Loading page, please wait…

What is the Legal Status of Cryptocurrency in India? - UPSC Economy

What is What is the Legal Status of Cryptocurrency in India? in UPSC Economy?

What is the Legal Status of Cryptocurrency in India? is a key topic under Economy for UPSC Civil Services Examination. Key points include: Cryptocurrencies in India are unregulated but not banned.. They are not recognized as legal tender by the government.. A 30% tax is levied on the transfer of virtual digital assets since Union Budget 2022-23.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What is the Legal Status of Cryptocurrency in India? important for UPSC exam?

What is the Legal Status of Cryptocurrency in India? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What is the Legal Status of Cryptocurrency in India?, making it essential for comprehensive IAS preparation.

How to prepare What is the Legal Status of Cryptocurrency in India? for UPSC?

To prepare What is the Legal Status of Cryptocurrency in India? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What is the Legal Status of Cryptocurrency in India? to related GS Paper topics.

Key takeaways of What is the Legal Status of Cryptocurrency in India? for UPSC

- Cryptocurrencies in India are unregulated but not banned.

- They are not recognized as legal tender by the government.

- A 30% tax is levied on the transfer of virtual digital assets since Union Budget 2022-23.

- India has launched its own Central Bank Digital Currency (CBDC), the Digital Rupee (e-RUPI).

- CBDCs are legal tender, issued and backed by the central bank, unlike private cryptocurrencies.

What is the Legal Status of Cryptocurrency in India?

Medium⏱️ 5 min read

economy

📖 Introduction

Legal Status of Cryptocurrency in India

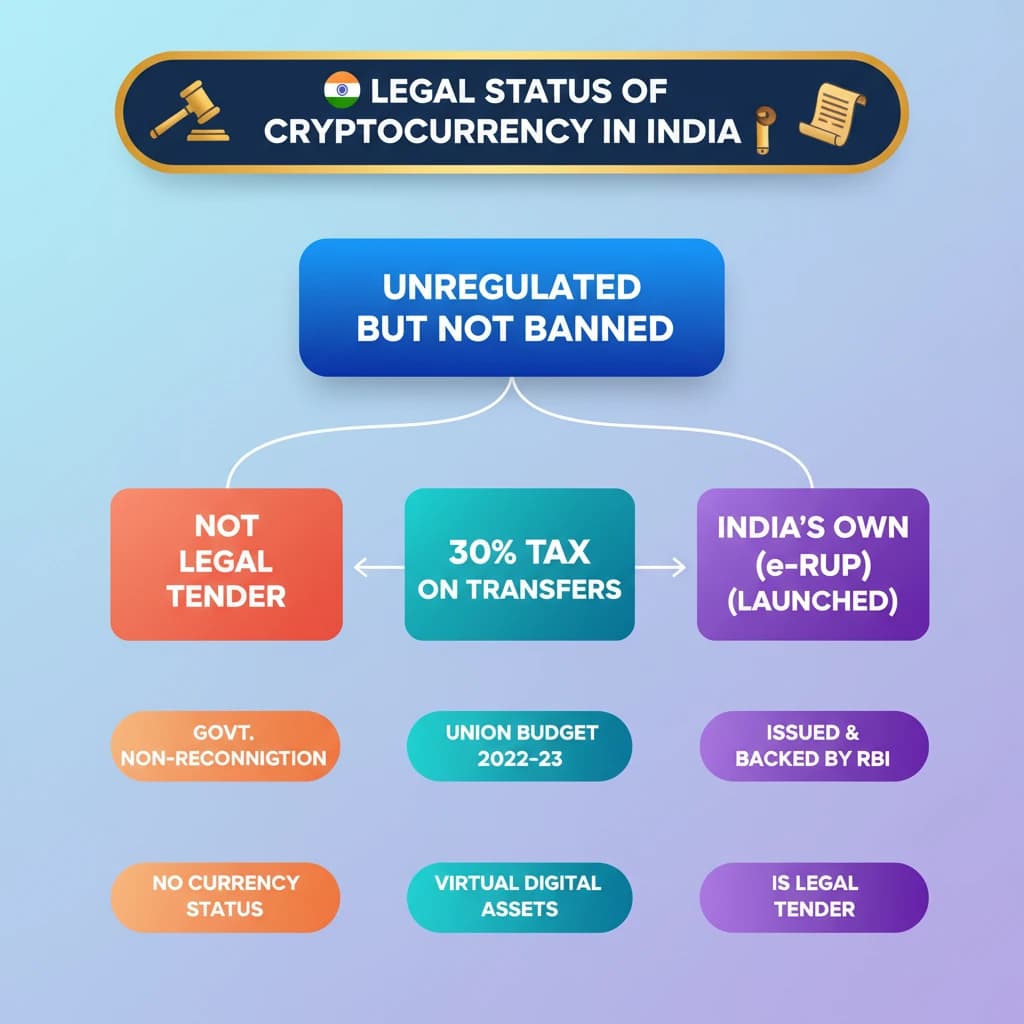

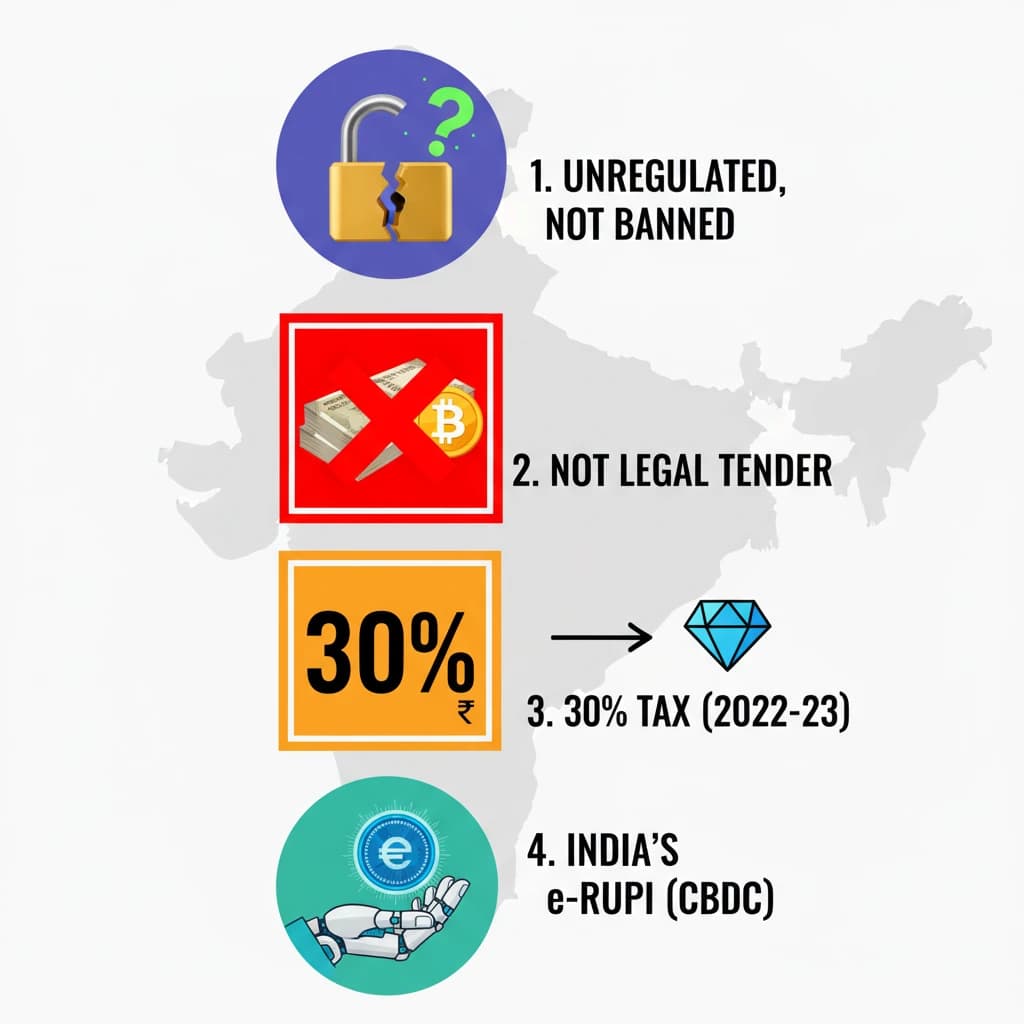

In India, the legal status of cryptocurrencies is characterized by a nuanced approach. They are currently unregulated but are not specifically banned. This means while there isn't a dedicated legal framework governing them, their existence and certain activities are not outright prohibited.

Government Stance and Recognition

The Government of India maintains that cryptocurrencies are not recognized as legal tender. This distinction is crucial, as it implies they cannot be used to discharge debts or make payments with statutory backing. The government also intends to address their potential use in financing illegal activities, treating such instances as a payment method for illicit transactions.

Key Point: Cryptocurrencies are unregulated, not banned, but not legal tender in India.

Taxation of Virtual Digital Assets

A significant development occurred in 2022. During the Union Budget 2022-23, the government announced a specific tax regime for Virtual Digital Assets (VDAs), which include cryptocurrencies. This move effectively acknowledges their existence for taxation purposes.

Taxation Rule: The transfer of any virtual currency/cryptocurrency asset is subject to a 30% tax deduction.

UPSC Insight: The introduction of taxation, while not conferring legal tender status, signifies a de facto recognition of cryptocurrencies as assets. This can be a point of discussion in GS Paper III (Economy) questions.

Introduction of Central Bank Digital Currency (CBDC)

In parallel to its stance on private cryptocurrencies, India has launched its own Central Bank Digital Currency (CBDC). This initiative is a significant step towards modernizing the country's financial infrastructure.

India's CBDC: Known as the Digital Rupee, which the source text also refers to as ‘e-RUPI’. It was launched by the National Payments Corporation of India (NPCI) in collaboration with various government bodies and partner banks.

- Collaborating Entities: Department of Financial Services (DFS), National Health Authority (NHA), Ministry of Health and Family Welfare (MoHFW), and partner banks.

CBDC vs. Cryptocurrencies: Key Distinctions

While the concept of CBDCs was inspired by decentralized digital currencies like Bitcoin, they are fundamentally different. CBDCs are a digital form of a country's fiat currency, issued and backed by the central bank.

Core Difference: CBDCs are legal tenders, issued and backed by a central bank. Cryptocurrencies operate in a regulatory vacuum and lack state backing or legal tender status.

The Digital Rupee or e-Rupee can be transacted using wallets, often leveraging blockchain technology. This provides a secure and efficient medium for digital transactions.

💡 Key Takeaways

- •Cryptocurrencies in India are unregulated but not banned.

- •They are not recognized as legal tender by the government.

- •A 30% tax is levied on the transfer of virtual digital assets since Union Budget 2022-23.

- •India has launched its own Central Bank Digital Currency (CBDC), the Digital Rupee (e-RUPI).

- •CBDCs are legal tender, issued and backed by the central bank, unlike private cryptocurrencies.

🧠 Memory Techniques

95% Verified Content