Loading page, please wait…

What is the Deposit Insurance Scheme of DICGC? - UPSC Economy

What is What is the Deposit Insurance Scheme of DICGC? in UPSC Economy?

What is the Deposit Insurance Scheme of DICGC? is a key topic under Economy for UPSC Civil Services Examination. Key points include: DICGC insures bank deposits up to Rs 5 lakh per depositor per bank.. The premium for this insurance is paid by the banks, not the depositors.. Covers all major types of banks (commercial, rural, foreign, cooperative) and deposit types (savings, FD, current, RD).. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What is the Deposit Insurance Scheme of DICGC? important for UPSC exam?

What is the Deposit Insurance Scheme of DICGC? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What is the Deposit Insurance Scheme of DICGC?, making it essential for comprehensive IAS preparation.

How to prepare What is the Deposit Insurance Scheme of DICGC? for UPSC?

To prepare What is the Deposit Insurance Scheme of DICGC? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What is the Deposit Insurance Scheme of DICGC? to related GS Paper topics.

Key takeaways of What is the Deposit Insurance Scheme of DICGC? for UPSC

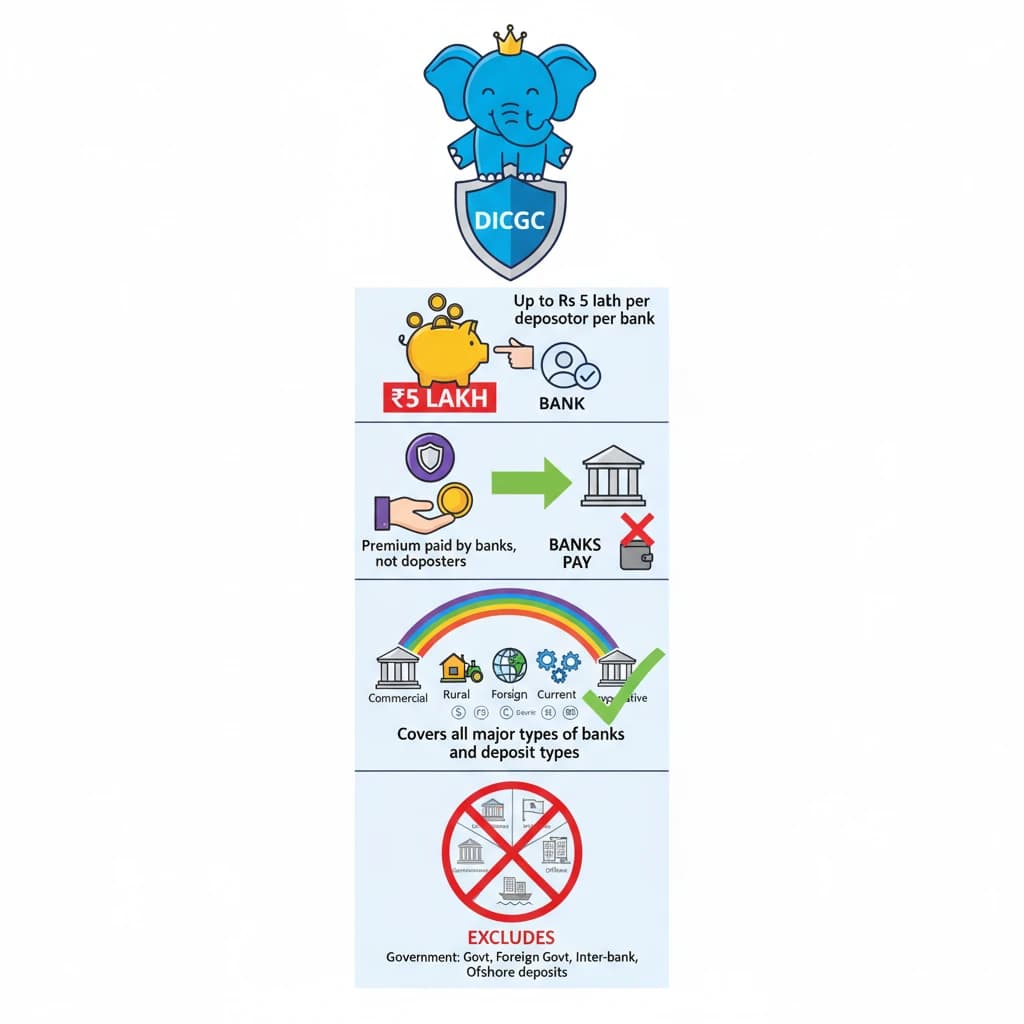

- DICGC insures bank deposits up to Rs 5 lakh per depositor per bank.

- The premium for this insurance is paid by the banks, not the depositors.

- Covers all major types of banks (commercial, rural, foreign, cooperative) and deposit types (savings, FD, current, RD).

- Excludes deposits of governments, foreign governments, inter-bank deposits, and offshore deposits.

- Crucial for maintaining depositor confidence and financial stability in India.

What is the Deposit Insurance Scheme of DICGC?

Medium⏱️ 7 min read

economy

📖 Introduction

Understanding the Deposit Insurance Scheme of DICGC

The Deposit Insurance Scheme is a critical mechanism designed to protect depositors' money in Indian banks. It ensures that a certain portion of their deposits is returned even if a bank fails.

This scheme is administered by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly-owned subsidiary of the Reserve Bank of India (RBI). Its primary objective is to instill confidence in the banking system.

Deposit Insurance Limit

Currently, the deposit insurance limit provides coverage up to Rs 5 lakh per depositor per bank. This means that if a bank collapses, a depositor is legally entitled to receive up to Rs 5 lakh from DICGC, irrespective of the total amount deposited.

Maximum Coverage: A depositor has a claim to a maximum of Rs 5 lakh per account as insurance cover. This amount is termed ‘deposit insurance’.

Important Note: Deposits exceeding Rs 5 lakh in an account have no legal recourse to recover the excess funds in case of bank failure, beyond the insured limit.

Insurance Premium Structure

Banks are required to pay a premium to the DICGC for this insurance cover. This premium is a crucial part of the scheme's funding mechanism.

- The premium rate has been raised from 10 paise for every Rs 100 deposit to 12 paise.

- A maximum limit of 15 paise per Rs 100 deposit has been imposed.

- Crucially, this premium is paid by banks to the DICGC and cannot be passed on to depositors.

Insured banks pay these advance insurance premiums to the corporation semi-annually. Payments are due within two months from the beginning of each financial half-year, based on their deposits at the end of the previous half-year.

Scope of Coverage: Insured Banks

The DICGC scheme mandates coverage for a wide array of banking institutions in India. This ensures broad protection for depositors across different banking sectors.

Banks Mandated to Take Cover:

- All Commercial Banks (including regional rural banks, local area banks).

- Foreign banks with branches operating in India.

- All Cooperative Banks (State, Central, and Primary Cooperative Banks).

Exclusion: Primary cooperative societies are explicitly not insured by the DICGC.

Types of Deposits Covered

The scheme covers almost all types of deposits maintained by depositors in insured banks, providing comprehensive protection for various financial instruments.

Covered Deposits Include:

- Savings deposits

- Fixed deposits (FDs)

- Current accounts

- Recurring deposits (RDs)

- Any other type of deposit, unless specifically exempted.

Deposits Not Covered by DICGC

While broad, certain categories of deposits are specifically excluded from the DICGC insurance cover due to their nature or the entities involved.

Deposits Excluded from Insurance:

- Deposits of foreign Governments.

- Deposits of Central/State Governments.

- Inter-bank deposits (deposits made by one bank in another).

- Deposits of the State Land Development Banks with State co-operative banks.

- Any amount due on account of any deposit received outside India.

- Any amount specifically exempted by the corporation with the previous approval of the RBI.

DICGC's General Fund

The DICGC maintains a General Fund to manage its operational expenditures. This fund is crucial for the smooth functioning of the corporation.

The General Fund covers DICGC’s operational expenses. It is primarily funded by the surplus generated from its operations, ensuring financial self-sufficiency.

For UPSC Prelims, remember the Rs 5 lakh limit, who pays the premium (banks), and the major categories of deposits/banks covered and excluded. For Mains, understand its role in financial stability and depositor confidence (GS Paper III: Economy).

💡 Key Takeaways

- •DICGC insures bank deposits up to Rs 5 lakh per depositor per bank.

- •The premium for this insurance is paid by the banks, not the depositors.

- •Covers all major types of banks (commercial, rural, foreign, cooperative) and deposit types (savings, FD, current, RD).

- •Excludes deposits of governments, foreign governments, inter-bank deposits, and offshore deposits.

- •Crucial for maintaining depositor confidence and financial stability in India.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•DICGC Official Website

•Reserve Bank of India (RBI) Publications