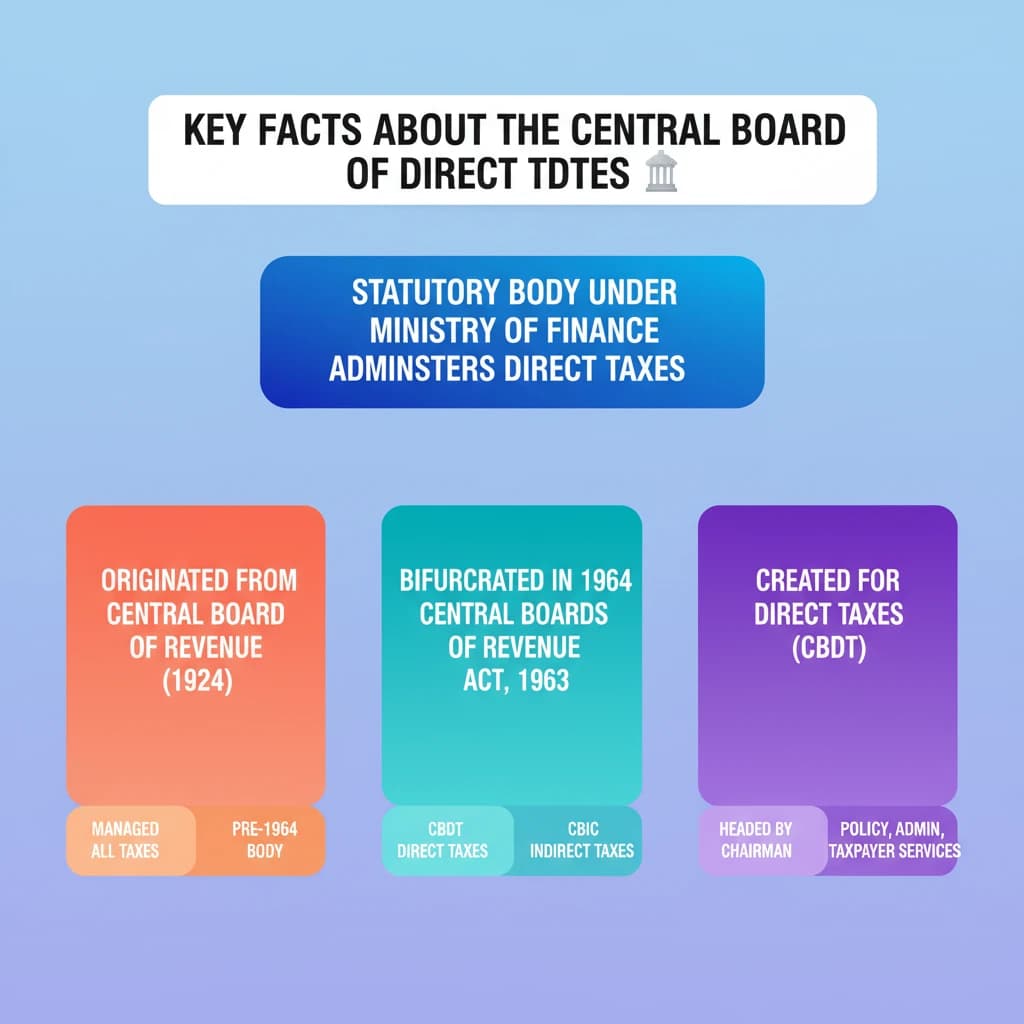

- CBDT is a statutory body under the Ministry of Finance, Department of Revenue, administering direct taxes.

- It originated from the Central Board of Revenue (1924), which managed both direct and indirect taxes.

- The Central Board of Revenue was bifurcated in 1964, formalized by the Central Boards of Revenue Act, 1963.

- This bifurcation created CBDT for direct taxes and the Central Board of Excise and Customs for indirect taxes.

- Headed by a Chairman, CBDT is crucial for policy formulation, administration, and collection of direct taxes, and for improving taxpayer services.

What are the Key Facts About the Central Board of Direct Taxes?

Medium⏱️ 7 min read

economy

📖 Introduction

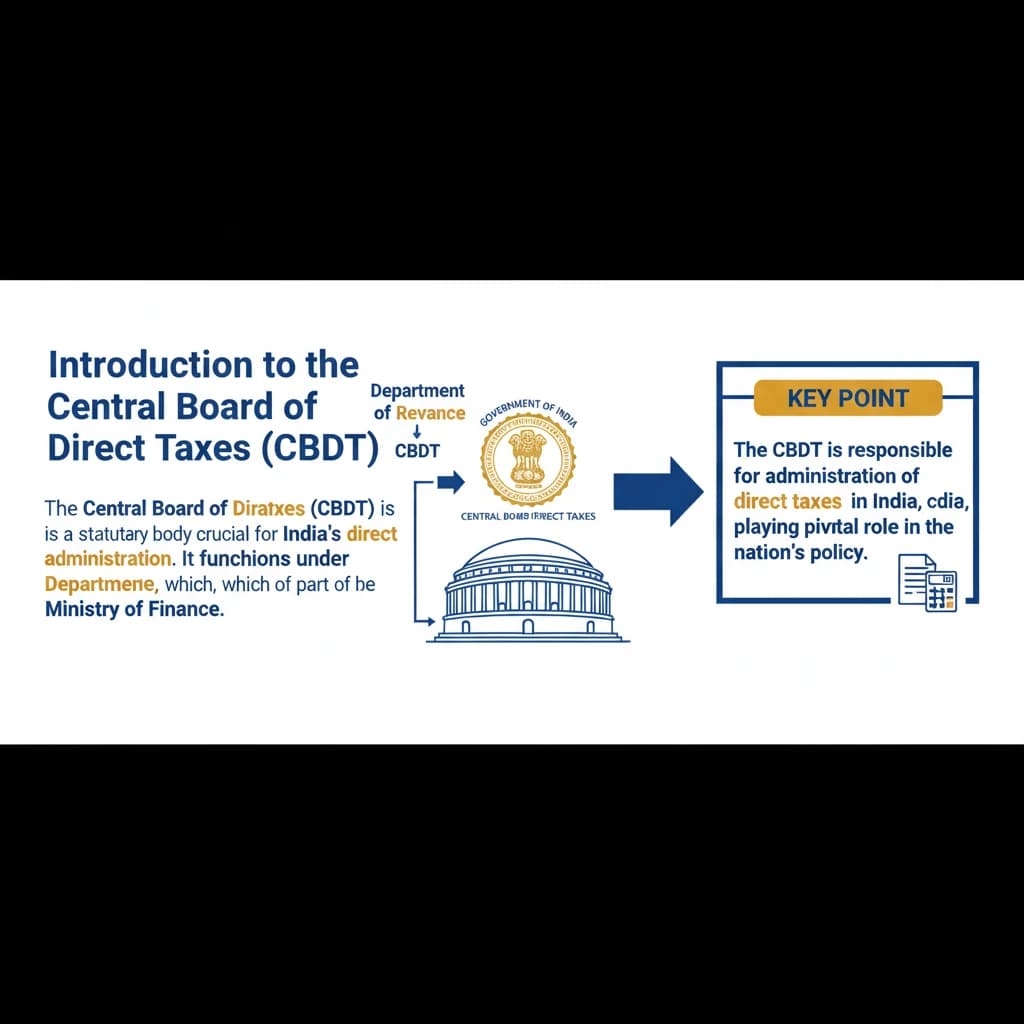

Introduction to the Central Board of Direct Taxes (CBDT)

The Central Board of Direct Taxes (CBDT) is a statutory body crucial for India's direct tax administration. It functions under the Department of Revenue, which is part of the Ministry of Finance.

The CBDT is responsible for the administration of direct taxes in India, playing a pivotal role in the nation's fiscal framework.

Historical Evolution and Genesis

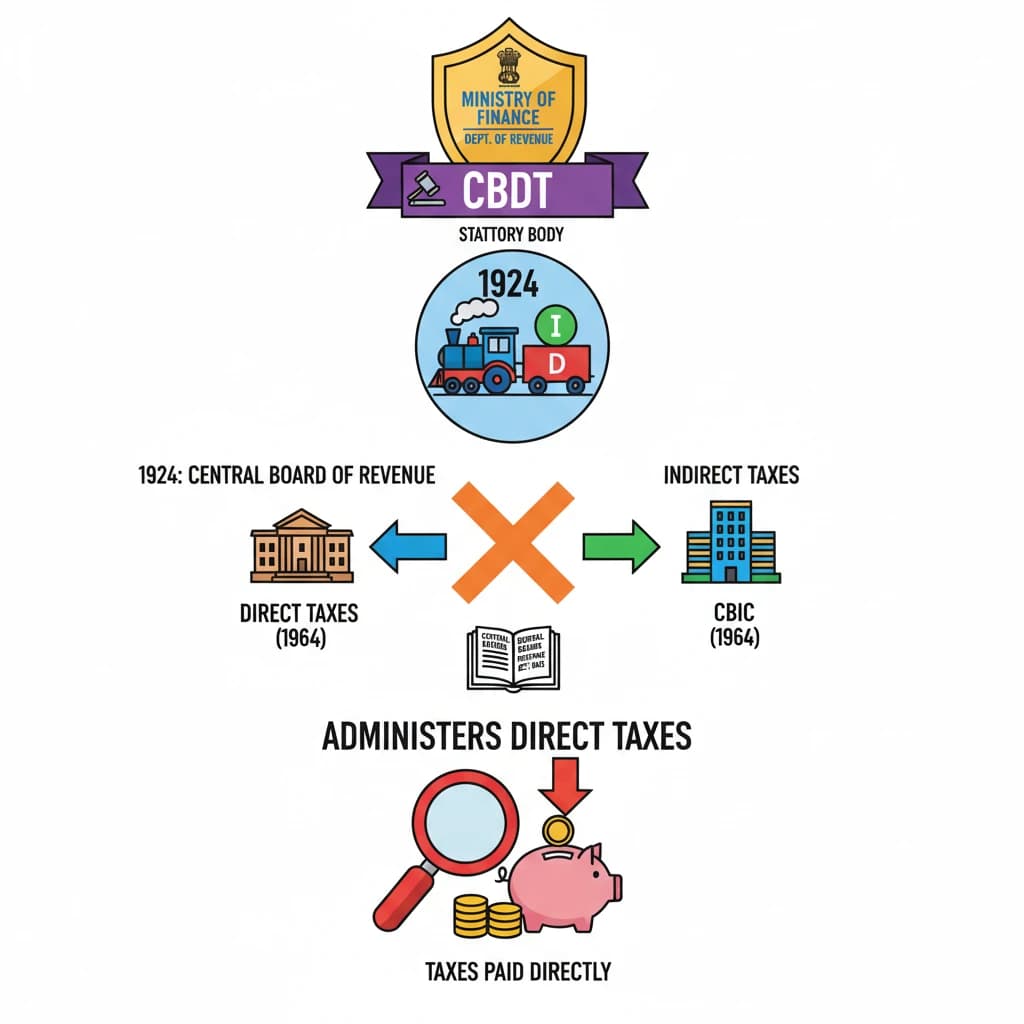

The origins of the CBDT can be traced back to the pre-independence era. Initially, a single administrative body managed both direct and indirect taxes.

This initial body was established under the provisions of the Central Board of Revenue Act, 1924. It was known as the Central Board of Revenue.

The Central Board of Revenue Act, 1924, created the Central Board of Revenue, which had jurisdiction over both direct and indirect taxes.

Bifurcation of the Central Board of Revenue

Over time, the administrative burden associated with managing both categories of taxes became significant. This led to a recognition of the need for specialized bodies.

Consequently, in 1964, the Central Board of Revenue was bifurcated. This split aimed to streamline and enhance the efficiency of tax administration.

- The first distinct body formed was the Central Board of Direct Taxes (CBDT), specifically for direct taxes.

- The second body was the Central Board of Excise and Customs, established for the administration of indirect taxes.

Formalization and Legal Framework

This crucial restructuring was formally institutionalized through the enactment of the Central Boards of Revenue Act, 1963. This Act provided the legal basis for the separate functioning of the two boards.

The Central Boards of Revenue Act, 1963, legally separated the administration of direct and indirect taxes, creating the CBDT and the Central Board of Excise and Customs.

Organizational Structure of CBDT

The CBDT operates with a clear hierarchical structure to ensure effective governance and policy implementation.

At its helm, the CBDT is led by a Chairman. The Chairman is responsible for coordinating all the functions and activities of the Board members and departments.

💡 Key Takeaways

- •CBDT is a statutory body under the Ministry of Finance, Department of Revenue, administering direct taxes.

- •It originated from the Central Board of Revenue (1924), which managed both direct and indirect taxes.

- •The Central Board of Revenue was bifurcated in 1964, formalized by the Central Boards of Revenue Act, 1963.

- •This bifurcation created CBDT for direct taxes and the Central Board of Excise and Customs for indirect taxes.

- •Headed by a Chairman, CBDT is crucial for policy formulation, administration, and collection of direct taxes, and for improving taxpayer services.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•Central Board of Direct Taxes (CBDT) official website

•Ministry of Finance, Government of India