Loading page, please wait…

What are the Government Schemes Related to Microfinance? - UPSC Economy

What is What are the Government Schemes Related to Microfinance? in UPSC Economy?

What are the Government Schemes Related to Microfinance? is a key topic under Economy for UPSC Civil Services Examination. Key points include: Government microfinance schemes target financial inclusion for the unbanked and underserved.. <strong>PMMY</strong> provides collateral-free loans up to ₹10 lakh for micro-enterprises (Shishu, Kishor, Tarun).. <strong>SHG-Bank Linkage Program</strong> connects Self-Help Groups with formal banks, empowering collective action.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What are the Government Schemes Related to Microfinance? important for UPSC exam?

What are the Government Schemes Related to Microfinance? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What are the Government Schemes Related to Microfinance?, making it essential for comprehensive IAS preparation.

How to prepare What are the Government Schemes Related to Microfinance? for UPSC?

To prepare What are the Government Schemes Related to Microfinance? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What are the Government Schemes Related to Microfinance? to related GS Paper topics.

Key takeaways of What are the Government Schemes Related to Microfinance? for UPSC

- Government microfinance schemes target financial inclusion for the unbanked and underserved.

- <strong>PMMY</strong> provides collateral-free loans up to ₹10 lakh for micro-enterprises (Shishu, Kishor, Tarun).

- <strong>SHG-Bank Linkage Program</strong> connects Self-Help Groups with formal banks, empowering collective action.

- <strong>NRLM (DAY-NRLM)</strong> focuses on rural poverty reduction through SHGs and livelihood opportunities.

- <strong>DAY-NULM</strong> addresses urban poverty via skill development and micro-enterprise support for urban SHGs.

- <strong>CGTMSE</strong> offers credit guarantee cover to banks for collateral-free loans to Micro and Small Enterprises (MSEs).

What are the Government Schemes Related to Microfinance?

Medium⏱️ 8 min read

economy

📖 Introduction

Introduction to Government Microfinance Schemes

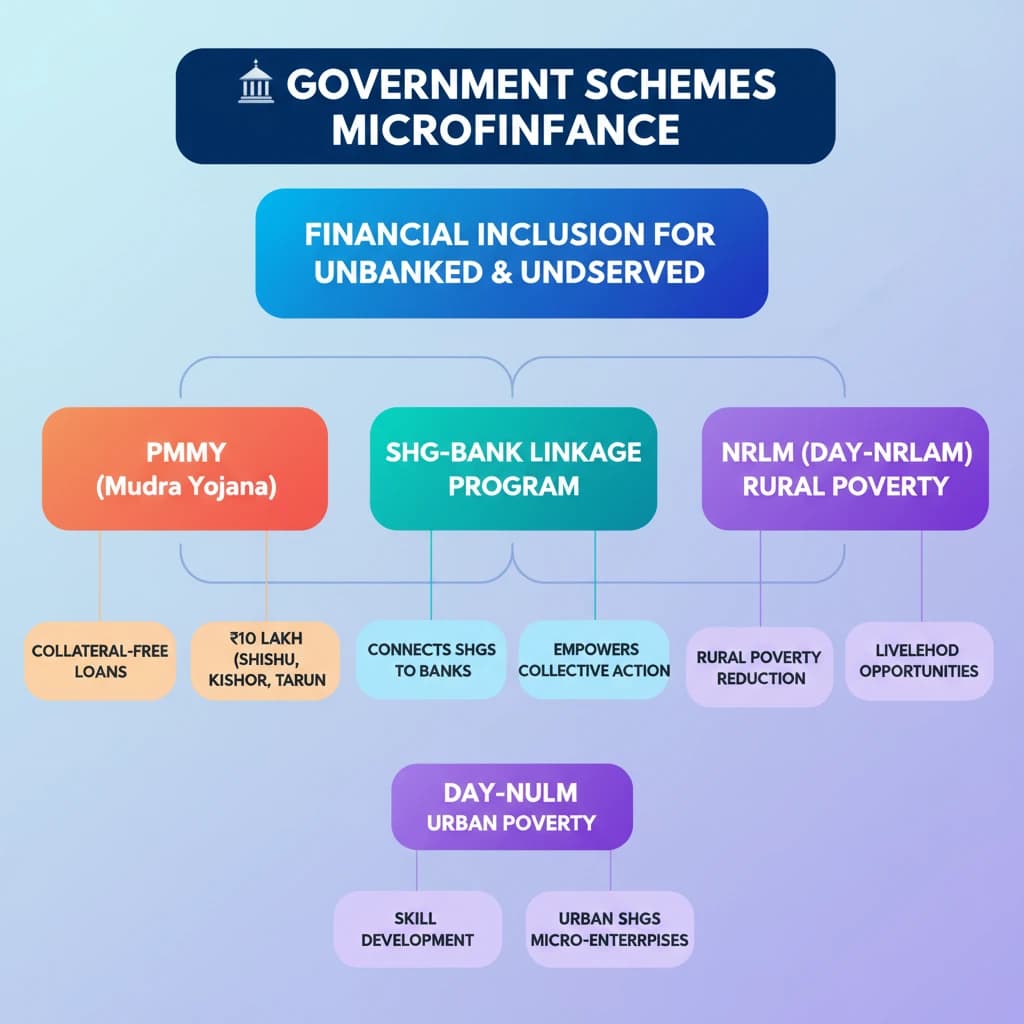

The Indian government has launched various initiatives to promote microfinance, recognizing its critical role in financial inclusion and poverty alleviation. These schemes aim to provide accessible credit to the unbanked and underserved populations, particularly in rural and semi-urban areas.

Microfinance facilitates small loans and other financial services to individuals or groups who typically lack access to conventional banking services. It empowers beneficiaries, often women, to start or expand small businesses and improve their livelihoods.

Key Objective: To extend financial services to the poor and low-income households, enabling them to become self-reliant and integrate into the formal economy.

Pradhan Mantri Mudra Yojana (PMMY)

Launched in 2015, the Pradhan Mantri Mudra Yojana (PMMY) provides loans up to ₹10 lakh to non-corporate, non-farm small/micro enterprises. These loans are extended by commercial banks, RRBs, Small Finance Banks, MFIs, and NBFCs.

Loan Categories under PMMY:

- Shishu: Loans up to ₹50,000 (for new businesses)

- Kishor: Loans above ₹50,000 and up to ₹5 lakh

- Tarun: Loans above ₹5 lakh and up to ₹10 lakh

The scheme focuses on funding the 'unfunded' and encourages entrepreneurship among the disadvantaged sections of society, including women and Scheduled Castes/Tribes.

Self-Help Group (SHG) - Bank Linkage Program (SBLP)

The SHG-Bank Linkage Program (SBLP), initiated by NABARD in 1992, is one of the largest microfinance programs globally. It aims to link Self-Help Groups (SHGs) with formal financial institutions.

SHGs are small, informal groups, predominantly of women, who pool their savings and lend to each other. Once mature, these groups become eligible for credit from banks, leveraging their collective guarantee for loans.

Mechanism: SHGs act as intermediaries between banks and their members, reducing transaction costs for both, and ensuring better repayment rates due to peer pressure and local knowledge.

National Rural Livelihoods Mission (NRLM) / Aajeevika

The National Rural Livelihoods Mission (NRLM), now known as Aajeevika - Deendayal Antyodaya Yojana-NRLM (DAY-NRLM), was launched in 2011. It aims to reduce poverty by enabling poor households to access gainful self-employment and skilled wage employment opportunities.

NRLM promotes institution building of the poor, primarily through SHGs, and provides financial support, capacity building, and access to credit and markets. It works towards universal financial inclusion for rural poor households.

UPSC Insight: NRLM is crucial for understanding rural development and women's empowerment. Questions often link it to SHG functionality and its impact on poverty reduction.

Deen Dayal Upadhyaya Antyodaya Yojana (DAY-NULM)

The Deen Dayal Upadhyaya Antyodaya Yojana (DAY-NULM) focuses on alleviating urban poverty. Launched in 2013, it aims to uplift the urban poor by enhancing their livelihood opportunities through skill development and self-employment.

DAY-NULM supports the formation of Self-Help Groups (SHGs) among the urban poor and provides them with financial assistance for setting up micro-enterprises. It also includes components for shelter for the urban homeless and vendor support.

Key Components: Social Mobilization and Institution Development (SM&ID), Capacity Building and Training (CBT), Employment through Skill Training and Placement (EST&P), Self-Employment Programme (SEP), Support to Urban Street Vendors (SUSV), Scheme for Homeless (SUH).

Credit Guarantee Fund for Micro and Small Enterprises (CGTMSE)

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) was jointly set up by the Ministry of MSME and SIDBI in 2000. Its primary objective is to make collateral-free credit available to the Micro and Small Enterprise (MSE) sector.

This scheme provides a guarantee cover to banks and financial institutions for collateral-free loans extended to eligible MSEs. It mitigates the risk for lenders, thereby encouraging them to lend more to this crucial sector.

Benefit: CGTMSE eliminates the need for collateral or third-party guarantees, which is often a major hurdle for small entrepreneurs seeking finance.

💡 Key Takeaways

- •Government microfinance schemes target financial inclusion for the unbanked and underserved.

- •<strong>PMMY</strong> provides collateral-free loans up to ₹10 lakh for micro-enterprises (Shishu, Kishor, Tarun).

- •<strong>SHG-Bank Linkage Program</strong> connects Self-Help Groups with formal banks, empowering collective action.

- •<strong>NRLM (DAY-NRLM)</strong> focuses on rural poverty reduction through SHGs and livelihood opportunities.

- •<strong>DAY-NULM</strong> addresses urban poverty via skill development and micro-enterprise support for urban SHGs.

- •<strong>CGTMSE</strong> offers credit guarantee cover to banks for collateral-free loans to Micro and Small Enterprises (MSEs).

🧠 Memory Techniques

98% Verified Content

📚 Reference Sources

•NABARD (SHG-Bank Linkage Program, NRLM information)

•Ministry of Rural Development, Government of India (NRLM details)

•Ministry of Housing and Urban Affairs, Government of India (DAY-NULM details)

•Reserve Bank of India (RBI) publications on financial inclusion and microfinance