Loading page, please wait…

What is Non-Performing Asset (NPA)? - UPSC Economy

What is What is Non-Performing Asset (NPA)? in UPSC Economy?

What is Non-Performing Asset (NPA)? is a key topic under Economy for UPSC Civil Services Examination. Key points include: NPA: Loan overdue for 90+ days (or 2 crop seasons for short-duration agri loans).. Gross NPA = total bad loans; Net NPA = Gross NPA minus provisions.. Provisions are funds set aside by banks for potential NPA losses.. Understanding this topic is essential for both UPSC Prelims and Mains preparation.

Why is What is Non-Performing Asset (NPA)? important for UPSC exam?

What is Non-Performing Asset (NPA)? is a Medium-level topic in UPSC Economy. It is tested in both Prelims (factual MCQs) and Mains (analytical answer writing). Previous year UPSC questions have frequently covered aspects of What is Non-Performing Asset (NPA)?, making it essential for comprehensive IAS preparation.

How to prepare What is Non-Performing Asset (NPA)? for UPSC?

To prepare What is Non-Performing Asset (NPA)? for UPSC: (1) Study the comprehensive notes covering all key concepts on Vaidra. (2) Practice previous year questions on this topic. (3) Connect it with current affairs using daily updates. (4) Revise using key takeaways and mind maps available for Economy. (5) Write practice answers linking What is Non-Performing Asset (NPA)? to related GS Paper topics.

Key takeaways of What is Non-Performing Asset (NPA)? for UPSC

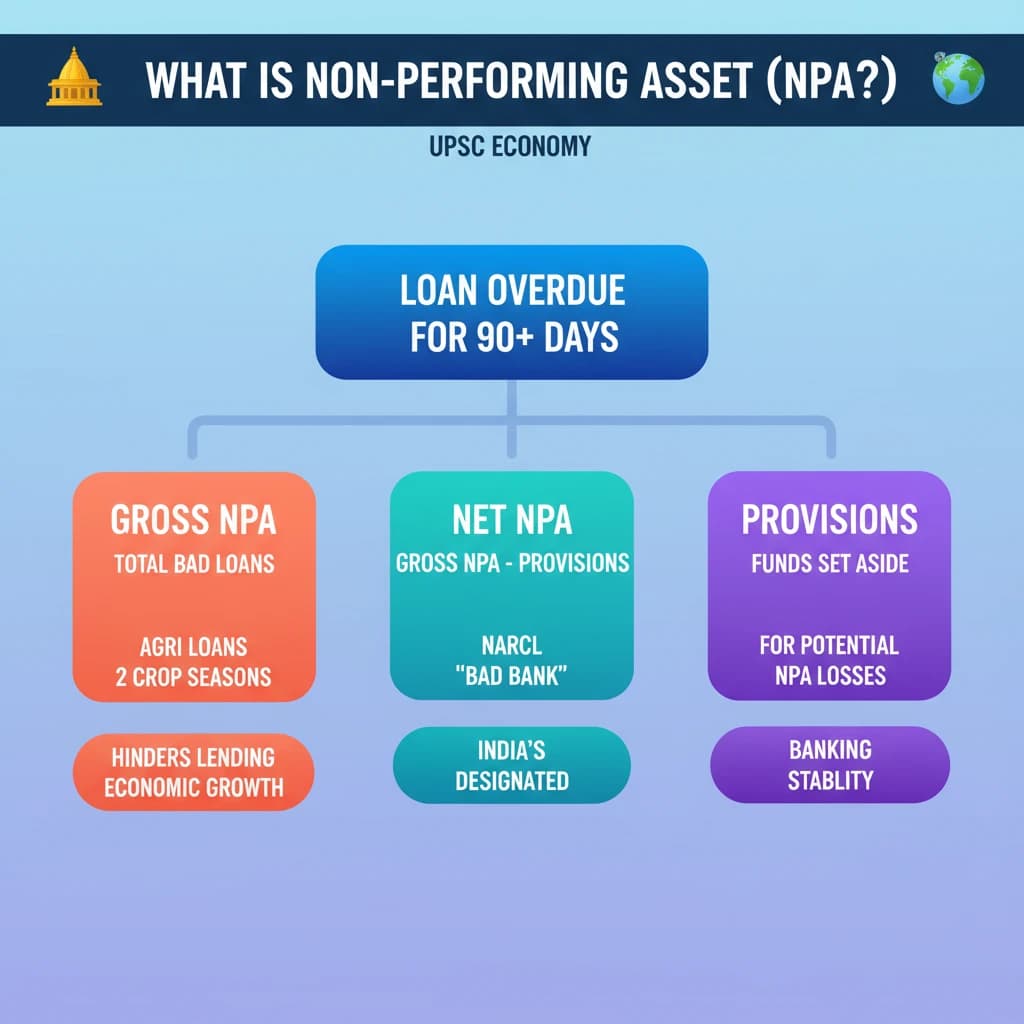

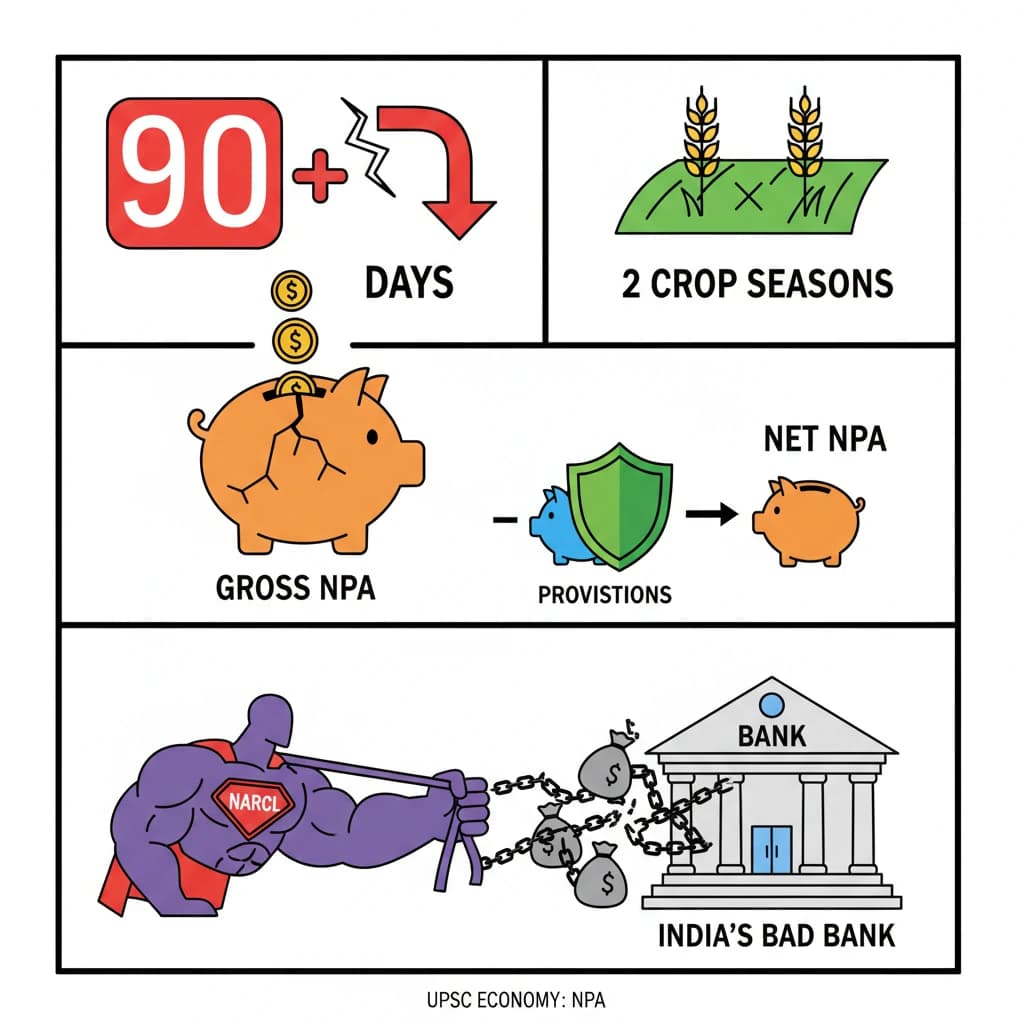

- NPA: Loan overdue for 90+ days (or 2 crop seasons for short-duration agri loans).

- Gross NPA = total bad loans; Net NPA = Gross NPA minus provisions.

- Provisions are funds set aside by banks for potential NPA losses.

- NARCL (National Asset Reconstruction Company Ltd) is India's designated 'Bad Bank'.

- High NPAs hinder fresh lending, impacting economic growth and investment.

What is Non-Performing Asset (NPA)?

Medium⏱️ 8 min read

economy

📖 Introduction

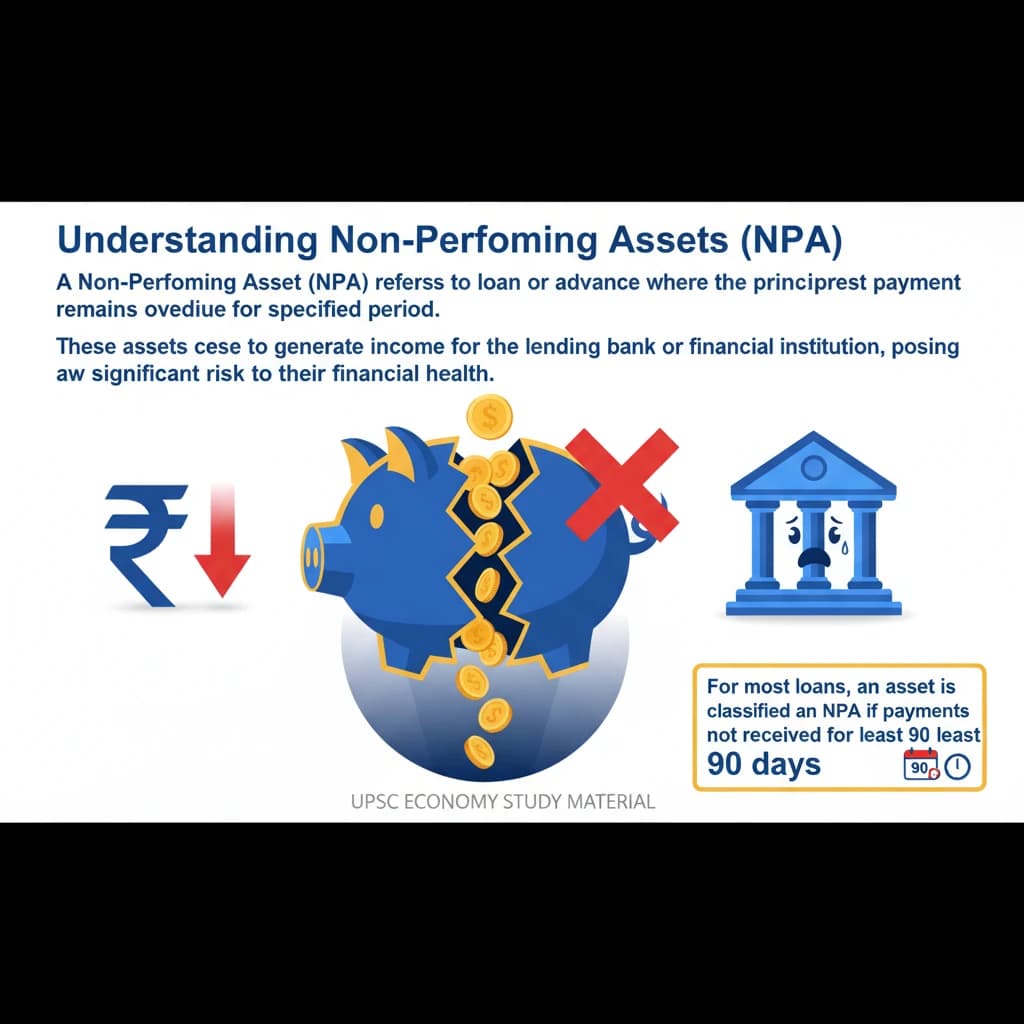

Understanding Non-Performing Assets (NPA)

A Non-Performing Asset (NPA) refers to a loan or advance where the principal or interest payment remains overdue for a specified period.

These assets cease to generate income for the lending bank or financial institution, posing a significant risk to their financial health.

For most loans, an asset is classified as an NPA if payments are not received for at least 90 days.

Special Case: Agricultural Loans

The classification criteria for agricultural loans differ, considering the seasonal nature of farming.

A loan granted for short-duration crops becomes an NPA if the principal or interest remains overdue for two crop seasons.

This adjustment recognizes the unique challenges faced by farmers in timely repayments.

Types of NPAs

NPAs are broadly categorized into Gross NPA and Net NPA, providing different perspectives on a bank's asset quality.

- Gross NPA: This represents the total value of non-performing assets held by a bank before any provisions are deducted.

- Net NPA: This is calculated by subtracting the provisions made by the bank from its Gross NPA. It gives a more realistic picture of the actual burden.

Understanding Provisions

Provisions are crucial for banks to mitigate risks associated with bad loans.

A provision refers to the funds that banks are mandated to set aside from their profits to cover potential losses arising from NPAs.

These funds act as a buffer, ensuring the bank can absorb losses without jeopardizing its stability.

Laws and Provisions Related to NPAs: The Bad Bank Concept

To address the burgeoning issue of NPAs, the concept of a "Bad Bank" has emerged as a significant mechanism.

A Bad Bank is essentially an entity that buys the bad loans (NPAs) from commercial banks, allowing them to clean up their balance sheets and focus on fresh lending.

In India, the National Asset Reconstruction Company Ltd (NARCL) has been designated as the country's "bad bank" to aggregate and resolve stressed assets.

Understanding NARCL is vital for UPSC Mains GS Paper 3 (Economy), especially questions related to financial sector reforms and banking challenges.

💡 Key Takeaways

- •NPA: Loan overdue for 90+ days (or 2 crop seasons for short-duration agri loans).

- •Gross NPA = total bad loans; Net NPA = Gross NPA minus provisions.

- •Provisions are funds set aside by banks for potential NPA losses.

- •NARCL (National Asset Reconstruction Company Ltd) is India's designated 'Bad Bank'.

- •High NPAs hinder fresh lending, impacting economic growth and investment.

🧠 Memory Techniques

95% Verified Content

📚 Reference Sources

•Reserve Bank of India (RBI) Guidelines on Asset Classification

•Ministry of Finance Reports

•Economic Survey of India